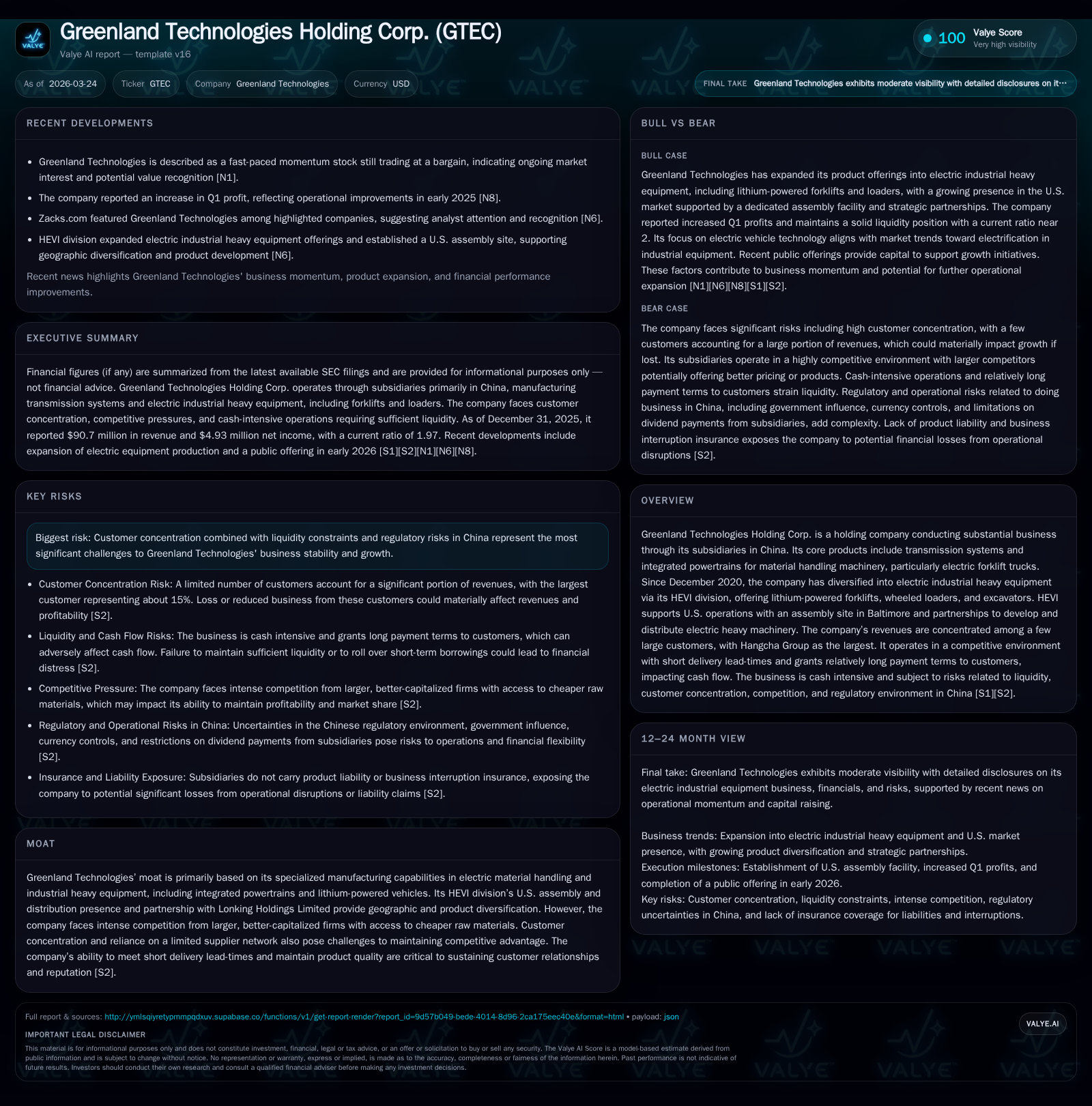

Greenland Technologies’ Balancing Act: Customer Concentration Risks and Expansion into Electric Heavy Equipment

Customer concentration and competitive pressures challenge Greenland Technologies as it diversifies into electric heavy industrial equipment through its HEVI division.

Greenland Technologies Holding Corp. reported revenues of approximately $90.7 million in 2025, up 8% year-over-year after a dip in 2024 [F1]. Operating income declined over 40% in 2025 to $7.5 million, reflecting margin compression amid raw material inflation and competitive pricing pressures [F1][S2]. The company’s customer base remains concentrated, with the Hangcha Group accounting for around 15–18% of quarterly revenues and the top five customers contributing about 40%, creating negotiation leverage risks and sales volatility [S4][S5][S6][S7][S8][S10]. Greenland is expanding into electric industrial heavy equipment via its HEVI division, which operates a U.S. assembly site and has partnerships targeting North American markets, though market acceptance and profitability risks remain [S22][S28]. Operationally, improved cash flow generation coupled with sharply reduced capital expenditures enabled positive free cash flow near $15 million in 2025 despite working capital challenges from long payment terms and supplier concentration [F1][S26][S27]. Going forward, key considerations include customer diversification efforts, HEVI’s market penetration, raw material cost management, and navigating regulatory uncertainties related to China operations.

Growth Trajectory and Revenue Drivers: Peaks and Valleys

Greenland Technologies has experienced fluctuating financial performance through FY2025. Revenue was steady near $90 million levels from FY2022 ($90.8M) before declining to $83.9M in FY2024, then rebounding by about 8% to $90.7M in FY2025 [F1]. Despite top-line recovery, operating income showed volatility—rising from $5.96 million in FY2022 to nearly $12.6 million by FY2024 before falling more than 40% to $7.52 million last year—indicating margin compression likely due to cost inflation or competitive pressures [F1]. Net income swung dramatically from a small profit of $0.75 million in FY2022 to a loss of $15.9 million in FY2023 before recovering to double-digit millions profit ($14.1M) in FY2024 and retreating again to around $4.9 million in FY2025 [F1].

Operating cash flow improved steadily with a roughly 17% increase reaching nearly $15.6 million last fiscal year while capital expenditures were curtailed significantly—from above $1.9 million down near half a million—reflecting operational discipline that produced positive free cash flow exceeding $15 million most recently [F1]. This suggests underlying business efficiency despite profitability headwinds.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 91 | 5 | 16 | 8 | +8.0% | -64.9% |

| 2024 | 84 | 14 | 13 | 13 | -7.1% | +188.6% |

| 2023 | 90 | -16 | 2 | 11 | -0.5% | -2229.8% |

| 2022 | 91 | 1 | 7 | 6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 2 | 15 | 6.8 |

| 2024 | 6 | 11 | 23.4 |

| 2023 | 1 | -31.7 | |

| 2022 | 1.1 |

Source: SEC companyfacts cache [F1].

Note: Revenue shows cyclicality with a dip in FY24; operating income peaked then contracted; net income includes loss turnaround; capital spending was curtailed substantially.

Customer Dependence: Risks of Concentration

Greenland’s revenues are heavily dependent on a limited number of customers. The largest client—Hangcha Group—accounts for approximately 15-18% of quarterly revenues consistently across reporting periods [S4–S10], while the top five customers collectively contribute around 40%. This concentration exposes Greenland to significant negotiation leverage risks and revenue volatility if any major customer reduces orders or alters contract terms.

Moreover, subsidiaries are not exclusive providers for these clients and face intense competition that limits pricing power during contract negotiations—a risk factor repeatedly emphasized as potentially leading to unfavorable terms impacting margins or revenue levels [S4][S5][S6][S7][S8][S10]. Fluctuations due to project completions or spending reductions from key customers can thus materially affect growth.

Competitive Environment and Supply Chain Vulnerabilities

Greenland operates amid intense competition from larger global peers who benefit from greater financial resources and access to cheaper raw materials—a critical factor given steel comprises a substantial portion of input costs [S2][S7][S8][S10]. Volatility in steel prices directly affects operational results since passing through price increases is often constrained by competitive pricing pressures.

The company faces short lead times for product deliveries demanded by large manufacturing clients that require prompt fulfillment [S13], increasing procurement challenges. Supplier concentration further elevates risk; the need for diversifying the supplier network is highlighted given potential disruptions if key suppliers are lost or unable to meet demand at competitive prices [S4][S6][S23]. These factors limit earnings stability despite ongoing supply chain investments.

Diversification via HEVI Division: Strategic Opportunities and Challenges

Greenland has sought diversification through its HEVI subsidiary focused on electric industrial heavy equipment such as lithium-powered forklifts and wheel loaders targeting North American markets—a strategic pivot beyond traditional transmission systems primarily sold within China [S22].

HEVI operates a sizable assembly facility (54,000 square feet) in Baltimore since August 2022 enhancing local assembly and distribution capabilities for U.S.-based clients [S22]. Additionally, HEVI formed a partnership with Lonking Holdings Limited announced mid-2024 focused on developing products tailored for the U.S., signaling intent for robust market penetration beyond incumbent forklift segments [S22][S28].

However, this new business line entails execution risks including uncertain market acceptance of electric heavy machinery products alongside relatively high fixed costs associated with new technology deployment—factors that may delay profitability gains or revenue contributions as disclosed by the company [S22][S28].

Liquidity Position and Capital Allocation

At fiscal year-end 2025 Greenland held current assets of approximately $95 million against current liabilities near $48 million yielding a current ratio around 1.97 indicative of reasonable short-term liquidity coverage though extended receivable collection periods partially constrain cash turnover efficiency [F1][S26][S27].

Operating cash flow improved significantly by about 17% reaching nearly $15.6 million while capital expenditures were reduced by over seventy percent compared to prior year spendings—resulting in positive free cash flow near $15 million after investment outlays—which provides flexibility for reinvestment or shareholder returns despite margin pressures [F1].

Dividend payments totaled roughly $2.2 million in FY25 following higher dividends paid previously reflecting moderated payout aligned with subdued net income levels relative to peaks; return on equity stands modestly at approximately 6.8%, indicating moderate profitability relative to equity base size after recent fluctuations [F1].

Operational Efficiency Amid Margin Pressures

The sharp contraction in operating income despite rising revenues illustrates mounting margin pressure during FY25 likely driven by steel price spikes noted as a key cost factor limiting profitability improvements even as volume grew [(supported by S2)][F1]. Extended customer payment terms further strain working capital requiring internal financing that reduces operational leverage.

Intense competition necessitates pricing discipline that constrains Greenland’s ability to fully offset input cost inflation while tight delivery timelines increase procurement inefficiencies eroding margins further; these factors collectively dampen earnings quality despite volume gains [F1] [S7] [S8].

Outlook: Key Milestones and Risks Ahead

While no explicit forward guidance is provided in recent filings monitoring should focus on several strategic areas:

- Diversifying the customer base beyond dominant players like Hangcha to reduce negotiation risk concentration.

- Progress on HEVI division’s electric heavy equipment product launches including U.S. facility integration and partnership outcomes.

- Management’s effectiveness at passing through raw material cost increases without damaging order volumes amid volatile steel markets.

- Navigating evolving China regulatory frameworks affecting offshore listings and industry operations.

- Recovery trajectory for operating margins indicating success managing cost pressures alongside competitive intensity.

These factors will shape Greenland Technologies’ ability to balance legacy forklift drivetrain sales risks tied to concentrated customers against growth opportunities emerging from nascent electric heavy equipment ventures abroad.

This analysis is based solely on publicly available data extracted from SEC filings dated through March 24, 2026 ([F1],[S#]) without speculative forecasts or invented data. It does not constitute investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments