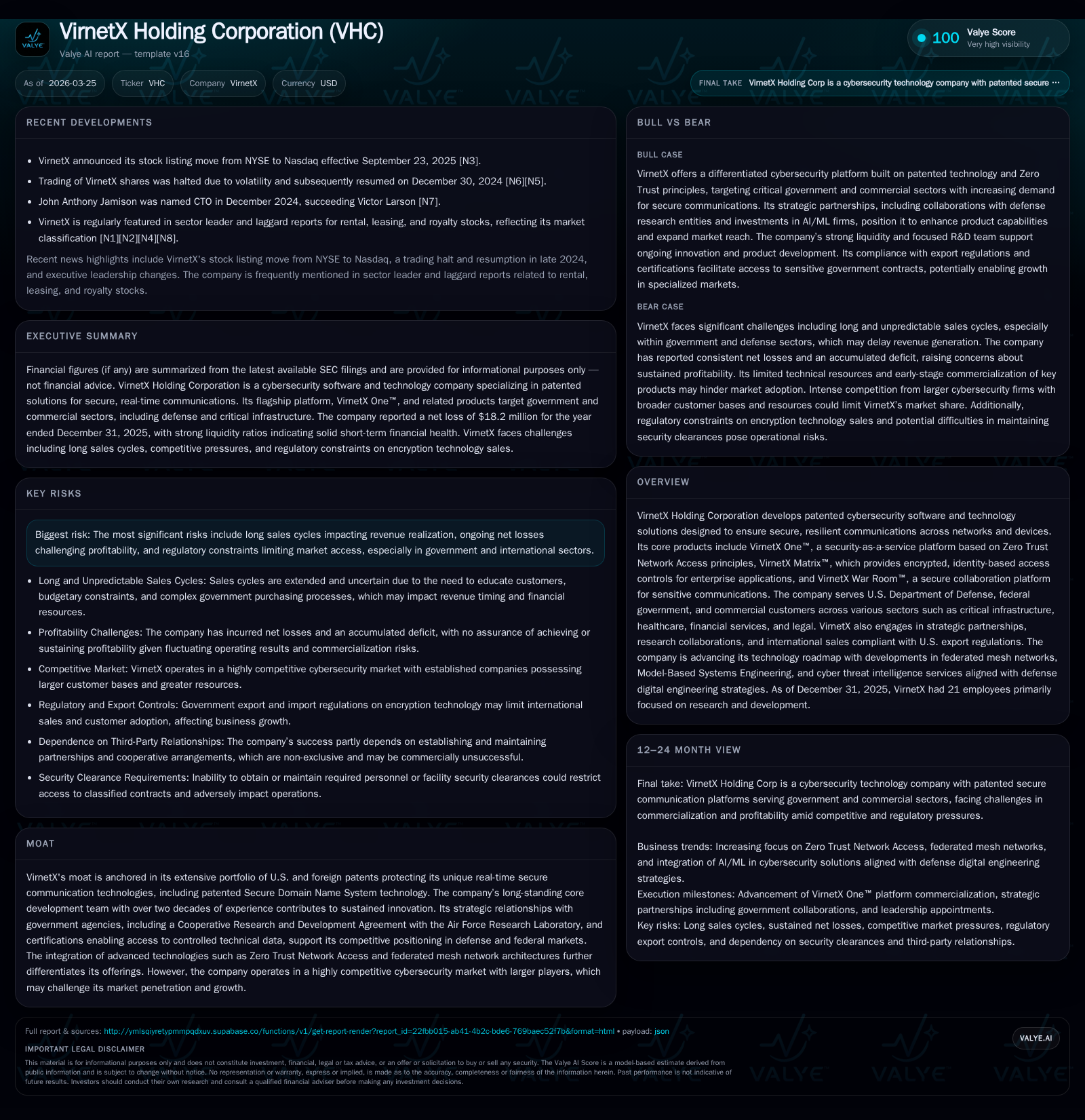

VirnetX Holding: Patent-Backed Cybersecurity Growth Constrained by Persistent Losses and Lengthy Sales Cycles

VirnetX leverages patented secure communication technologies targeting government and enterprise clients but faces earnings volatility amid competitive pressures.

VirnetX Holding Corporation centers its business on patented cybersecurity software platforms emphasizing real-time secure communications, primarily serving the U.S. government and critical industries. Despite steady R&D investment and expanding product suites like VirnetX One™, Matrix™, and War Room™, the company has operated at a net loss for several years, influenced by long sales cycles and intense competition. Its sizable patent portfolio reinforces a unique moat, yet profitability and operating cash flow remain challenged. Monitoring future milestones around enterprise adoption, partnership expansion, and technology roadmap execution is essential to assess growth trajectory.

Company Overview

VirnetX Holding Corporation is a specialized cybersecurity software developer whose core value proposition revolves around patented technologies enabling resilient, real-time secured communications across various network environments. Its flagship platform, VirnetX One™, implements Zero Trust Network Access (ZTNA) principles combined with proprietary Secure Domain Name System (SDNS) technology to secure applications, devices, and infrastructure irrespective of geographic distribution or endpoint variation [S12].

The company complements this with VirnetX Matrix™, which provides encrypted identity-based access control targeted at securing enterprise applications without substantial infrastructure changes. Another pillar, VirnetX War Room™, addresses confidential collaboration needs frequently encountered in governmental, legal, financial, and healthcare sectors [S12].

Focused predominantly on U.S. Department of Defense agencies alongside commercial verticals such as critical infrastructure and healthcare, VirnetX also supports export-compliant international sales constrained by stringent U.S. encryption export laws [S12].

Historical Performance Drivers

VirnetX's revenue streams derive primarily from licensing patents related to its Secure Domain Name System technology and subscriptions or licenses to its cybersecurity platforms. Though direct revenue figures were not disclosed explicitly in available filings, the company reports long sales cycles particularly pronounced within government contracts due to extensive internal reviews and budgetary timing [S17][S18].

Financially, VirnetX has consistently reported net operating losses for the past four fiscal years as it invests in product development while pursuing market penetration.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -18 | -16 | -19 | 17000 | -0.3% |

| 2024 | -18 | -15 | -20 | 22000 | +34.8% |

| 2023 | -28 | -25 | -31 | 65000 | +23.1% |

| 2022 | -36 | -17 | -22 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -16 | -81.1 | |

| 2024 | 0 | -15 | -45.9 |

| 2023 | 71 | -25 | -49.8 |

| 2022 | -17 | -23.8 |

Source: SEC companyfacts cache [F1].

Source: [F1]

The company's operating income loss narrowed modestly in 2025 relative to prior years despite ongoing negative results. Operating cash flow remains notably negative reflecting cash burn intrinsic to continued R&D spending and slow license monetization.

Moat and Competitive Positioning

VirnetX’s moat is firmly anchored in its expansive portfolio of U.S. and foreign patents around SDNS and other proprietary elements forming the base of its real-time encryption capabilities [S12]. This intellectual property footprint restricts direct replication by competitors.

Complementing its technical edge are longstanding collaborations with government bodies such as the U.S. Air Force Research Laboratory via Cooperative Research Agreements that confer privileged access to classified data environments necessary for tailored cybersecurity solutions [S12].

However, the cybersecurity market segment for ZTNA platforms is intensely competitive. Service giants like Palo Alto Networks (Prisma Access), Cisco (Umbrella), Cloudflare as well as emerging security-as-a-service providers offer bundled SASE/SSE solutions that pressure VirnetX’s somewhat narrower product approach on both price points and scale [S14]. Additionally, some government customers consider developing internal ZTNA capabilities potentially reducing reliance on vendors.

Future Growth Prospects

VirnetX indicates a technology roadmap focused on federated hybrid mesh networks embedding dynamic trust evaluation and autonomous recovery to enhance network resilience — aligning closely with sector trends toward decentralized security architectures [S12]. It also pursues expanding secure network coverage into IoT and edge computing spaces through obfuscated lightweight security methods suitable for resource-constrained devices.

Growth levers include broadening adoption of VirnetX One™ among large enterprises and government entities as well as increasing integrations via third-party partnerships who resell or embed VirnetX’s capabilities into their offerings [S17][S18]. Achieving commercial traction for Matrix™ and War Room™ platforms beyond niche governmental customers would also drive incremental revenue.

Risks to growth arise from extended sales cycles inherent in public sector engagement driving unpredictability of contract wins [S17][S18], aggressive competition establishing entrenched cloud security standards impacting price acceptance [S14], regulatory export controls limiting international expansion potential [S12], plus potential shifts in demand driven by emergent disruptive technologies including generative AI [S14].

Forecasts / Milestones / Expectations

The company has not provided explicit revenue or profitability guidance publicly. Investor focus should include tracking:

- Progression of contracts won or renewed with defense agencies.

- Uptake statistics for VirnetX One™ within commercial enterprise segments.

- Development updates relating to mesh network architecture deployments.

- Expansion or establishment of reseller/service partnerships.

- Impact of regulatory changes on export/compliance frameworks.

These indicators will be critical to judging whether VirnetX can accelerate from a loss-making innovation stage toward sustained commercialization.

Financial Returns / Capital Allocation

VirnetX’s capital allocation reflects heavy reinvestment consistent with a firm prioritizing product development over shareholder distributions:

- The company recorded no dividends or share buybacks in recent years [F1].

- Capex remains minimal relative to operating expenses ($17k in FY2025), underscoring a software-centric model rather than asset-heavy operations.

- The equity base declined sharply since FY2022 mainly due to accumulated losses reducing retained earnings from over $152 million down to $22 million by FY2025 [F1].

- Approximate Return on Equity remains deeply negative (~-81% based on latest annual net income/equity), indicating lack of realized profitability despite intellectual property assets [F1].

- Operating cash flows persistently negative; free cash flow estimated at about -$15.66 million in FY2025 after capex subtraction signals continuing funding needs from capital markets or partners to sustain operations [F1].

Liquidity metrics are currently strong with the latest current ratio exceeding 10x primarily due to robust short-term cash equivalents (~$15.5 million at FY-end) versus liabilities of about $2 million [F1]. This provides a near-term buffer though not addressing medium-term profitability challenges.

Risks Summary

Primary risk factors stem from:

- Lengthy sales cycles delaying revenue inflections risking cash exhaustion before scale efficiencies materialize [S17][S18].

- Intensifying competition from better resourced incumbents offering cost-effective bundled cloud solutions jeopardizing pricing power [S14].

- Regulatory constraints restricting overseas market expansion particularly concerning encryption-tech export controls [S12].

- Potential unforeseen product errors given high technical complexity could damage customer confidence if discovered post-deployment [S19].

- Economic downturns affecting public sector budgets or private industry IT spend thereby reducing contract opportunities.

Analysis Conclusion

VirnetX Holding embodies a classic technology pioneer archetype: rich patent-derived intellectual property underpinning innovative secure communication platforms aimed at high-barrier government sectors requiring fortified data integrity under adversarial conditions. However, tangible monetization hurdles surface through prolonged contract cycles typical of defense-oriented procurement alongside stiff headwinds from larger cloud security competitors embedding ZTNA features into comprehensive service edges.

Continued investments into federated mesh architectures targeting evolving IoT/edge demands demonstrate adaptability aligned with cybersecurity’s directional shifts but must ultimately translate into improved license uptake to offset entrenched losses. Solid liquidity cushions ease short-term operational solvency concerns yet highlight imperative for strategic partnerships or possible capital infusions pending scalable revenue attainment.

Monitoring expansions into broader commercial verticals complemented by validation through partnership channels will be vital signals evidencing sustainable growth beyond government niche dominance while navigating looming technological disruption risks inherent in the dynamic cybersecurity market environment.

This analysis is intended solely for informational purposes without providing investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments