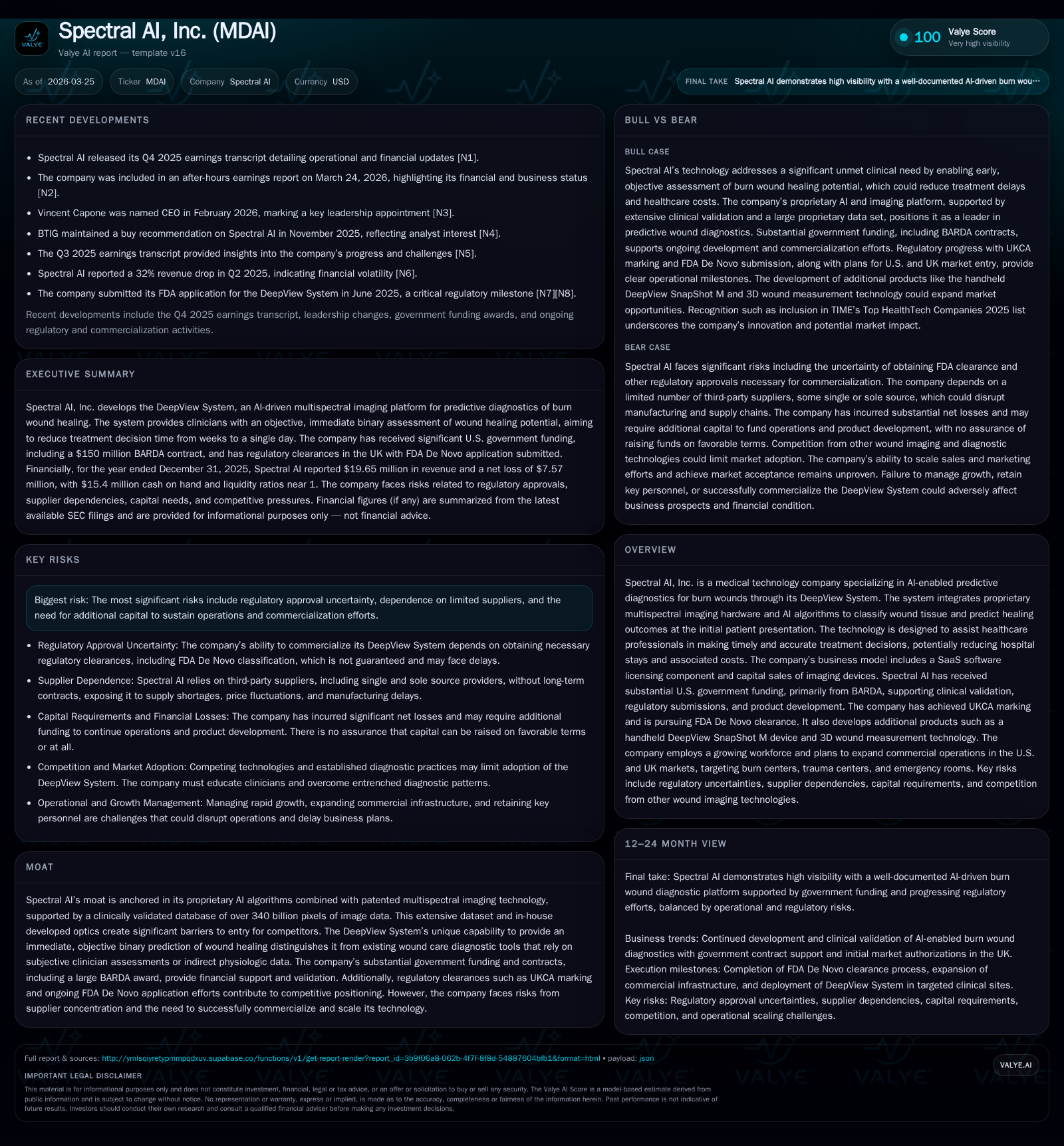

Spectral AI’s Burn Diagnostic Growth Hinges on FDA Clearance and Capital Infusion

Spectral AI specializes in AI-powered multispectral imaging for burn wound assessment, with recent UK approval and ongoing FDA De Novo pursuit.

Spectral AI, Inc. has demonstrated volatile revenue growth over recent years driven by government contracts and technology development in AI-based burn diagnostics. The company’s proprietary DeepView System achieved UKCA marking in early 2024 and is advancing FDA regulatory clearance with a De Novo application submitted in mid-2025. Despite growing revenues to $19.65 million in FY2025, losses remain substantial, underpinned by high R&D and commercialization costs. Its moat stems from proprietary AI algorithms combined with patented multispectral imaging hardware supported by extensive clinical data. Future growth depends heavily on regulatory approvals, successful commercialization execution, and additional capital availability amid supplier dependency and intensified competition.

Business Overview and Technology

Spectral AI, Inc. distinguishes itself as a medical technology company leveraging artificial intelligence integrated with proprietary multispectral imaging (MSI) hardware to provide predictive diagnostics for burn wounds. At its core is the DeepView System, an innovative platform melding patented MSI optics capable of capturing wavelengths beyond human vision—from near ultraviolet through visible light into near infrared—with advanced AI algorithms trained on a vast clinical dataset exceeding 340 billion pixels of tissue imagery [S1]. This combination enables an immediate binary prediction assessing whether a burn wound will heal within a predefined timeframe upon initial patient presentation.

This diagnostic insight aims to support healthcare professionals in making more accurate, timely decisions regarding treatment plans for burns—a notoriously difficult clinical challenge due to subjective visual assessments traditionally employed. The system processes image acquisition ultra-rapidly (0.2 seconds) and completes AI classification within approximately 20–25 seconds, producing overlays highlighting non-healing tissue portions alongside original images.

Historical Financial Performance

Over the past four fiscal years ending 2025, Spectral AI’s revenue trajectory has shown significant fluctuations influenced by technology development stages and contract funding cycles, particularly from U.S. government agencies such as BARDA. Revenues rose sharply from $18.06 million in FY2023 to a peak of $29.58 million in FY2024 before retracting by 33.6% to $19.65 million in FY2025 [F1]. Operating losses remained deeply negative during this period but improved from a high-water mark loss of approximately $13 million in FY2023 to $8.6 million loss in FY2025.

The net income picture mirrors operating performance yet features exceptionally volatile swings: positive net income recorded once in FY2022 at just over $11 million was followed by steep losses thereafter, albeit improving by over 50% year-over-year to a nearly $7.57 million deficit last fiscal year [F1]. Operating cash flow has consistently been negative since at least FY2022 due to sizable R&D expenses and scaling efforts.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 20 | -8 | -10 | -9 | -33.6% | +50.6% |

| 2024 | 30 | -15 | -9 | -7 | +63.8% | +26.6% |

| 2023 | 18 | -21 | -13 | -13 | -288.9% | |

| 2022 | 11 | -1 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 132.2 |

| 2024 | 211.2 |

| 2023 | 1220.2 |

| 2022 | -91.3 |

Source: SEC companyfacts cache [F1].

Note: Revenue YoY % compares current fiscal year revenue against prior fiscal year; Net Income YoY % is the comparable change.

Competitive Position and Moat

Spectral AI’s moat centers on its unique fusion of patented MSI technology plus homegrown AI algorithms validated extensively via its proprietary clinical image database of unmatched scale (>340 billion pixels). This technical barrier sharply limits competitors’ ability to replicate similar diagnostic precision or speed [S7][S15]. Furthermore, the DeepView System’s output—a binary prognostic indicator at initial visit—is distinct from conventional methodologies relying predominantly on subjective clinician assessments or indirect physiological measures.

However, the company operates within a mature wound care diagnostics market featuring established competitors with entrenched clinical relationships and broader portfolios that may leverage bundling or discounting strategies to defend market share [S7]. Gaining physician acceptance will require overcoming ingrained diagnostic habits through extensive education efforts.

Regulatory Status and Milestones

Regulatory progress forms a critical catalyst for Spectral AI’s commercial ramp:

- The DeepView System secured United Kingdom Conformity Assessed (UKCA) marking for burn indications as of February-March 2024, endorsing safety and effectiveness per UK standards and enabling sales in this jurisdiction [S1].

- In June 2025, Spectral filed a pivotal FDA De Novo application seeking Class II medical device designation allowed under US regulations for novel devices without predicate equivalents [S1]. Approval here would vastly broaden US commercial opportunities beyond research or limited use environments.

- A conditional second tranche of Avenue Capital Group debt hinges explicitly on this FDA clearance alongside raising a fresh $7 million equity round by management-defined thresholds [S8][S20].

This regulatory pathway underscores both opportunity—enabling scalable go-to-market options—and risk given inherent uncertainties around timing and ultimate classification outcome.

Growth Prospects and Operational Strategy

Post-approval revenues will likely derive from two streams: (i) SaaS licensing fees under software-as-a-medical-device frameworks offering algorithm updates, maintenance, image hosting; (ii) capital equipment sales of the MSI imaging hardware platform serving as universal interface potentially expandable beyond burns toward other tissue indication diagnostics [S1]. Pricing will differ strategically by geography and site-of-service considerations to optimize adoption dynamics.

Additional BARDA funding commitment totaling $31.7 million supports ongoing clinical validation activities paramount to evidentiary sufficiency during regulatory reviews while bolstering operational runway through early commercialization phases [N3].

Despite these avenues, constraints remain:

- Market penetration requires iterative user education against entrenched traditional approaches.

- Scale-up depends on securing diversified manufacturing capabilities beyond current single-supplier exposure reducing potential bottlenecks seen across medtech supply chains globally post-pandemic disruptions [S4][S24].

- Regulatory conditions may evolve as authorities continue refining oversight over emerging AI technologies adding complexity around compliance costs [S21].

Financial Condition and Capital Allocation

As of December 31, 2025, cash & equivalents stood at approximately $15.4 million—sufficient combined with anticipated BARDA funds and debt capacity under existing multi-year agreements to finance operations for at least the subsequent twelve months barring unanticipated expenditure surges or slower-than-expected market traction [F1][S8][S20].

Operating cash flows remained negative near $10 million last fiscal year indicating ongoing investment mode primarily funding R&D rather than profitability generation so far [F1]. Equity stood at a deficit reflecting accumulated losses consistent with sector patterns among early-stage medtech innovators deploying capital aggressively ahead of commercial breakeven milestones [F1].

No dividends or share repurchases have been reported given the company’s current focus on capital preservation amid ongoing development efforts.

Risks Summary

Principal risks span regulatory approval uncertainty—including potential delays or denials impacting available financing tranches—supplier concentration exposes manufacturing continuity vulnerabilities aggravated by component specificity of MSI optics assembly chains known for long lead times [S4][S10][S24]. Additional capital raises are likely needed beyond current financing arrangements if commercialization ramp deviates from internal forecasts placing pressure on valuation metrics or ownership dilution profiles. Product liability exposures inherent in medical devices treating ill patients could prompt costly litigation despite insurance protections given reputational stakes present another headwind especially considering newness of technology domains involving automated predictions requiring user training diligence [S4][S18][S19]. Lastly, rapid shifts in regulatory frameworks around AI technology deployment may compel unforeseen compliance adaptations imposing material operational burdens disproportionate to company size presently operating on slender margins unsecured by sustainable profit streams yet [S21].

What to Watch Going Forward

Key next milestones include:

- Outcome timeline on FDA De Novo decision anticipated sometime after mid-2026; any delays or requests for additional data could stall capital deployment timing.

- Execution progress on expanding clinical trial sites underpinning real-world evidence generation aligned with payer dossier development facilitating future reimbursement evaluations.

- Scaling manufacturing capabilities mitigating supplier risks along with robust quality control processes vital for post-market surveillance demands enforced by regulatory agencies worldwide declining tolerances for non-conformances impacting patient safety.[N1]

- Ability to complete contingent equity raises underpinning tranche releases from Avenue Capital lenders—the success there signals external confidence boosting partnership prospects among strategic buyers or OEM collaborations expanding channel reach.

- Progress toward diversifying product indications leveraging universal MSI platform positioning beyond burns could uncover material incremental addressable market opportunities enhancing valuation narratives when matured.[N2]

Conclusion

Spectral AI operates at the intersection of AI-driven diagnostics and specialized optical engineering addressing a clinically challenging area where objective predictive capability meets unmet medical needs. While its foundational technology offers strong differentiation supported by substantial intellectual property protection and initial regulatory validations such as UKCA marking, achieving profitable scale hinges critically on navigating complex US FDA pathways successfully amidst intense competition meeting clinician adoption hurdles coupled with sufficient liquidity management amidst capital-intensive development cycles. Investors should monitor regulatory developments closely along with execution evidence regarding capital raises and manufacturing robustness as these constitute principal levers influencing future operational sustainability absent explicit profitability guidance currently disclosed.[F1][N3] This analysis is informational only without investment recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments