Zentalis Pharmaceuticals’ Azenosertib Clinical Progress Confronts Capital and Regulatory Hurdles

Azenosertib advances as a potential first-in-class therapy for Cyclin E1-positive platinum-resistant ovarian cancer amid continued operating losses and evolving regulatory risks.

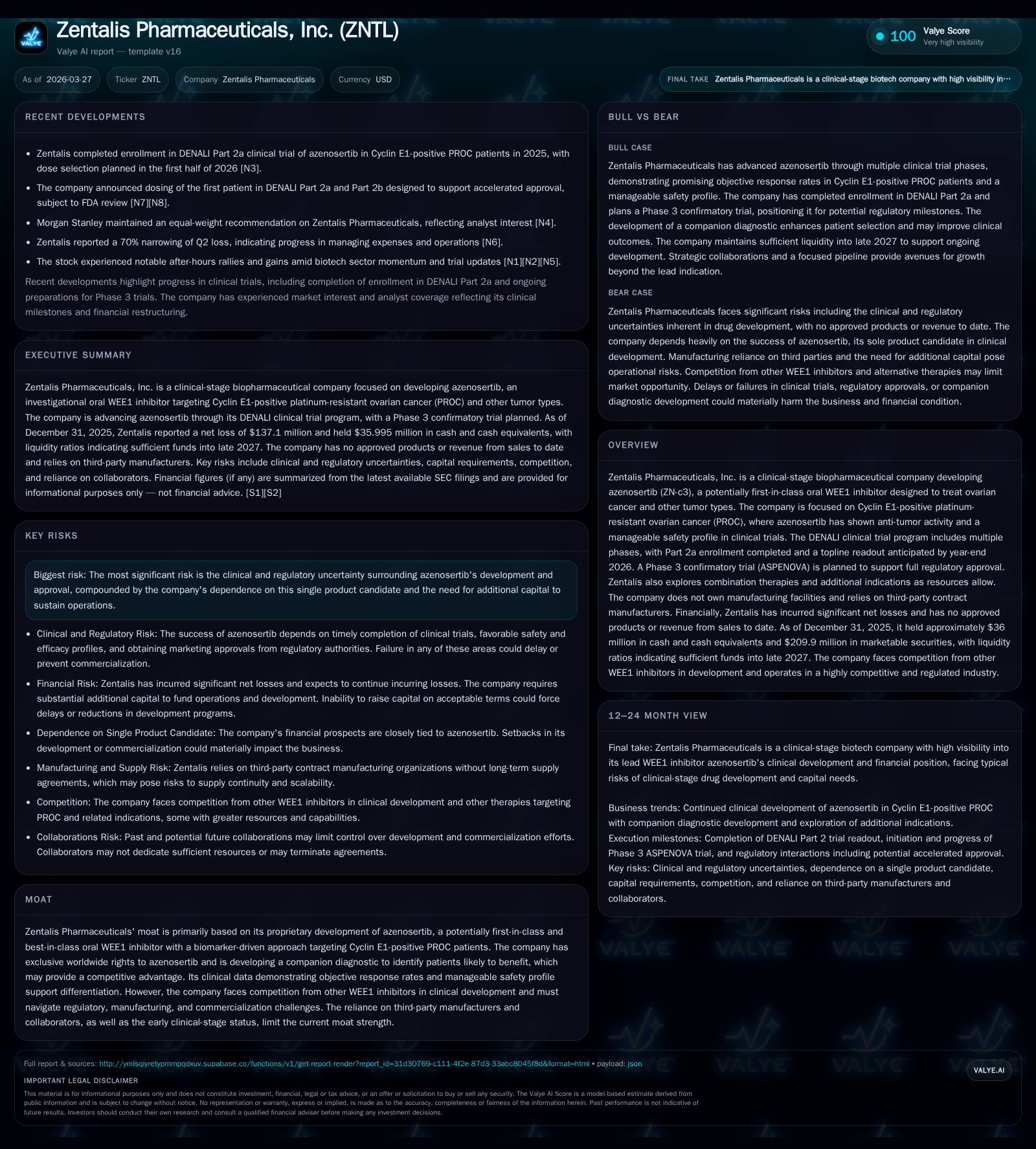

Zentalis Pharmaceuticals remains focused on developing azenosertib, an oral WEE1 inhibitor targeting Cyclin E1-positive PROC patients, with Phase 2 topline data expected by late 2026. Historical setbacks have led to persistent net losses exceeding $100 million annually, though costs declined in 2025 following strategic restructuring. The pathway to regulatory approval hinges on data from the DENALI Part 2 trial, with a confirmatory Phase 3 study planned. While the company’s proprietary biomarker-driven approach offers differentiation, reliance on a single product candidate and third-party manufacturers presents financial and operational challenges. Coverage, reimbursement, and healthcare compliance risks also loom over prospective commercialization.

Company Background and Product Focus

Zentalis Pharmaceuticals is a clinical-stage biopharmaceutical company concentrating its R&D efforts on azenosertib (ZN-c3), a potentially first-in-class oral inhibitor of WEE1 kinase. WEE1 regulates DNA damage response; its inhibition by azenosertib disrupts repair processes in cancer cells, promoting mitotic catastrophe especially in tumor cells with Cyclin E1 overexpression—a biomarker linked to poor prognosis in platinum-resistant ovarian cancer (PROC). The proprietary immunohistochemistry (IHC) cutoff developed by Zentalis aims to identify patients most likely to benefit from treatment.

Historical Performance

Since its inception, Zentalis has not commercialized any products and has relied exclusively on equity financings to fund operations. Net losses remain significant but showed improvement in the most recent fiscal year owing largely to strategic cost reductions.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -137 | -125 | -153 | 0 | +17.4% |

| 2024 | -166 | -171 | -191 | 0 | +43.2% |

| 2023 | -292 | -208 | -300 | 1 | -23.4% |

| 2022 | -237 | -164 | -227 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -125 | -63.4 |

| 2024 | -171 | -49.2 |

| 2023 | -208 | -66.8 |

| 2022 | -166 |

Source: SEC companyfacts cache [F1].

Note: Revenues are absent given early-stage status without approved products.

Operating income improved by approximately 20% year-over-year from 2024 to 2025 [F1], primarily driven by reductions in R&D spend associated with their principal program.

Pipeline and Development Prospects

Zentalis' lead candidate azenosertib targets a niche but clinically pressing indication: Cyclin E1-positive PROC patients who have limited options beyond chemotherapy with modest benefits. Approximately half of PROC patients overexpress Cyclin E1 based on company analyses covering major Western markets—U.S., EU4 countries plus UK—representing an estimated patient pool of about 21,500 annually [S1].

The ongoing DENALI Phase 2 study has completed Part 2a enrollment targeting this biomarker-defined population with topline results slated for late-2026. Positive results could support accelerated approval pathways contingent upon FDA feedback. Moreover, a confirmatory ASPENOVA Phase 3 trial is planned as a prerequisite for full marketing authorization [S1].

Beyond monotherapy indications in PROC, Zentalis explores combination regimens—such as pairing azenosertib with bevacizumab maintenance therapy—as well as investigating efficacy across other tumor types holding Cyclin E1 dysregulation. These expansions remain resource-dependent given current financial constraints.

Financial Condition and Capital Allocation

The company reports no revenues or product sales; all operating expenses relate to R&D and corporate overheads. Research and development expenditures declined from prior years reflecting strategic prioritization of resources toward advancing azenosertib efficiently within clinical programs [F1][S17].

Operating cash flow was negative $125 million in the most recent fiscal period with near-zero capital expenditure outlays indicating minimal fixed asset investments consistent with biopharma model relying on third-party manufacturing capabilities [F1]. The equity base decreased alongside net losses but remains sufficient for ongoing operations into late-stage clinical milestones without immediate capital raises reported.

Approximate annual return on equity (ROE) stands negative at around -63%, reflecting deep continued investment into pipeline development absent any commercialization or licensing revenue streams so far [F1].

No dividends or share repurchase programs exist per filings; all cash generated or raised is reinvested into clinical development.

Risks and Operational Challenges

Zentalis faces multiple high-stakes risks typical for clinical-stage biotech firms:

- Clinical & Regulatory Uncertainty: Success depends heavily on positive DENALI Part2a results leading toward accelerated FDA approval attempts. Failure or delay would significantly hinder commercial prospects [S4][S5].

- Capital Requirements: With no product revenue currently and significant operating losses ($137M net loss FY2025), additional fundraising will be required to support costly Phase 3 trials and possible eventual commercialization efforts.

- Manufacturing Reliance: The absence of owned manufacturing assets mandates robust third-party partnerships which can introduce supply chain vulnerabilities or cost escalations.

- Healthcare Laws and Reimbursement: Post-approval market access depends on complex payer coverage decisions both domestic and abroad under increasingly stringent pricing regulations such as Medicare negotiations introduced by the Inflation Reduction Act (IRA) effective soon [S13][S16]. Commercial success requires navigating these evolving mechanisms successfully.

- Legal Compliance Risks: Adherence to multifaceted anti-kickback statutes, fraud prevention laws including False Claims Act provisions and international equivalents requires rigorous corporate governance lest penalties or reputational damage ensue [S7][S12][S19].

- Intellectual Property Litigation: Competitor patent disputes or infringement claims common in the pharmaceutical space could divert managerial focus and incur material costs [S14].

Sector Context Analysis

WEE1 kinase inhibitors are emerging as attractive targets especially when paired with biomarker-driven strategies that improve patient selection precision—a trend that could alter standard care frameworks if validated clinically. Oral small molecule oncology agents offer convenience advantages but must demonstrate durable efficacy gains vs existing lines including PARP inhibitors which increasingly saturate ovarian cancer treatment after platinum-resistance emerges.

Incorporating companion diagnostics alongside therapeutics aligns with personalized medicine momentum but adds complexity related to diagnostic approval pathways and payer reimbursement structures.

Milestones To Watch (Analysis)

Investors should closely monitor:

- Announcement of topline safety and efficacy data from DENALI Part 2a expected by end of calendar year 2026,

- FDA feedback regarding accelerated approval prospects post-DENALI,

- Initiation timelines for the ASPENOVA Phase 3 confirmatory study,

- Potential partnership announcements that might provide capital or commercial infrastructure,

- Progress validating companion diagnostic toward co-approval which may influence market uptake dynamics.

Summary Outlook

Zentalis Pharmaceuticals operates at the intersection of cutting-edge oncology drug development and precision medicine targeting unmet needs within PROC populations defined by biomarker expression profiles. Although the scientific rationale for azenosertib appears compelling backed by early-phase clinical activity signals and targeted patient stratification tools under development,[S1] commercialization remains several years away pending pivotal clinical outcomes with accompanying regulatory review cycles.

Financially constrained yet disciplined operationally following recent restructuring,[F1][S17] Zentalis faces critical inflection points tied to trial results which will dictate future capital strategy and partnership discussions. The company must navigate multilayered legal/regulatory compliance regimes alongside reimbursement challenges which could complicate market access efforts even after potential approval.[S4][S13]

The concentrated focus on a single product candidate intensifies execution risk but also sharpens resource allocation toward streamlined evidence generation required for regulatory submissions.[S10]

This report is intended solely for informational purposes reflecting public filings and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments