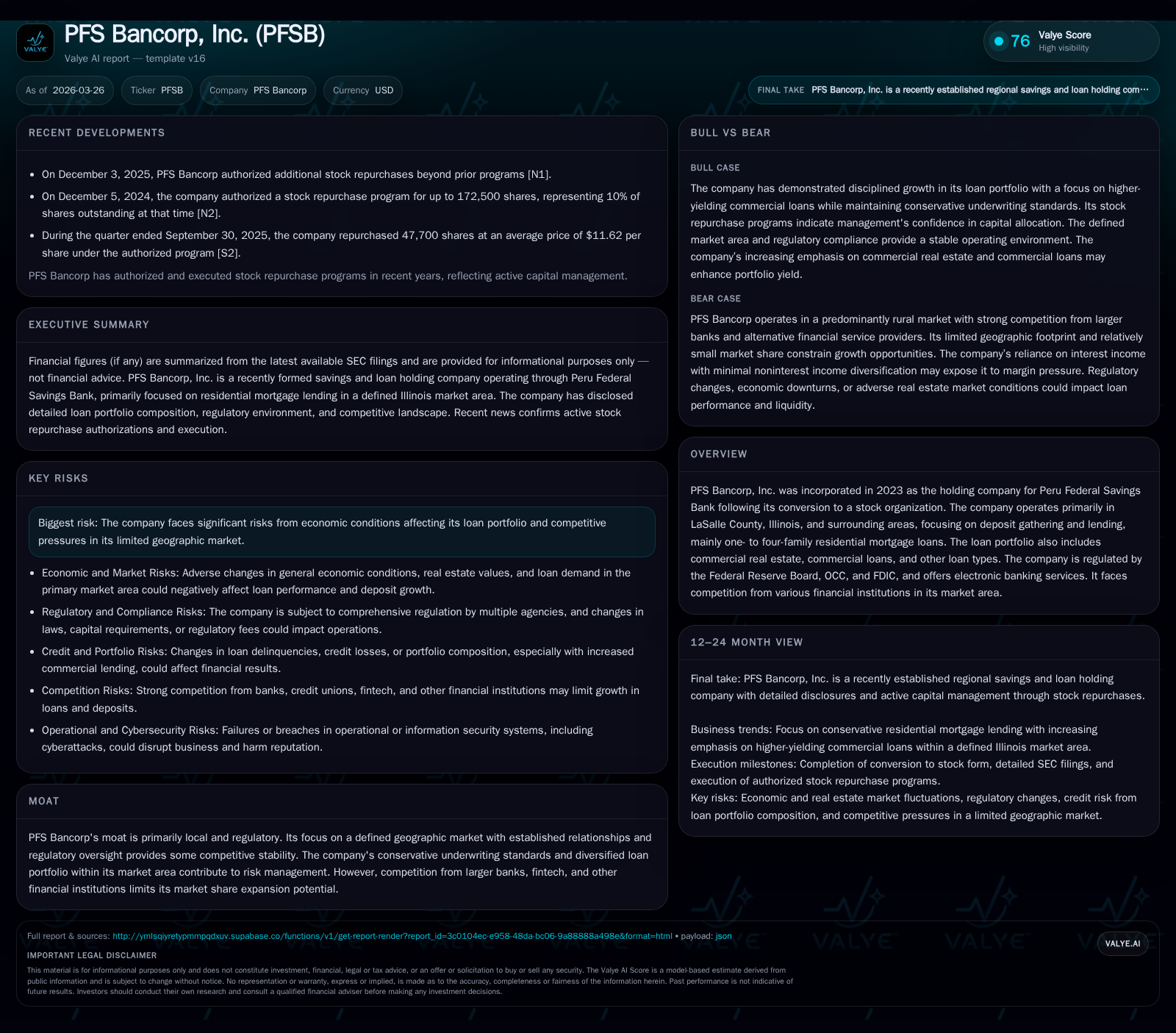

PFS Bancorp’s Modest Expansion and Capital Management Reflect Local Market Limits

Focused on community banking, PFS Bancorp grows cautiously with conservative underwriting and steady capital allocation.

PFS Bancorp, Inc., established in 2023 from Peru Federal Savings Bank’s mutual-to-stock conversion, operates predominantly in LaSalle County, Illinois, emphasizing residential mortgage lending. While its small geographic footprint and local regulatory environment provide some competitive stability, growth is constrained by intense competition and economic sensitivity. The company’s financials show solid recent income growth driven by operational efficiency and loan portfolio expansion. Capital allocation prioritizes buybacks over dividends to enhance shareholder value amid limited earnings scope. Continued prudent underwriting and deposit growth will be critical amid rising interest rates and regional economic conditions.

Background and Market Focus

PFS Bancorp, Inc. emerged in October 2023 as the stock holding company for Peru Federal Savings Bank following its mutual-to-stock conversion [S13]. This event marked a significant structural shift but did not change the company’s fundamental business model: serving a community-centric banking franchise centered primarily in LaSalle County, Illinois [S1]. Operating out of two main physical branches in Peru, Illinois, it draws heavily on longstanding local relationships established since Peru Federal's founding in 1887 [S15]. The bank’s competitive moat lies in this tight geographic focus combined with close regulatory oversight by the OCC, FDIC, and Federal Reserve Board [S1], fostering conservative underwriting and risk management.

Historical Performance and Financial Trajectory

PFS Bancorp’s reported net income increased significantly from $905,000 in 2024 to $1.67 million in 2025 — an 84.6% improvement [F1]. This sharp margin expansion aligns with net interest income growth supported by rising loan balances and improved deposit cost management amid an upward interest rate environment [S21]. Operating cash flow likewise surged by over 56%, reaching $2.14 million in 2025 [F1]. Capital expenditure plummeted nearly tenfold compared to prior year levels ($21K vs $219K), bolstering free cash flow generation to approximately $2.12 million [F1]. This cash flow strength underpins the company's ability to fund growth organically while sustaining capital returns.

The loan portfolio expanded notably during this period with total net loans increasing from approximately $96 million at end-2024 to nearly $109 million at end-2025 [S14], predominantly anchored by residential mortgages making up about 63% of loans—$69.2 million [S5]. To mitigate concentration risk and enhance yield potential, management is also targeting incremental origination growth in commercial real estate ($29.4 million) and commercial loans ($5.7 million), which carry comparatively higher credit risk profiles [S5][S24]. Importantly, despite portfolio growth pressures, asset quality metrics remain strong with nonperforming assets at a negligible 0.37% of total assets [S5].

Financial Summary Table

Historical performance (annual)

| FY | Net ($) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 1671000 | 2 | 21000 | +84.6% |

| 2024 | 905000 | 1 | 219000 | -10.2% |

| 2023 | 1008000 | 2 | 44000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1325000 | 2 | 4.3 |

| 2024 | 63000 | 1 | 2.5 |

| 2023 | 400000 | 2 | 2.8 |

Source: SEC companyfacts cache [F1].

Net income for PFS Bancorp rose sharply in FY25 following the public offering and organic growth initiatives.

Business Strategy and Future Growth Prospects

Management’s strategic emphasis remains on sustained organic growth within its core market area through:

- Continuing focus on one- to four-family residential mortgage lending retained on the balance sheet for consistent yield generation.

- Expanding commercial real estate and business loan segments prudently to diversify revenue streams while maintaining tight credit standards [S5].

- Increasing low-cost core deposits (accounting for about 55% of total deposits) as a stable funding base amid competitive pressures from larger regional institutions and fintech disruptors [S5][S14].

- Potential opportunistic branching or acquisitions in adjacent markets are contemplated but not immediately planned; stock offering proceeds support flexibility for such future expansions [S15].

Challenges loom from rising interest rates compressing margins if asset repricing lags liabilities and regional economic factors impacting loan demand or asset quality [S16]. The local footprint limitation inherently restricts top-line scale economies but supports focused customer service.

Regulatory Capital Position and Risk Management

Peru Federal Savings Bank maintains regulatory well-capitalized status comfortably exceeding minimum requirements across leverage ratio (15.9%), Common Equity Tier I (33%), and Total Capital ratio (33.7%) as of December 31, 2025 [S20]. High capital levels relative to risk-weighted assets underpin resilience against credit losses or liquidity shocks.

Asset quality remains robust due to conservative underwriting practices: nonperforming assets stayed minimal at under half a percent of total assets while allowance for credit losses increased modestly alongside loan book expansion ($842K provisioned at year-end) [S17][S24]. Loan concentrations are closely monitored with exposure limits around aggregate borrower lending capped per regulatory thresholds [S19].

Liquidity is supported chiefly by customer deposits totaling approximately $166 million at year-end 2025, supplemented by access to the Federal Home Loan Bank advances line ($50 million capacity unused as of December ’25) and correspondent lines ($9 million) that can fund short-term needs if deposit withdrawals rise unexpectedly [S11][S19]. Daily monitoring aids preserving strong liquidity [S4].

Capital Allocation: Buybacks Over Dividends

PFS Bancorp has yet to pay dividends since its IPO but has demonstrated active share repurchases totaling approximately $1.33 million in fiscal year ’25 — more than twenty times the prior year amount — highlighting a shareholder value strategy focusing on stock consolidation rather than immediate yield distributions [F1][S22][S2].

The stock repurchase program was authorized for up to approximately 10% of shares outstanding at launch with ongoing open market purchases reflecting favorable valuation perceptions near recent price bands between roughly $11-$15 per share throughout ’25 [S2][S22]. Dividend policy remains contingent upon regulatory capital requirements, internal cash needs, earnings levels, and overall economic conditions.

Competitive Dynamics and Operational Risks

Operating exclusively within LaSalle County exposes PFSB to economic cyclicality more acutely than diversified regional banks benefiting from multiple industry sectors or broader geography. Housing market fluctuations directly affect predominant residential mortgage loans while competition for deposits intensifies against national banks offering digital-first solutions.

Technology infrastructure investments appear moderate—given the significant capex reduction—but cybersecurity risks remain inherent alongside third-party vendor dependencies common among community banks transitioning toward enhanced digital offerings [S16].

What To Watch: Upcoming Milestones & Indicators

- Monitor loan portfolio composition shifts particularly commercial real estate originations relative to residential mortgages for risk-adjusted yield trends.

- Deposit growth trajectory amidst evolving local economic conditions and regional competition that influences funding stability.

- Credit loss trends reflected in allowance adequacy given macroeconomic shifts potentially impacting borrowers’ repayment capabilities.

- Capital deployment decisions including further buybacks or initiation of dividend payouts tied to sustained profitability.

- Any strategic moves toward area expansion via new branches or acquisitions signaling ambitions beyond organic growth.

Conclusion

PFS Bancorp exemplifies a community bank model centered around localized relationship banking buttressed by conservative risk controls post-conversion into a public company structure just three years ago. Its promising financial momentum is underpinned by disciplined credit quality oversight coupled with focused capital returns via share repurchases rather than dividends so far.

Nonetheless, the firm confronts structural limitations owing to its constrained market area coupled with heightened competition from larger institutions leveraging technology advantages which caps upside scale potential absent strategic expansion moves in coming years.

This analysis is intended solely for informational purposes based on publicly available data as of March 26, 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments