Polyrizon Ltd. Advances Hydrogel-Based Nasal Barriers with Expanding Clinical Pipeline and Funding Challenges

Innovative nasal spray hydrogels for virus and allergen protection position Polyrizon on a novel biotech path amid regulatory hurdles and operational losses.

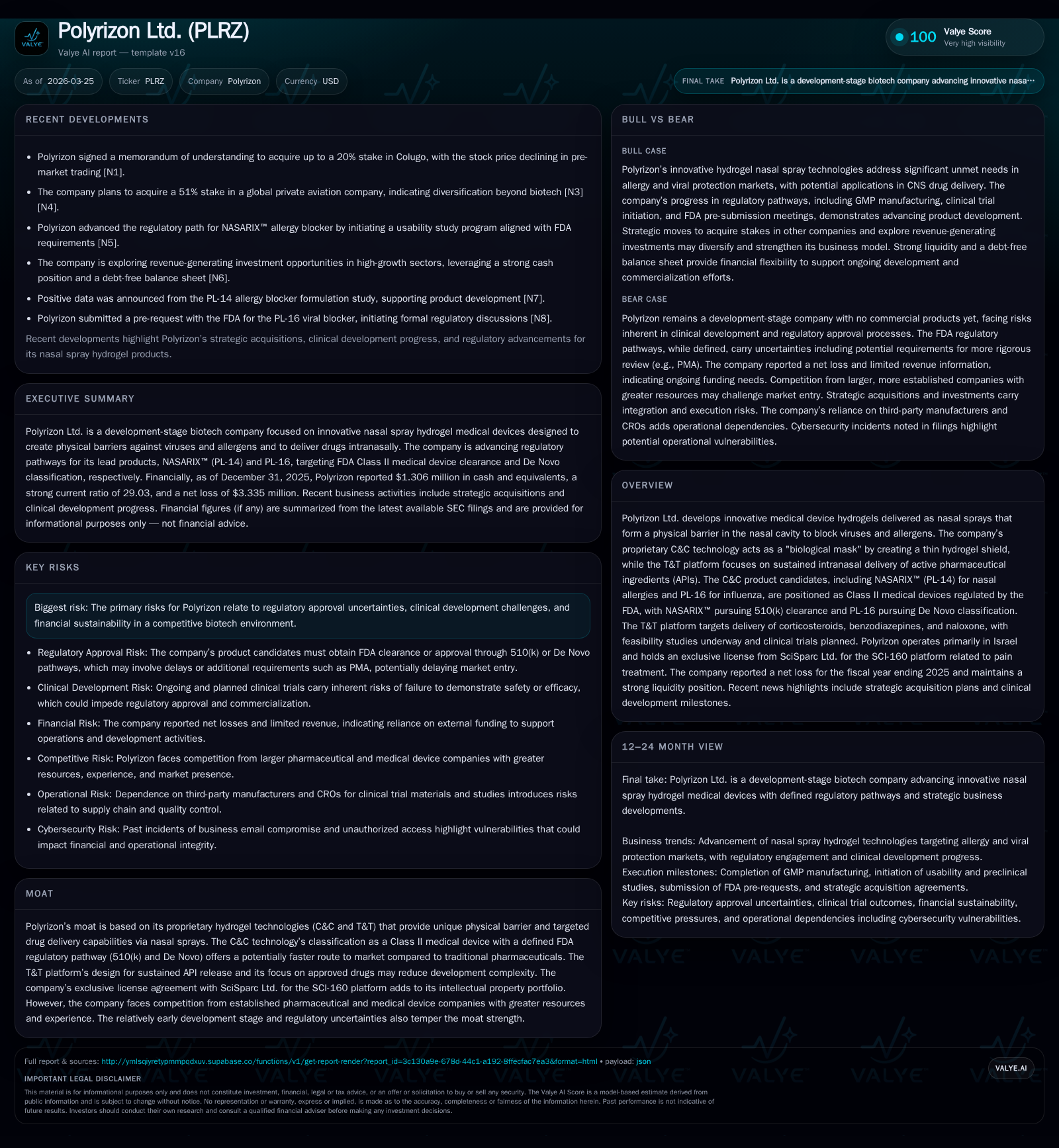

Polyrizon Ltd., an Israeli biotech firm, is developing proprietary hydrogel nasal sprays designed as physical barriers against viruses and allergens, distinguished by its C&C and T&T platform technologies. The company’s lead medical device candidates aim for FDA clearance via expedited pathways, with clinical development advancing through preclinical agreements and GMP manufacturing partnerships. Despite promising technological differentiation and intellectual property advantages, Polyrizon reports widening operating losses and negative cash flows in 2025, while maintaining a strong liquidity buffer. Near-term growth depends on successful regulatory milestones and clinical progress, tempered by competitive pressures, regulatory risks, and heightened cybersecurity vigilance.

Company Overview and Technological Differentiation

Polyrizon Ltd., headquartered in Israel since its incorporation in 2005, is at the forefront of developing innovative medical device hydrogels delivered as nasal sprays. The company's core C&C technology forms a thin protective hydrogel barrier inside the nasal cavity that physically blocks viruses and allergens—conceptualized as a "biological mask." This product line notably includes NASARIX™ (PL-14) targeting nasal allergies and PL-16 for influenza virus protection. Both products are regulated as Class II medical devices by the FDA: NASARIX™ is seeking clearance through the established 510(k) process while PL-16 is positioned under De Novo classification for novel device types.

Complementing C&C is the T&T platform aimed at intranasal administration of active pharmaceutical ingredients (APIs), such as corticosteroids (commonly used for allergic rhinitis), benzodiazepines, and naloxone (used in opioid overdose emergencies). The T&T platform's distinctive feature is sustained release capability at the deposition site within the nasal cavity—this could improve drug bioavailability compared with existing spray formulations. Currently, the company has completed feasibility studies with further clinical trials planned.

The company holds an exclusive license agreement from SciSparc Ltd. concerning the SCI-160 platform that enhances their IP portfolio surrounding hydrogel formulation technologies.

Historical Financial Performance

Operating results reflect a company still firmly within early-stage development expenditures rather than revenue generation. In fiscal year 2025, Polyrizon reported an operating loss of approximately $6.25 million, worsening from a loss of about $1.3 million in 2024—a nearly fourfold increase signaling intensifying investment in R&D activities prior to commercial launch [F1]. Correspondingly, net income declined steeply to -$3.335 million from -$1.545 million year-on-year.

Cash flow trends mimic this trajectory; operating cash flow outflows widened sharply to -$4.528 million in 2025 compared to -$1.147 million previously. Capital expenditures remain negligible ($7k vs $3k) consistent with an asset-light operations model focused more on laboratory and development outsourcing than heavy infrastructure [F1].

This investment phase increased shareholder equity significantly from $5.29 million at FY2024 year-end to $20.99 million by FY2025 close, suggestive of capital raises during the period to fortify balance sheet strength.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -3 | -5 | -6 | 7000 | -115.9% |

| 2024 | -2 | -1 | -1 | 3000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -5 | -15.9 |

| 2024 | -1 | -29.2 |

Source: SEC companyfacts cache [F1].

Numbers reflect intensified R&D spend ahead of clinical milestones[F1]

Growth Drivers and Future Prospects

The company's near-term growth catalysts hinge critically on advancing its clinical programs along regulatory pathways:

- The pursuit of FDA clearance for NASARIX™ via 510(k) alongside De Novo submissions for PL-16 represent accelerated routes favorable to medical devices versus traditional pharmacologics.

- Preclinical collaboration inked with a leading global contract research organization (CRO) supports scaling experimental validation essential for regulatory filings [S2].

- Manufacture of clinical trial material under Good Manufacturing Practices (GMP), through Eurofins CDMO AmatsiAquitaine S.A.S., evidences progression towards U.S.-based clinical trials [S3].

- Pipeline expansion including acquisition interest in Colugo—with MoU signed for up to a 20% stake—may broaden technology reach or synergize product offerings but introduces integration risks highlighted by market reactions [N1].

Challenges potentially curbing growth include uncertainties intrinsic in regulatory approvals where deviations or additional data requests could delay timelines or drive up costs [S19]. Competitive forces intensify pressure particularly from entrenched pharmaceutical companies dominating intranasal therapeutics markets who benefit from scale advantages in manufacturing and global commercialization [S17].

Regulatory Landscape and Risks

Polyrizon’s chosen FDA classification pathways offer expedited review relative to standard drug approvals but do not insulate it from complex compliance demands:

- The company must navigate rigorous FDA oversight encompassing preclinical GLP studies, IND enabling studies prior to human trials, cGMP manufacturing inspections as well as post-market surveillance once cleared [S19][S21].

- Compliance with evolving healthcare fraud prevention frameworks such as Anti-Kickback statutes and False Claims Act presents operational vigilance requirements; inadvertent breaches can lead to severe financial penalties or exclusion from federal reimbursement programs .

- State-level drug pedigree laws mandating full supply chain traceability add layers of administrative burden.

- Cybersecurity enhancements have been prioritized after incidents of fraudulent wire transfers exploiting management email accounts surfaced in late 2025—the company responded swiftly with improved transfer verification protocols overseen by audit committee governance [S15].

Capital Allocation and Liquidity Position

Despite operating at a net loss reflecting its development stage focus, Polyrizon maintains a sturdy liquidity cushion:

- Cash & equivalents stood at approximately $1.31 million at year-end 2025 while current assets totaled $12.86 million against modest current liabilities around $443k delivering an extremely conservative current ratio exceeding 29x—indicative of solid short-term fiscal health [F1].

- The rise in equity signifies recent capital injections likely utilized to finance expanded R&D efforts without resorting heavily to debt—indeed no indications of significant leverage are noted.

- There were no dividends or share buybacks reported as of latest filings consistent with standard biotech practice during development phases.

- Return on equity runs negative (-15.9%) due largely to net losses but is not unexpected given absence of product commercialization currently [F1][S20].

Free cash flow remains negative hovering near -$4.53 million underscoring ongoing dependence on external financing until revenue streams emerge.

Competitive Dynamics

Polyrizon competes within two segments:

Nasal Barrier Devices (C&C Technology)

Competitors range from companies marketing classical physical protective measures such as face masks to other firms offering nasal sprays intended as barriers against allergens/viruses. Key attributes distinguishing Polyrizon include non-drip formulations that do not irritate mucosa coupled with extended retention covering relevant nasal epithelial tissue zones—a usability advantage fostering patient adherence.[S17]

Intranasal Drug Delivery (T&T Platform)

This space is crowded by established pharmaceutical giants producing intranasal corticosteroids favored in allergic rhinitis management like Sanofi or GlaxoSmithKline products.[S17] Polyrizon’s value proposition centers on enhancing bioavailability via sustained release mechanisms which if clinically validated could carve out niche segments.

However scalability challenges exist given these incumbents' expansive marketing channels as well as R&D budgets dwarfing those available to Polyrizon.

Operational Footprint and Governance Highlights

Core operations remain Israeli-centric including R&D labs located in Raanana under month-to-month leases reflecting lean fixed-cost structures adequate for near future requirements [S23]. Cybersecurity governance features dedicated external IT consultancy layered beneath audit committee oversight ensuring rapid management escalation upon incident detection; controls around wire transfers tightened substantially post late-year criminal fraud attempts thwarted without material business disruption [S15][S1].

What To Watch Forward (Analysis)

Key milestone indicators shaping Polyrizon’s trajectory include favorable FDA determinations regarding its device submissions (NASARIX™ clearance or De Novo approval for PL-16), successful initiation of clinical trials supported by manufacturing readiness demonstrated through GMP processes confirmed by Eurofins partnership,[S2][S3] progression or completion of pivotal feasibility studies under T&T platform, and any evolving strategic partnerships or financing events following recent partial Colugo stake MOU announcements[N1]. Regulatory clarity surrounding federal pricing reforms or state-level reimbursement policies may also impinge on market entry potential.[S11][S13]

Financially monitoring narrowing operational deficits balanced against available liquidity will provide insights into funding runway adequacy amid plunging stock price reactions signaling market sensitivity around near-term corporate developments.

Conclusion

Polyrizon represents an emerging growth biotech focused on novel hydrogel-based nasal devices combining medical device regulatory pathways with innovative API delivery adjuncts heralding an unconventional entry route into respiratory protection markets. While technological uniqueness offers differentiation amid strong underlying competitive pressures led by pharma incumbents,the firm’s strategy hinges heavily on successful regulatory navigation more so than near-term commercial revenues evident from widening losses paired with stable ample liquidity. Vigilant execution of planned clinical milestones alongside prudent governance over cybersecurity risks will be pivotal components determining whether Polyrizon can translate its scientific innovations into viable market offerings within compressed timelines dictated by health emergency imperatives.

This analysis is based solely on publicly available information including SEC filings and recent press releases provided through March 25th 2026 without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments