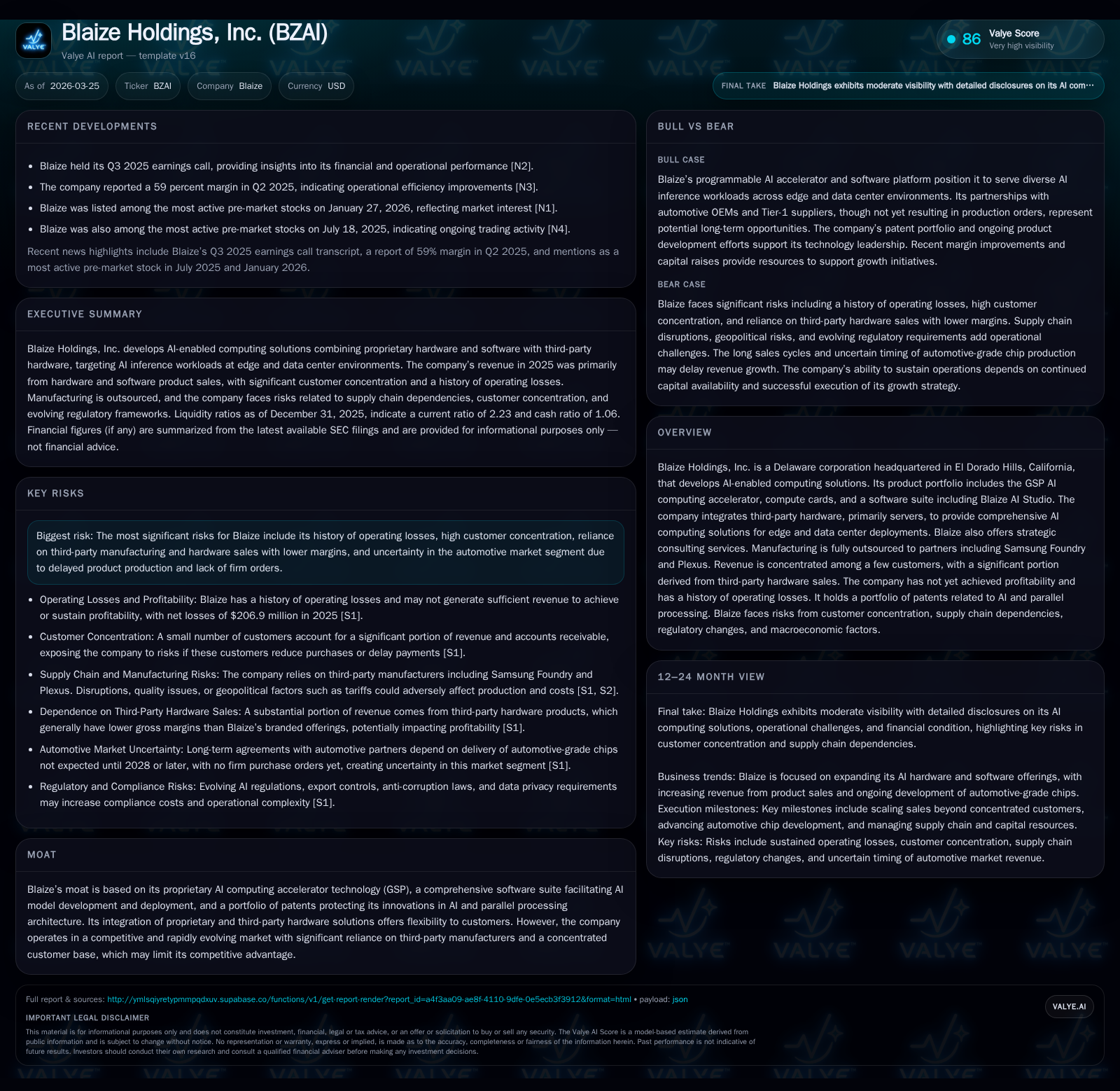

Blaize Holdings’ Revenue Concentration and Operating Losses Challenge Growth Amid AI Edge Computing Evolution

Blaize Holdings faces steep operating losses, concentrated customer revenue, and supply chain dependencies while developing AI-enabled computing solutions.

Blaize Holdings, a developer of AI accelerator hardware and software solutions, has built its moat around proprietary GSP chips, a comprehensive AI software suite, and selective integration of third-party hardware. Despite revenue growth driven largely by third-party hardware sales from a few major customers—most notably in China—the company has not achieved profitability and reported a steep increase in losses in 2025. Its capital-intensive roadmap includes expanding into automotive-grade chips, yet customer concentration, manufacturing reliance on partners like Samsung Foundry, and delayed contract milestones constrain visibility on future growth. Blaize’s cash position offers some runway but substantial risks to margins and execution remain amid fierce competition and evolving AI market demands.

Company Overview

Blaize Holdings, Inc., incorporated in Delaware and headquartered in El Dorado Hills, California, specializes in AI-enabled computing solutions optimized for edge and data center environments [S1][S10]. Its product portfolio centers on the proprietary Graph Streaming Processor (GSP) accelerator chip engineered for highly parallel AI workloads such as computer vision and machine learning. The GSP supports extensive programmability and efficient data streaming mechanisms aimed at low-power, high-performance inference processing [S10]. Complementing the GSP are compute cards in industry-standard form factors and a broad software suite branded Blaize AI Studio—a visual no-code or low-code platform designed to simplify AI model creation and deployment [S10].

Beyond its internally developed products, Blaize also integrates third-party hardware components—mainly servers—to provide fully integrated AI compute solutions tailored to customer needs. This hybrid approach aims to leverage partner offerings while retaining differentiation through proprietary technology [S10]. Manufacturing is outsourced entirely to partners such as Samsung Foundry (semiconductor wafers) and Plexus (assembly/testing), placing the company at risk of supply chain disruptions beyond its direct control [S2][S10].

Historical Performance

While Blaize has steadily expanded its presence since its formation in 2010 and became publicly listed after a reverse recapitalization via SPAC merger completed January 2025 [S1], it has operated at significant net losses throughout recent years.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -207 | -74 | -104 | -4929.8% |

| 2024 | -4 | -3 | -5 | -407.2% |

| 2023 | 1 | -2 | -3 | -20.0% |

| 2022 | 2 | -1 | -2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -530.5 |

| 2024 | 17.6 |

| 2023 | -8.5 |

| 2022 | -16.5 |

Source: SEC companyfacts cache [F1].

Note: Revenue data was not fully disclosed; quarterly revenue of approximately $11.9 million was reported for Q3 2025 [F1][S1].

The standout issue is the dramatic increase in operating losses—from about $5 million negative in fiscal 2024 to nearly $104 million negative in fiscal 2025—reflecting expansion costs tied to product development, marketing effort intensification, and operational scaling without corresponding uplift in revenues [F1]. Likewise, net income deteriorated sharply into negative territory exceeding $200 million.

Cash flow from operations remains negative at roughly $74 million for FY2025 amid continued investment outlays in R&D and sales, constraining free cash flow. The company carries positive equity as of year-end due partially to capital raises but faces ongoing cash burn challenges [F1].

Revenue Drivers and Customer Concentration

Blaize's revenues are dominated by sales of third-party hardware products comprising mainly servers hosting Blaize technology platforms as well as their own branded chipset-based cards [S4][S15]. These third-party hardware sales generally yield lower gross margins relative to Blaize’s own GSP-enabled offerings.

Customer concentration is acute: two non-related Chinese customers accounted for around 88% (61% + 27%) of total revenues in fiscal-year 2025, marking a geographic shift from prior years when revenue was centered among U.S.-based related parties primarily engaged through strategic consulting services that have since expired [S4][S5][S6][S7]. Such dependence exposes Blaize materially to changes or loss of orders from these customers.

Additionally, accounts receivable balances are similarly concentrated posing credit risk, particularly given potential geopolitical trade tensions impacting cross-border operations involving China [S4][S7][S14].

The long sales cycles typical with large enterprise clients combined with the need for substantial product qualification contribute further uncertainty in revenue predictability [S12].

Growth Prospects

Management expects potential future growth from multiple vectors including:

- Expanding the ecosystem integrating both proprietary hardware/software and third-party server solutions.

- Increasing adoption within existing customer base while acquiring new enterprise clients globally.

- Developing an automotive-grade chip intended for Advanced Driving Assistance Systems (ADAS) applications with anticipated production commencing no sooner than calendar year 2028—critical purchase orders remain contingent on chip delivery [S25].

- Enhancing AI Studio capabilities to drive easier deployment of generative AI use cases targeting edge deployments [S18][N/A].

Execution risks around these prospects remain significant due to competitive pressures, customer concentration constraints, delays inherent in automotive segment maturation, reliance on outsourced manufacturing capacity, and capital intensity involved with continuous R&D investment [S8][S16][S19][S21].

Forecasts & Milestones

While specific numerical guidance is not explicitly disclosed within filings or news sources provided here, watchers should monitor:

- Progress toward qualification and production milestones for automotive-grade chips.

- Growth trends in branded hardware versus third-party hardware sales mix impacting gross margins.

- Expansion or diversification of customer base beyond top two Chinese customers.

- Capital raising activities or equity issuance under B. Riley equity facility indicating liquidity status [S11][S13][S27].

Absent firm contracts or visible pipeline maturation signals detailed timing remains opaque.

Returns & Capital Allocation

Blaize does not pay dividends and has no current plans to initiate dividend distributions; shareholder returns rely solely on stock-price appreciation potential which remains uncertain given sustained losses [S26].

Capital allocation is directed largely toward R&D spend as well as sales and marketing to scale market presence which depresses near-term profitability despite long-term upside ambitions [F1][S18].

Equity capital raising via a common stock purchase agreement with B. Riley provides up to $50 million in financing capacity over about three years; thus far approximately $33 million has been raised through this channel supporting ongoing operations but entails dilution risks for shareholders [S11][S13][S27].

The substantial negative return on equity (~ -530%) signals inefficient capital use currently driven by steep net losses relative to modest positive equity capital base as of end FY2025 ([F1]).

Competitive Environment & Risks

Blaize competes amidst deep-pocketed established players addressing edge-AI compute markets who benefit from scale economies, extensive IP portfolios, broader product lines spanning CPU/GPU/ASIC accelerators paired with mature ecosystems [S12]. Market dynamics are fast evolving with rapid technological progress demanding constant innovation alongside pricing pressures.

Key risks include:

- Customer concentration limiting revenue stability.

- Supply chain interruptions stemming from outsourced manufacturing dependencies.

- Delay or failure in advancing next-generation chips timely enough to meet client demands.

- Legal/regulatory compliance challenges across international jurisdictions including IP protection complexities surrounding AI technology.

- Potential impacts from geopolitical tensions affecting cross-border operations especially vis-à-vis China.

- Operating cash burn requiring consistent access to capital markets under market-sensible terms.

- Uncertainty around realization of automotive segment revenue given long timelines before ADAS deployment commercialization [S8][S19][S20][S22][S24].

Conclusion & What To Watch Next

Blaize Holdings stands at an inflection point balancing cutting-edge innovation against operational execution hurdles common among emerging AI hardware-specialists transitioning beyond early adopter phases into commercial scale deployments.

Monitoring upcoming quarterly report disclosures will be critical for insights on shifts away from an overreliance on third-party hardware sales toward more profitable branded product revenue expansion; updates on automotive-grade chip development progress; key customer diversification efforts; supply chain stability; and cash flow trends vis-à-vis fundraising activities under committed equity facilities.

Execution discipline coupled with expanding market traction across broader customer bases will shape the sustainability of Blaize's business model amid intense sector competition.

This analysis synthesizes publicly available SEC filings as of March 24, 2026 ([F1],[S1]-[S29]) without speculative forward-looking financial metrics or investment recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments