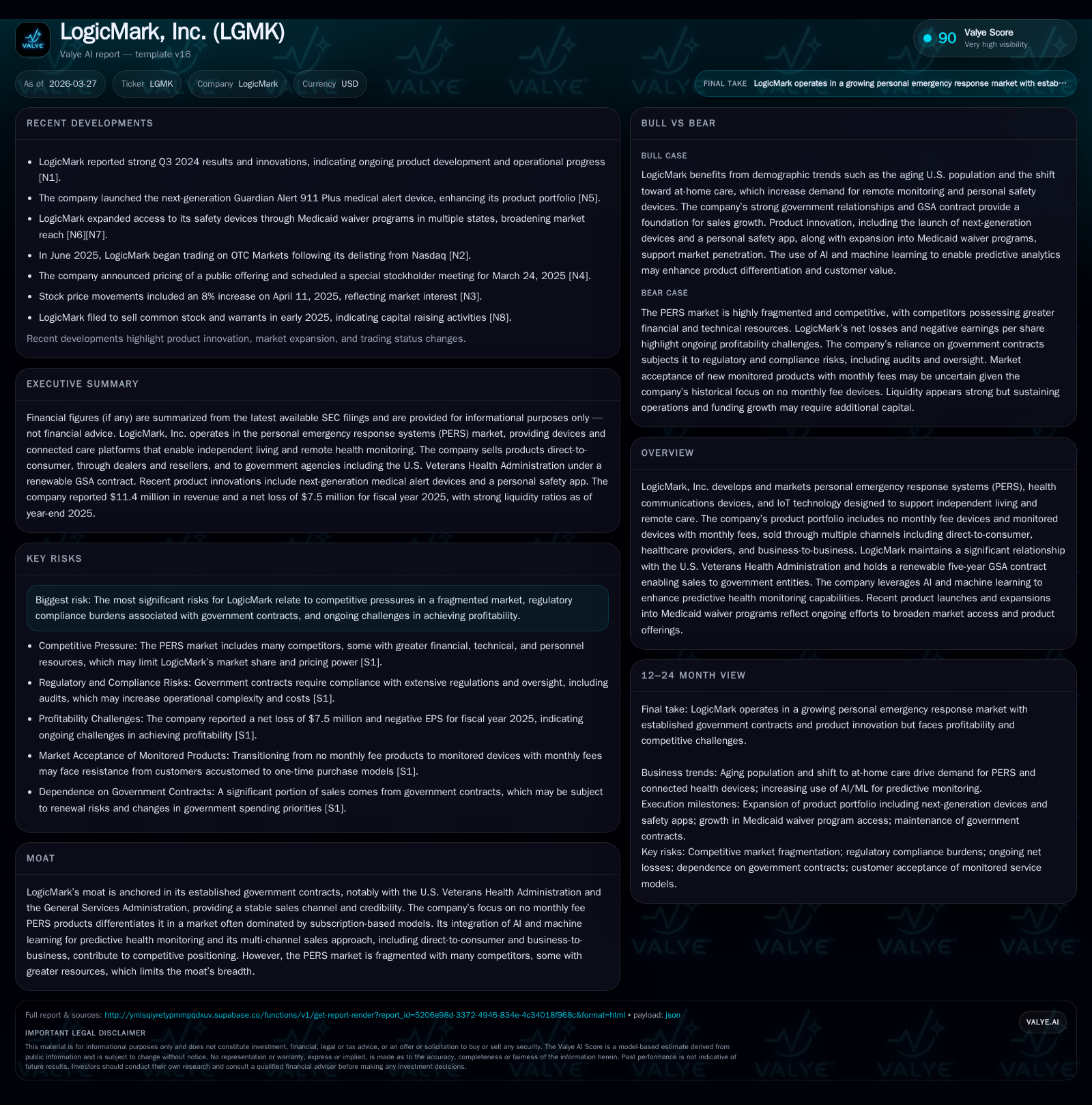

LogicMark's Pursuit of Connected Care: Government Contracts, AI, and Market Challenges

LogicMark leverages government partnerships and AI to expand in the personal emergency response market despite ongoing financial losses.

LogicMark, Inc. has grown revenue steadily over recent years while continuing to report operating and net losses. Its competitive strength stems from longstanding U.S. government contracts, including with the Veterans Health Administration and a renewed five-year GSA IDIQ contract, alongside a unique no monthly fee product offering. Investments in AI-powered predictive health monitoring and expansion into Medicaid markets support future growth ambitions. However, risks remain high due to intense competition, contract concentration, regulatory demands, and persistent negative cash flow. Key milestones such as contract renewals and product launches will be critical to monitor progress toward profitability.

Historical Performance: Revenue Growth Amid Operating Losses

LogicMark has experienced fluctuating revenue over the past four years with recent signs of recovery. Revenues declined from approximately $11.9 million in FY2022 to $9.9 million in FY2023 and FY2024 before rebounding by 15.4% to $11.4 million in FY2025 [F1]. Despite top-line gains, the company continues to report significant operating losses which slightly widened from -$7.7 million in FY2024 to -$7.9 million in FY2025. Net losses followed a similar trend improving from -$9.0 million in FY2024 to -$7.5 million in FY2025.

Operating cash flows have remained negative throughout this period with approximately -$5.1 million reported for FY2025. Capital expenditures have been minimal at just over $70 thousand in FY2025, signaling a focus on lean investment primarily geared toward product development rather than infrastructure expansion or fixed assets acquisition [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 11 | -7 | -5 | -8 | +15.4% | +17.1% |

| 2024 | 10 | -9 | -4 | -8 | -0.3% | +38.1% |

| 2023 | 10 | -15 | -4 | -15 | -16.7% | -110.1% |

| 2022 | 12 | -7 | -4 | -7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -5 | -45.9 |

| 2024 | -4 | -86.7 |

| 2023 | -111.0 | |

| 2022 | -4 | -33.0 |

Source: SEC companyfacts cache [F1].

Note: Parentheses denote negative values representing losses or outflows.

Market Position: Government Contracts and Product Differentiation

A core strength for LogicMark is its entrenched relationships with U.S. government entities including the Veterans Health Administration (VHA), which has accounted for sales exceeding 700 thousand devices since at least 2012, alongside a pivotal five-year General Services Administration (GSA) contract initially awarded in July 2021 and renewed early in February 2026 [S1], [S15]. This contract framework utilizes an indefinite delivery/indefinite quantity (IDIQ) structure providing flexible ordering capabilities over time.

Government contracts provide revenue stability but also concentration risk as margins are pressured by regulated procurement processes requiring continuous cost competitiveness for renewals or new awards [S1]. Loss of these key contracts would materially affect revenues and cash flow.

Differentiation arises from LogicMark’s "no monthly fee" personal emergency response systems contrasting with industry peers that typically rely on subscription models burdening consumers with recurring charges—making LogicMark's offering attractive particularly among low-income seniors or Medicaid populations seeking affordable independence solutions aligned with demographic shifts favoring at-home care [S13], [S17].

Technology Innovation: AI Integration and IoT Enhancements

LogicMark is advancing its technology through integration of artificial intelligence and machine learning aimed at evolving its PERS devices from reactive emergency alert systems toward predictive health monitoring platforms capable of anticipating health risks before emergencies occur [N1], [S5]. This transition leverages data captured via connected devices within an Internet of Things ecosystem.

These innovations necessitate sustained research and development investment amid constrained financial resources; capital expenditures remain modest reflecting prioritization of technology development over heavy infrastructure expansion [F1], [S12]. The company’s Care Platform-as-a-Service (CPaaS) initiative enables interoperability with third-party wearable devices enhancing data aggregation for proactive care.

While this technology edge may strengthen competitive positioning against larger rivals with broader resources, it also introduces execution risk common for smaller companies navigating rapid innovation cycles and intellectual property complexities within healthcare technology sectors.

Sales Channels and Market Expansion

LogicMark employs a multi-channel sales strategy including direct-to-consumer e-commerce platforms like Amazon.com alongside dealer/reseller networks and significant penetration within healthcare provider channels anchored by the VHA relationship cited above [N1], [S1].

Recent initiatives involve expanding participation in Medicaid waiver programs aimed at broadening access through public healthcare funding mechanisms as well as developing B2B partnerships targeting organizational care coordination services relevant across eldercare and other demographics requiring safety solutions beyond traditional PERS use cases [N1], [S17].

This evolution aligns with broader “Care Economy” trends emphasizing integrated digital health solutions supporting professional caregivers as well as family members.

Financial Overview: Cash Flow Management and Capital Allocation

Despite revenue growth reaching $11.4 million in FY2025 (+15% YoY), LogicMark continues to operate at a loss with an operating deficit near $7.9 million and net loss around $7.5 million for the year ending December 31, 2025 ([F1]). Operating cash flow remains negative at approximately -$5.06 million with minimal capital expenditure focused on product development rather than asset acquisition or capacity build-out ([F1]).

Balance sheet metrics indicate an improved equity position rising from about $10.4 million at end-2024 to roughly $16.3 million by end-2025 alongside working capital growth from $3.3 million to nearly $9.7 million reflecting enhanced short-term liquidity possibly supported by financing activities or improved receivables management though exact details are not explicit beyond standard disclosures ([F1], [S14]).

The company currently does not pay dividends nor repurchase shares prioritizing reinvestment towards operational sustainability and innovation funding given ongoing losses typical of growth-oriented medtech enterprises ([S11], [S21], [S26]). Preferred stock dividends are paid per contractual obligations but structured not to unduly constrain operational liquidity.

Risk Factors: Competition, Contract Dependence & Regulatory Challenges

LogicMark operates within a highly fragmented personal emergency response system market featuring competitors ranging from emerging startups focusing solely on PERS innovations to large established corporations possessing greater financial resources brand recognition distribution networks intellectual property portfolios ([S13]). Larger competitors may leverage integrated telecom or security service offerings enabling aggressive pricing strategies that challenge standalone device adoption economics.

The company’s reliance on government contracts subjects it to competitive rebidding under IDIQ frameworks exposing margins to pressure; any loss or non-renewal would have material adverse effects ([S1]). Regulatory compliance imposes significant operational costs encompassing federal communications certification product safety audits government oversight ([S1], [S3], [S6]). Intellectual property protection remains challenging given limited internal patent defense resources coupled with infringement risk ([S8], [S9]).

Geopolitical risks arise from supply chain dependence on Taiwanese manufacturing facilities exposed to cross-strait tensions that could disrupt production continuity ([S7]).

Outlook & Milestones

Key upcoming milestones include renewal outcomes of the GSA IDIQ contract which secures primary federal market access alongside potential expansions into additional governmental agency channels ([N1], [S1]). Product launch execution particularly of AI-enabled devices will be critical indicators of progress toward competitive differentiation. Monitoring quarterly cash burn versus financing availability will inform runway sufficiency influencing capital raise needs and strategic flexibility. Tracking uptake within Medicaid programs offers insight into penetration success within new payer segments essential for scaling volume economics.

Conclusion: Navigating Growth Amid Financial Constraints

LogicMark combines technological innovation leveraging AI-enhanced PERS products with strong government contracting foundations conferring credibility amidst intense competition ([F1], [N1], [S13]). While recent top-line recovery signals demand traction persistent operating deficits and negative cash flows underscore execution challenges compounded by contract concentration regulatory complexities and geopolitical supply vulnerabilities. The company faces the delicate task of balancing continued R&D investment necessary for technological leadership against strict financial discipline preserving liquidity essential for survival within an evolving digital health landscape. Investors should weigh long-term strategic value drivers against near-term fiscal headwinds inherent to companies scaling within fast-changing connected care markets.

This analysis is based solely on publicly disclosed information without endorsement or prediction regarding investment outcomes.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments