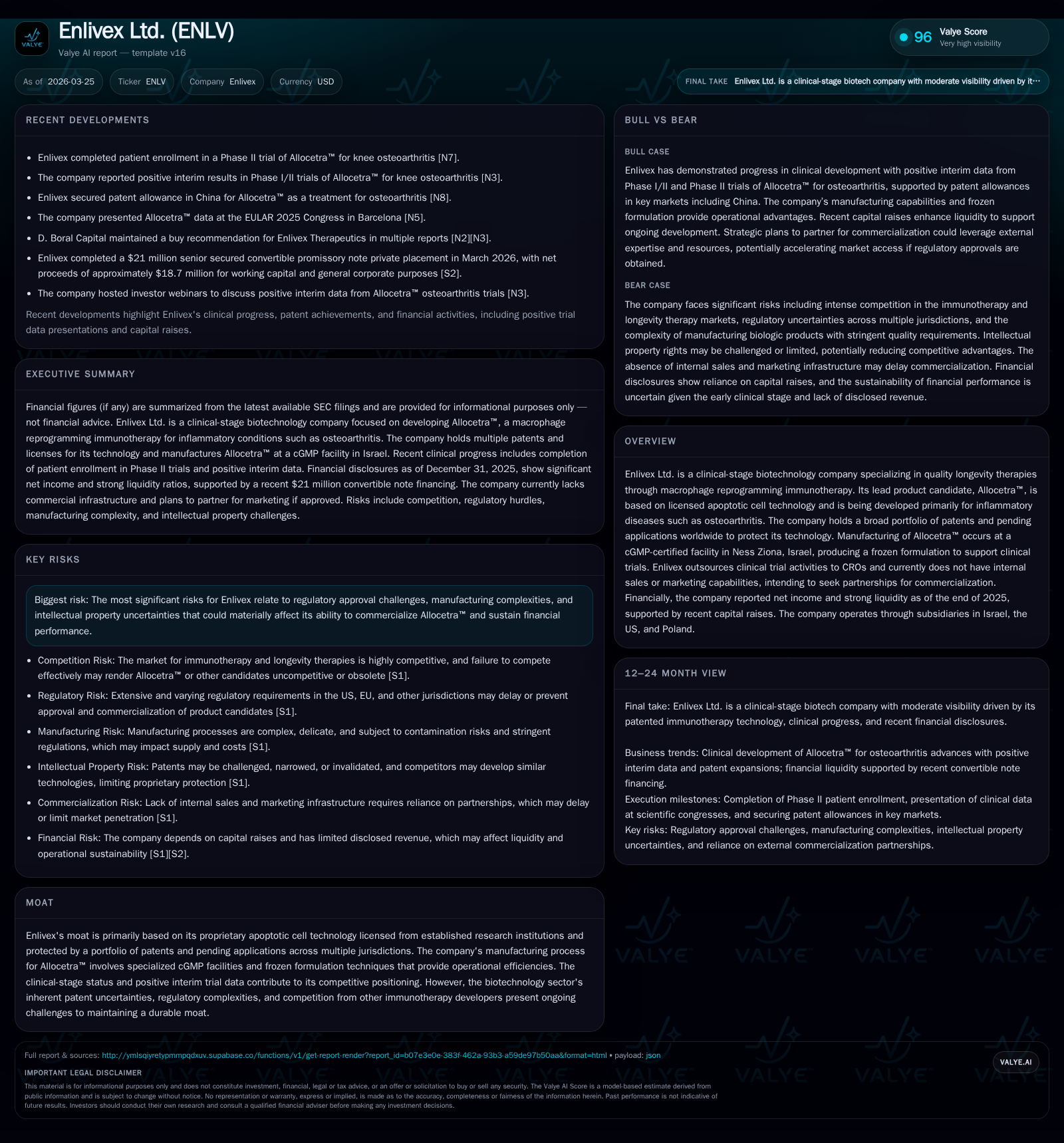

Enlivex Ltd.’s Clinical-Stage Immunotherapy Push and Financial Volatility in 2025

Enlivex leverages proprietary apoptotic cell technology to develop Allocetra™ for inflammatory diseases amid regulatory and commercialization challenges.

Enlivex Ltd. is a clinical-stage biotech focused on macrophage reprogramming immunotherapy, primarily developing its lead product Allocetra™ using licensed apoptotic cell technology. The company holds an extensive intellectual property portfolio and outsources clinical trials, with no internal sales force, seeking partnerships for commercialization. Despite posting a significant net income gain in 2025 due to non-operating factors, operating losses and negative cash flows highlight ongoing funding needs as clinical development progresses. Key challenges include regulatory approvals, manufacturing scalability, and reimbursement dynamics across jurisdictions.

Company Overview

Enlivex Ltd. operates as a clinical-stage biotechnology company focusing on advancing quality longevity therapies through macrophage reprogramming immunotherapy [S1]. Its lead investigational product is Allocetra™, which is based on licensed apoptotic cell technology originally developed by Israeli medical research institutions such as Hadassah Hospital's technology transfer offices [S25]. Esteemed for treating autoimmune and inflammatory disorders—including osteoarthritis—Allocetra™ leverages this cellular approach to modulate immune response pathways.

The company's strategic moat primarily derives from its wide patent portfolio—covering key inventions, compositions, and processes—with issuances extending globally [S25]. As of March 2026, Enlivex holds multiple issued patents with expiration dates spanning from 2025 through 2038 alongside several pending US patent applications [S25]. Manufacturing occurs at a dedicated cGMP-certified facility located in Ness Ziona, Israel. This specialized setup produces frozen formulations designed specifically for stability during clinical trials [S1].

Importantly, Enlivex outsources the operational aspects of its clinical trials to contract research organizations (CROs), reflecting a virtualized model that lacks an internal commercial infrastructure including sales and marketing capabilities. The company signals intent to pursue co-development or licensing partnerships for eventual product commercialization [S1].

Historical Financial Performance

Examining Enlivex’s financial trajectory over the recent four-year span reveals persistent operating losses offset by a dramatic inflection in net income during FY2025 (figures cited from company filings) [F1]:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 1236 | -10 | -15 | 0 | +8329.2% |

| 2024 | -15 | -13 | -16 | 0 | +48.3% |

| 2023 | -29 | -24 | -29 | 0 | +6.4% |

| 2022 | -31 | -24 | -26 | 8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -10 | 63.9 |

| 2024 | -13 | -63.6 |

| 2023 | -24 | -96.6 |

| 2022 | -32 | -54.6 |

Source: SEC companyfacts cache [F1].

Operating losses have narrowed substantially from nearly $30 million in FY2023 and FY2022 to just over $15 million in FY2025—a sign of more controlled expenditure or possibly lower ongoing activities [F1]. Nevertheless, the net income figure swings from losses near $30 million up until FY2024 into an anomalous gain exceeding $1.23 billion in FY2025 [F1]. This divergent surge is not supported by an equivalent improvement in core operations or cash flows; operating cash flow remains negative (-$10.4 million), indicating that the bottom line benefit largely stems from extraordinary or non-operating items such as financial instruments or derivative gains rather than underlying profitability [F1,S1].

Capital expenditures have reduced drastically over this period to just $68 thousand in FY2025 from much higher levels previously; this supports the notion that capital investments are minimal currently as focus aligns on development activities rather than expanding manufacturing capacity [F1]. The company’s equity base expanded dramatically by year-end 2025 reflecting new financings raising liquidity for ongoing operations [F1,S27]. The current ratio stands extremely high at approximately 193x given current assets of $1.74 billion dwarfing current liabilities just over $9 million—indicating strong short-term liquidity buffer available despite operating cash burn [F1].

Growth Prospects

Enlivex’s future growth prospects hinge critically on successful transition from clinical-stage status through regulatory milestones towards product commercialization:

Clinical Development Progress: Allocetra™, being their lead candidate for inflammatory diseases, must successfully complete pivotal trials to achieve regulatory approval across key markets including the US FDA and European EMA [S1,S14,S16]. The company’s pipeline expansion potentially involves indications beyond osteoarthritis leveraging macrophage reprogramming platforms.

Regulatory Approvals: Gaining approvals entails navigating complex requirements such as compliance with Good Clinical Practices (GCP), managing risks indicated by prior FDA scrutiny of manufacturing sites and trial data integrity, securing orphan drug designations where applicable for market exclusivity benefits, and meeting post-approval pharmacovigilance obligations like REMS programs [S6,S7,S12,S14]. Delays or adverse regulatory actions represent material headwinds.

Manufacturing Scale-Up: Transitioning from clinical batch manufacture at Ness Ziona into scalable commercial production will require broadening GMP-certified capacities or establishing partnerships with CMOs familiar with cell therapy frozen formulation standards—an operational bottleneck common across biotech innovators specializing in cell-based therapies.

Partnerships & Commercialization: Lacking internal sales infrastructure necessitates alliance strategies with experienced biopharma firms capable of marketing immunotherapies globally—particularly critical amidst payer scrutiny emphasizing cost-effectiveness data submission before achieving formulary acceptance [S1,S22,S26].

Risks related to intellectual property enforceability amid intense competition from other immunotherapeutic approaches also pose challenges to maintain competitive differentiation long term [S19,S29].

Forecasts / Milestones / Expectations

The company has not provided explicit guidance or time-bound milestones for efficacy readouts or regulatory filings within these SEC filings or press releases up until March 2026 [S2,S3]. Investors should monitor indications such as:

- Initiation or completion timelines of phase II/III studies.

- FDA/EMA feedback on Investigational New Drug (IND) applications or Biologics License Applications (BLA).

- Regulatory orphan designation grants that can bolster market exclusivity.

- Licensing deals or co-development partnership announcements enhancing commercial positioning.

Enlivex’s upcoming financial disclosures following its March private placement ($19 million senior secured convertible promissory note) will further clarify runway adequacy supporting near-term development objectives [S3].

Returns / Capital Allocation

Return metrics measured by accounting standards indicate that despite the extraordinary net income reported in FY2025 resulting in an approximately 63.9% return on equity (ROE), this figure reflects non-operating financial events rather than sustainable profit generation from operations [F1]. Operating losses persist yearly:

- Steady but negative operating income ranging between -$29M (FY23) improving modestly to -$15M (FY25).

- Consistently negative cash flow from operations averaging roughly -$10 million annually recently.

Capital allocation has primarily focused on sustaining clinical study expenditures rather than infrastructure expansion; capital expenditures diminished drastically suggesting restrained investment apart from core trial support activities [F1]. There were no reported dividend distributions or share buybacks documented within these periods [F1], consistent with typical development-stage biotech practices prioritizing cash preservation.

Recent financing completed via private placement notes emphasizes reliance on debt-equivalent instruments convertible into equity rather than costly public offerings or dilution-heavy equity issuance presently [S3,S27], enabling flexible cash management matched against milestone-dependent R&D spending.

Industry Context Analysis

Biotechnology companies pursuing cellular immunotherapies face a complicated interplay between novel science validation cycles and stringent regulatory frameworks aimed at ensuring patient safety particularly given the innovative nature of apoptotic cell-derived treatments such as Allocetra™. Manufacturing frozen cell formulations under cGMP conditions is particularly challenging due to stability requirements that impact supply chain logistics compared with traditional pharmaceuticals—a factor influencing cost bases profoundly during early commercialization stages.

Patent protection breadth serves an outsized role since competitors might attempt biosimilar developments rapidly once exclusivity lapses unless secondary patents fortify barriers; thus proactive IP defense alongside accelerated regulatory pathways such as orphan drug designation often underpin commercial viability assumptions prevalent industry-wide.

Meanwhile payment systems globally exert growing pressure via health technology assessments requiring robust demonstration of comparative effectiveness versus established therapeutics—an emerging hurdle many pioneering immunotherapy developers grapple with when seeking formulary inclusion globally.

Conclusion

Enlivex Ltd.’s profile typifies a cutting-edge biotech entity balancing promising macrophage-reprogramming immunotherapy innovation against significant operational hurdles—notably continuing operating losses amidst volatile net income caused by one-time financial factors unrelated directly to core business profitability. With leading apoptotic cell technology protected by expansive patent rights and an outsourced yet focused development model culminating with Allocetra™, Enlivex steers towards critical regulatory milestones whilst relying heavily on external capital infusions such as recent secured convertible debt deals.

Success will depend substantially on successful clinical trial outcomes supporting regulatory submissions across major markets combined with strategic commercial partnerships adept at negotiating complex pricing/reimbursement landscapes inherent in emerging biologic therapies targeting inflammatory diseases.

Suitable monitoring of upcoming trial results visibility, regulatory step progression, partnership formations, and sustainability indicators like cash flow improvements will provide clearer insights into Enlivex’s maturation trajectory through the biotechnology lifecycle stages ahead.

This report is prepared solely for informational purposes without offering investment advice or recommendations concerning securities transactions involving Enlivex Ltd.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments