Non-Invasive Monitoring Systems: From Dormant Assets to Uncertain Horizons

This analysis explores the evolution of Non-Invasive Monitoring Systems Inc. from its discontinued therapeutic platform operations toward a future shadowed by financial distress and potential strategic transformation.

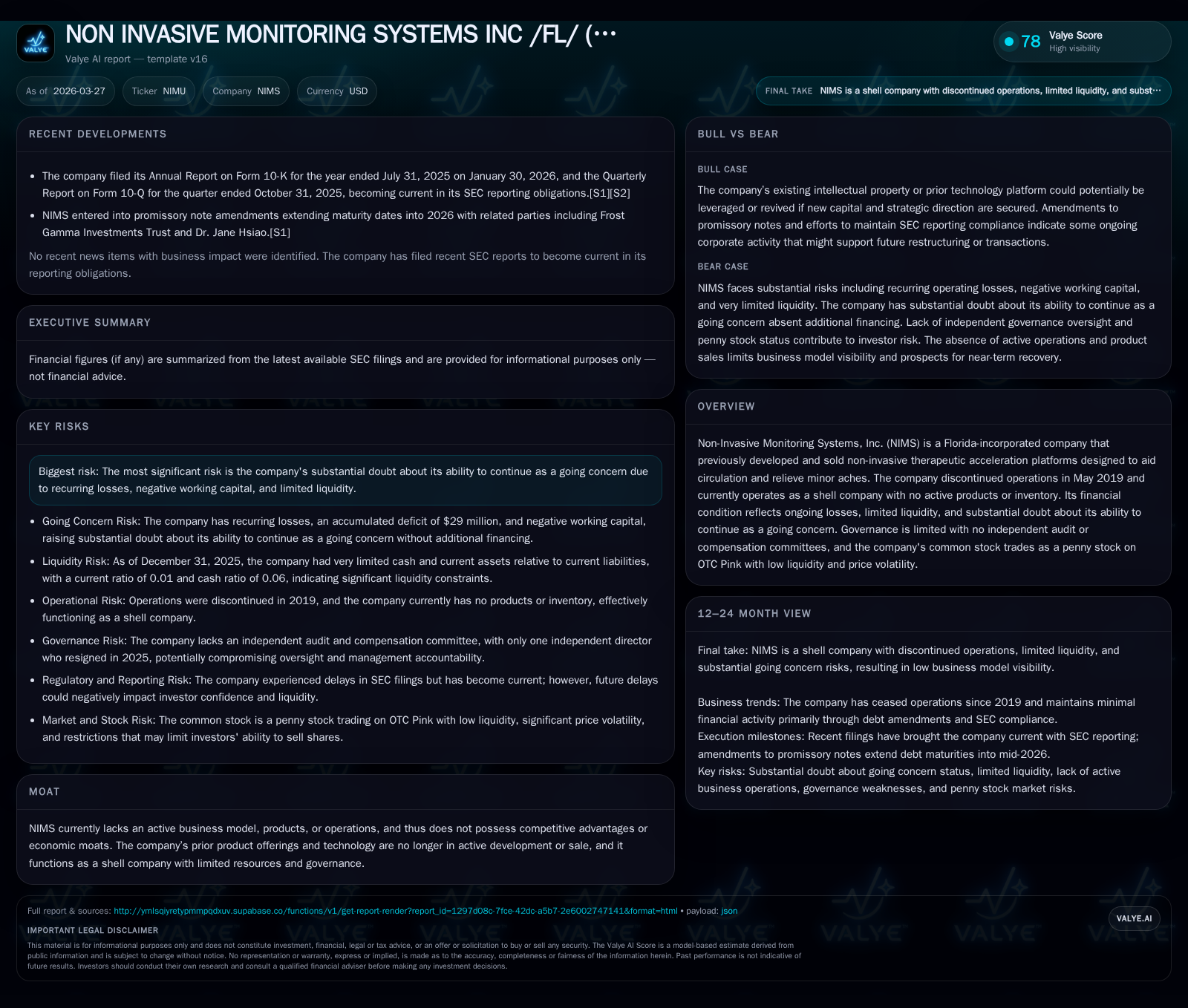

Non-Invasive Monitoring Systems Inc. (NIMS) once developed non-invasive therapeutic acceleration products but ceased operations in May 2019 and currently functions as a shell company with no active business. The company exhibits persistent operating losses, a deteriorating liquidity position with a current ratio near 0.01, and substantial doubt about its ability to continue as a going concern. A recently announced merger agreement signals a possible strategic pivot, but financial and governance challenges remain significant obstacles. Investors should monitor merger progress, capital raising efforts, and regulatory filings for clarification on the company's future trajectory.

Legacy of Product Innovation and Discontinuation

Founded in 1980 and headquartered in Miami, Florida, Non-Invasive Monitoring Systems Inc. originally engaged in research, development, manufacturing, marketing, and sales focused on non-invasive motorized platforms providing whole body periodic acceleration (WBPA). These devices aimed to temporarily increase local blood circulation to relieve minor aches and pains while facilitating muscle relaxation and reducing stiffness. However, the company effectively discontinued all active operations as of May 2019, electing to operate solely as a shell company defined per Rule 12b-2 of the Exchange Act. As such, it holds no inventory nor offers any products for sale currently [S1][S11]. This transition marks a stark contrast from its earlier innovation-driven existence to a dormant enterprise without ongoing commercial activities.

Financial Performance and Liquidity Analysis Over Time

Financially, NIMS manifests chronic deficits with minimal top-line revenue—historically peaking at only $23,000 in FY2016—and persistently negative operating income since at least FY2022. Operating income was recorded at -$21,000 by FY2025 improving from -$59,000 in FY2024 but still reflective of ongoing losses [F1]. Net income followed suit, narrowing from a loss of -$113,000 in FY2024 to -$49,000 in FY2025. Operating cash flow remained negative across these years with -$22,000 reported in FY2025 against -$182,000 in FY2024. Importantly, liquidity constraints are severe: current assets totaled roughly $6,000 against current liabilities around $1 million at year-end 2025, yielding a current ratio approximately 0.01—indicating extreme inability to cover short-term obligations [F1]. This places acute pressure on funding operations absent external support.

Historical performance (annual)

| FY | Net ($) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -49000 | -22000 | -21000 | +56.6% |

| 2024 | -113000 | -182000 | -59000 | +43.2% |

| 2023 | -199000 | -158000 | -169000 | -15.0% |

| 2022 | -173000 | -190000 | -159000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 4.9 |

| 2024 | 15.6 |

| 2023 | 32.5 |

| 2022 | 41.9 |

Source: SEC companyfacts cache [F1].

*FY2025 figures for current assets, liabilities and ratio approximate latest quarterly data [F1].

Structural Challenges Behind the Going Concern Doubt

Recurring operational losses coupled with an accumulated deficit nearing $29 million by July 31, 2025 underpin substantial doubt regarding NIMS’s ability to continue as a going concern. The balance sheet shows equity declining steadily into negative territory (-$996,000 by FY2025), compounded by negative working capital approximating $947,000 at mid-2025 [F1][S1][S8]. Cash reserves stood precariously low around $3,000 at fiscal year-end according to filings [S1], underscoring liquidity risk. Management explicitly acknowledges that absent additional financing—through equity issuance, debt instruments or strategic mergers—the company risks insolvency leading potentially to total shareholder value erosion [S1][S8]. These systemic challenges crystallize investor risk with no clear pipeline of revenue-generating operations.

Capital Allocation History and Shareholder Returns Assessment

NIMS maintains authorization for upwards of 400 million common shares alongside preferred stock issuances; however as of January 30, 2026 approximately 154.8 million common shares were outstanding along with preferred shares including Series B stock [S5][F1]. There is no history or expectation of dividend distributions due to continuing losses; management cites retention of earnings—if any—to support operational needs [S7]. The firm operates within penny stock regulations given extremely low trading prices on OTC Pink markets (<$0.01 per share) which further depresses liquidity and suppresses investor exit opportunities due to broker-dealer compliance burdens [S7][S9]. Capital allocation has included multiple promissory notes primarily from insiders or related parties—directors holding significant equity stakes—highlighting reliance on related-party financing amid public market constraints . Governance gaps are apparent: absence of independent audit or compensation committees arguably weakens stewardship over capital deployment and shareholder protections [S12]. This constellation reduces prospects for stable returns or value preservation absent fundamental business revival.

Prospects for Future Growth and Emerging Constraints

Given that NIMS ceased product-based operations over six years ago and currently holds no inventory or active lines of business, organic growth prospects are nil. The company candidly discloses its reliance on new capital infusions via public/private equity offerings or substantial business combinations including mergers or acquisitions for survival or future growth potential [S1][S6][S8]. Terms for such financing may entail significant dilution or restrictive covenants detrimental to existing shareholders. Moreover regulatory filing delays reported recently cast shadows over administrative capacity potentially complicating timely execution of strategic initiatives [S2][S13]. Thus any growth trajectory remains completely contingent upon successful external transactions rather than internal commercialization.

Corporate Governance and Reporting Irregularities

Material weaknesses identified in internal controls over financial reporting raise concerns regarding accuracy and timeliness of disclosures critical for investor assessment [S1][S6][S12]. The company experienced lapses delaying Annual Report (10-K) filings for fiscal year ended July 31, 2025 alongside subsequent Quarterly Reports (10-Q), resulting in periods out-of-compliance with SEC reporting obligations that may diminish market trust and restrict information availability [S2][S13]. Governance further suffers from lack of independent directors able to form audit or compensation committees; the sole independent board member resigned in August 2025 leaving management-dominated oversight unresolved [S12]. Such deficiencies may compromise risk evaluation processes essential during transition phases.

Key Milestones and Watchpoints for Potential Investors

Most notably since March 6, 2026 NIMS entered into an Agreement and Plan of Merger with Gravitics—a private entity involved in designing and manufacturing space infrastructure assets such as orbital carriers and modules serving commercial space development missions. This deal contemplates NIMS changing its name and ticker symbol post-close expected on or before June 30, 2026 subject to customary closing conditions including shareholder approvals and FINRA/NASDAQ clearances [S3][S17]. The transaction is structured as a tax-qualified reorganization under Section 368(a) implying accounting whereby Gravitics will be treated as the acquirer upon consummation replacing historical NIMS financials going forward.

Investors should closely track approval processes for this merger including regulatory filings (e.g., S-4 registration statements), effectuation of planned reverse stock split required by FINRA/penny stock rules for uplisting applications, debt conversions impacting capitalization structure estimated near $800K plus accrued interest principal conversion or paydown requirements by closing date preparations [S17][S20]. These factors collectively represent pivotal catalysts that could redefine the company's strategic direction away from a dormant shell status toward an operational business albeit entirely unrelated to legacy medical device applications.

Strategic Options Amid an Uncertain Business Model

Analysis: Given the absence of active products or generating revenue streams post-2019 discontinuation, NIMS exists primarily as a vehicle for external corporate transactions rather than a traditional operational entity. Its future options include completing the pending reverse merger with Gravitics thereby shifting business sectors entirely into commercial space hardware; alternatively it could pursue licensing or sale of residual intellectual property though no such initiatives are publicly documented.

As an OTC Pink shell company characterized by poor liquidity and regulatory filing irregularities combined with severe financial constraints—a recurrent pattern typical among microcap shells—the firm may serve speculative investors seeking reverse-merger opportunities rather than income-focused stakeholders requiring operational visibility or earnings stability.

In essence,NIMS’s valuation hinges less on historical product merit than on ability to successfully execute transformational merger agreements entailing comprehensive governance overhaul including appointment of a majority independent board structure post-merger enhancing compliance credibility consistent with Nasdaq standards [S17]. Until closing risks resolve decisively via formal announcements confirming transaction completion timelines this remains highly speculative.

This report aims solely at describing known facts derived from sources including recent SEC filings through March 2026 without offering investment advice or recommendations. The uncertainties surrounding Non-Invasive Monitoring Systems Inc.’s ongoing viability caution interpretation strictly within context supplied herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments