USBC, Inc.: Tokenized Deposits and the Road to Commercial Launch

USBC is advancing its blockchain-based tokenized deposit product through strategic partnerships and pilot testing while managing regulatory and financial challenges.

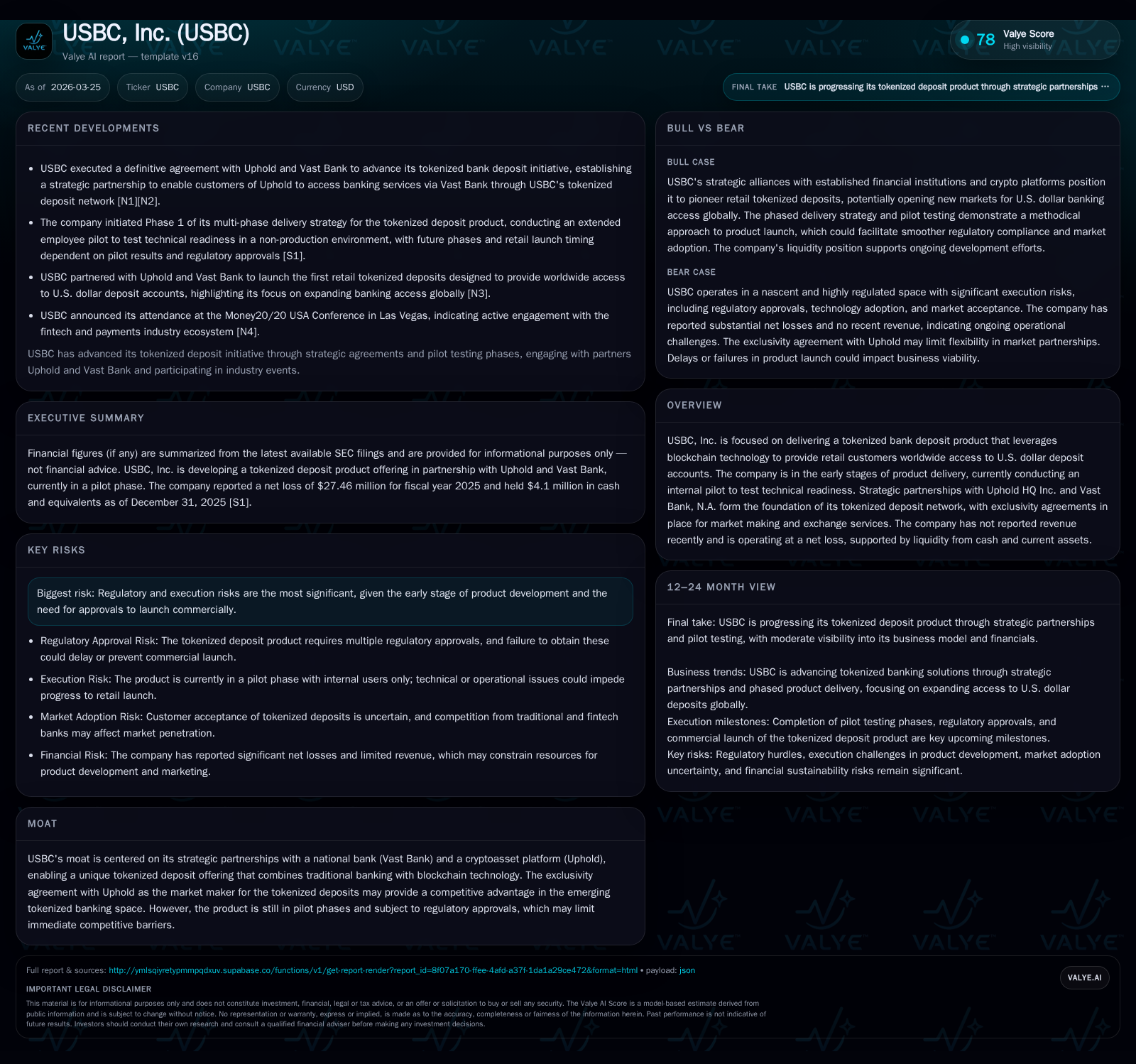

USBC, Inc. remains an early-stage fintech innovator focused on delivering U.S. dollar tokenized deposit accounts globally. Despite no current revenue and ongoing net losses driven by platform development investments, the company leverages exclusive strategic partnerships with Vast Bank and Uphold to create a unique tokenized banking ecosystem. Internal pilot testing initiated in early 2026 aims to validate technical readiness prior to commercial launch, which remains contingent on regulatory approvals. Financially, USBC maintains liquidity but continues operating with negative cash flow and an elevated burn rate, underscoring the cautious capital allocation approach critical during this development phase.

Early Growth Dynamics: An Overview of USBC’s Historical Financial Performance

USBC’s financial history portrays a fintech entity deep into development investment rather than commercial revenue generation. The company recorded modest revenue of approximately $121,939 in FY2020 followed by a sharp increase to nearly $4.36 million in FY2022, after which revenue dropped back to zero by FY2023 as USBC transitioned fully into building its tokenized deposit infrastructure [F1]. Operating income has been persistently negative—signaling substantial expenditures related to platform development—expanding from -$12.57 million in FY2022 to roughly -$17.13 million in FY2025 [F1]. Net income follows this trend with deepening losses, reaching -$27.46 million at the end of 2025.

Operating cash flow similarly reflects heavy burn rates typical for emerging blockchain fintech players during pilot phases, registering negative values that peaked near -$12.83 million in FY2024 before improving modestly to around -$4.63 million in FY2025 [F1]. Capital expenditures remain minimal recently, indicating a shift toward optimizing existing technology assets rather than expanding physical infrastructure.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -27 | -5 | -17 | -65.6% | ||

| 2024 | -17 | -13 | -15 | -8.5% | ||

| 2023 | 0 | -15 | -10 | -14 | -100.0% | +23.8% |

| 2022 | 4 | -20 | -7 | -13 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -5 | -33.7 |

| 2024 | -13 | 769.0 |

| 2023 | -10 | -408.4 |

| 2022 | -203.5 |

Source: SEC companyfacts cache [F1].

The financial trajectory aligns with typical early-stage blockchain platform ventures prioritizing technical readiness over immediate monetization.

Strategic Partnerships as the Cornerstone of USBC’s Product Architecture

USBC’s business model revolves fundamentally around two exclusive alliances: one with Vast Bank, N.A., a nationally chartered bank providing traditional banking capabilities; the other with Uphold HQ Inc., a cryptoasset platform serving as the sole market maker and exchange for the company’s tokenized deposits post-launch [S3][S7]. This exclusivity creates high entry barriers for competitors owing to regulatory constraints around banking relationships tied to digital asset issuance.

These partnerships integrate liquidity provisioning from Uphold’s platform with Vast Bank’s regulated banking services—enabling retail customers access to U.S. dollar-denominated accounts via tokenization on a blockchain network operated by USBC [S7]. The Agreement signed in January 2026 ensures Uphold remains the exclusive crypto-market entity for these tokenized deposits throughout the initial term starting from commercial launch onward with renewals annually unless terminated according to contract terms [S7].

This arrangement positions USBC uniquely at the intersection of traditional regulated banking and emerging decentralized finance infrastructure—a competitive moat anchored not only in technology but also deeply within regulated banking ecosystems.

Tokenized Deposit Pilot: Technical Readiness Tested Inside the Company

In March 2026 USBC commenced Phase 1 of its delivery strategy: an internal pilot involving select employees testing the tokenized deposit product within a closed non-consumer environment [S8][S9]. This stage is aimed at validating core technical components under controlled settings before exposing the product to external users or regulators.

This extended employee pilot serves dual purposes: refining system stability and establishing operational readiness necessary for eventual regulatory submissions—and alignment among stakeholders including Vast Bank and Uphold [S8]. Feedback loops between engineering teams and pilot participants help identify integration issues or security controls gaps early.

Notably public consumer launch timing remains undefined; future phases hinge entirely on pilot results alongside evolving regulatory clearances—reflecting prudent sequencing amid nascent hybrid financial service models blending fiat deposits with blockchain tokens.

Navigating Regulatory Headwinds: Risks Impacting Market Deployment

USBC confronts significant regulatory uncertainties common to fintech firms attempting innovative product launches bridging traditional finance (TradFi) and blockchain ecosystems [S4][S5]. Obtaining necessary banking charter approvals combined with compliance under securities laws governing digital assets poses a formidable barrier.

The company explicitly flags execution risks centered on achieving comprehensive regulatory clearance prior to general rollout—compounded by fragmentation in crypto-asset oversight across jurisdictions. Its operations must comply with applicable anti-money laundering statutes as well as consumer protection frameworks applied by banking regulators overseeing Vast Bank's participation [S4][S5].

This heavily scrutinized environment requires cautious navigation where perceived non-compliance could trigger enforcement actions or delay commercialization indefinitely.

Capital Allocation and Financial Health: Cash Flow, Equity Positioning and Shareholder Returns

At fiscal year-end 2025 USBC held approximately $4.1 million in cash equivalents supported by total current assets near $6.79 million against current liabilities close to $3.68 million—yielding a current ratio of about 1.85 consistent with sufficient short-term liquidity coverage despite ongoing operational deficits [F1].

Operating cash flows remain negative but improved significantly from nearly -$12.8 million in FY2024 down to roughly -$4.6 million in FY2025 reflecting tighter expense controls or efficiency gains despite continued investments required for platform development [F1]. Capital expenditures are negligible most recently indicating focus on software development versus physical asset outlays.

No dividends or share repurchases have been initiated; however management approved repricing of approximately 83 million stock options at market prices intended to retain executives and directors amid long-duration product maturation cycles—a retention mechanism during persistent losses [S15].

USBC's approximate return on equity was negative at about -33.7% for FY2025 due to continuing net losses relative to equity base expansion from financing activities and retained capital [F1].

Outlook: Key Milestones and Growth Considerations Ahead

While specific revenue forecasts or launch dates remain undisclosed publicly due to ongoing pilot status [S8], key inflection points include:

- Successful completion and evaluation of Phase 1 internal pilot testing;

- Advancement into subsequent delivery phases permitting limited external user onboarding;

- Receipt of all requisite regulatory approvals from banking authorities;

- Board-level endorsements regarding program expansion;

- Announcement of commercial launch availability for retail customers.

Future growth hinges on successful pilot outcomes validated through rigorous testing; regulatory clearance amidst evolving legal frameworks; scalable user adoption driven by partner ecosystem expansion beyond Uphold; and sustained capital discipline during commercialization ramp-up.

Investors should monitor SEC filings and official corporate disclosures for updates impacting timing assumptions around scaling growth trajectory.

Analysis based solely on information available as of March 25th, 2026 combining company filings ([F1], [S#]) without projecting investment advice or forecasts beyond stated sources.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments