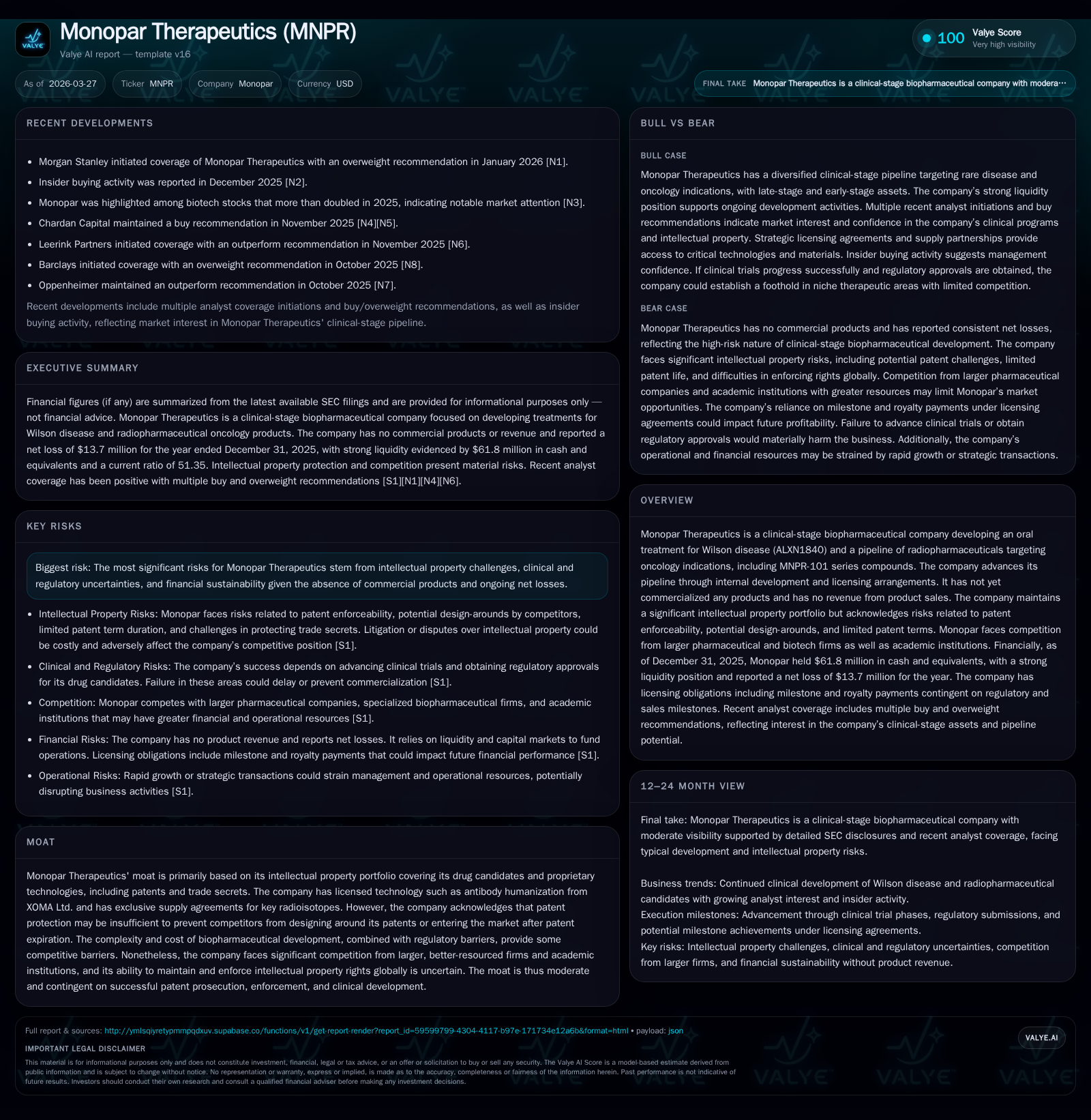

Monopar Therapeutics’ Transitioning Clinical Pipeline Faces Capital and IP Challenges

Monopar develops oral and radiopharmaceutical treatments, with no commercial revenue yet and deepening net losses.

Monopar Therapeutics is a clinical-stage biotech company advancing an oral Wilson disease candidate alongside oncology-focused radiopharmaceuticals. It remains pre-revenue, funding R&D chiefly through equity issuance, with a cash runway extending beyond 2027 but sustained net losses persisting. Intellectual property forms a moderate moat, complicated by global patent enforcement risks and potential design-arounds. Upcoming milestones hinge on clinical progress amid competitive pressures, while capital allocation prioritizes pipeline advancement over shareholder returns.

Company Background and Historical Performance

Monopar Therapeutics is a clinical-stage biopharmaceutical company developing therapeutics for rare diseases and oncology indications. Its lead assets include ALXN1840, an investigational once-daily oral treatment for Wilson disease—a genetic disorder causing copper accumulation—and the MNPR-101 series of radiopharmaceuticals targeting cancers expressing the urokinase plasminogen activator receptor (uPAR).

The company has not generated any product sales revenue to date [F1]. Financial results reflect typical early-stage biotech dynamics characterized by sustained operating losses driven by research and clinical trial costs.

Historical performance (annual)

| FY | Rev | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0 | -14 | -12 | -17 | +12.0% |

| 2024 | 0 | -16 | -6 | -16 | -85.5% |

| 2023 | 0 | -8 | -8 | -9 | +20.1% |

| 2022 | -11 | -7 | -11 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -10.0 |

| 2024 | -28.3 |

| 2023 | -150.4 |

| 2022 | -104.2 |

Source: SEC companyfacts cache [F1].

The company’s operating losses have persisted with modest year-over-year improvement in net income in FY2025 compared to FY2024 [F1]. Operating cash flow remains negative and increased in magnitude in FY2025 as clinical activities intensified. Equity has expanded significantly due to capital raises rather than earnings retention.

Business Model and Pipeline Development

Monopar’s strategy focuses on advancing proprietary drug candidates through clinical validation targeting unmet medical needs:

- ALXN1840 for Wilson disease represents a late-stage oral therapy candidate addressing a rare genetic disorder.

- The MNPR-101 radiopharmaceutical series includes imaging and therapeutic agents aimed at uPAR-positive tumors.

The company also licenses late preclinical or clinical assets to augment its pipeline [S22]. This approach leverages scientific expertise to reduce discovery risk but entails substantial ongoing expenditures without near-term revenues [F1].

Intellectual Property and Competitive Positioning

Monopar’s intellectual property portfolio includes patents covering its compounds and technologies alongside trade secrets and proprietary know-how secured via confidentiality agreements. Licensed technologies such as antibody humanization from XOMA Ltd. support its programs [S1].

However:

- Patent terms are finite with typical U.S. durations of up to 20 years from filing date; extensions may be available but eventual expiry is unavoidable [S1].

- Competitors might design around patents potentially eroding exclusivity [S1][S16].

- Enforcement challenges exist internationally due to variable IP law rigor [S16].

- Patent litigation or disputes could impose significant costs and divert management attention [S14][S15].

- Third-party claims may require licenses that could be costly or unavailable [S15][S23].

Competitors include larger pharmaceutical companies with deeper resources for R&D and legal defense.

Thus Monopar’s IP-based moat is moderate: providing barriers to entry but dependent on continued innovation success and effective enforcement.

Financial Position and Capital Allocation

At fiscal year-end 2025:

- Cash and cash equivalents stood at approximately $61.8 million supporting operations into late 2027 based on management’s forecasts [F1][S19].

- The company had an accumulated deficit of about $89.5 million reflecting cumulative net losses since inception [F1].

- Equity increased substantially through equity offerings including public placements; no dividends have been declared nor share repurchases undertaken consistent with the developmental stage [F1][S9][S13].

Capital allocation prioritizes advancing clinical programs over shareholder returns.

Growth Outlook and Key Milestones

Future growth prospects depend on:

- Progression of ALXN1840 through pivotal late-stage trials potentially leading to regulatory submissions.

- Clinical data from Phase 1 studies of MNPR-101 imaging and therapeutic agents assessing safety and efficacy.

- Potential strategic collaborations or licensing deals that could provide milestone payments or co-development funding.

Constraints include clinical trial risks such as delays or adverse outcomes; IP protection challenges; funding uncertainties; and competitive pressures.

Key events to monitor include trial enrollment completions, top-line data announcements for ALXN1840, regulatory interactions regarding Wilson disease therapy approval pathways, updates from MNPR-101 Phase 1 trials on imaging efficacy and therapeutic safety profiles; plus any new licensing transactions impacting capital needs.

Risks Summary

Principal risks involve:

- Intellectual property litigation potentially resulting in costly legal proceedings or licensing obligations [S14][S25].

- Clinical development uncertainties inherent to orphan diseases complicating trial execution.

- Financial sustainability given recurring net losses necessitating continued access to capital markets amid uncertain investment climates [S19].

- Regulatory compliance complexities including healthcare legislation affecting pricing or reimbursement environments adversely impacting future revenues.

The company maintains indemnification provisions for officers/directors alongside internal control certifications supporting governance standards but remains exposed to sector-wide operational risks [S7][S21].

Conclusion

Monopar Therapeutics exemplifies a classical clinical-stage biotech profile: no revenue generation yet deepening net losses funded through equity raises supporting a diversified pipeline anchored by an orphan disease candidate alongside novel oncology radiotherapies. Its liquidity position affords operational runway well into late 2027 absent unforeseen setbacks.

The moderate intellectual property moat is tempered by external patent challenges amid competition largely from better-capitalized peers. Sustained focus should be placed on forthcoming clinical milestones informing regulatory feasibility paired with monitoring capital efficiency reflecting financial resilience while managing inherent IP litigation exposures critical for long-term value creation potential within this challenging sector environment.

Disclaimer: This analysis is based solely on disclosed public financial data up to fiscal year-end 2025 and SEC filings through March 27th, 2026. It does not constitute investment advice but aims to provide a grounded evaluation of Monopar Therapeutics’ business dynamics within current evidentiary constraints.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments