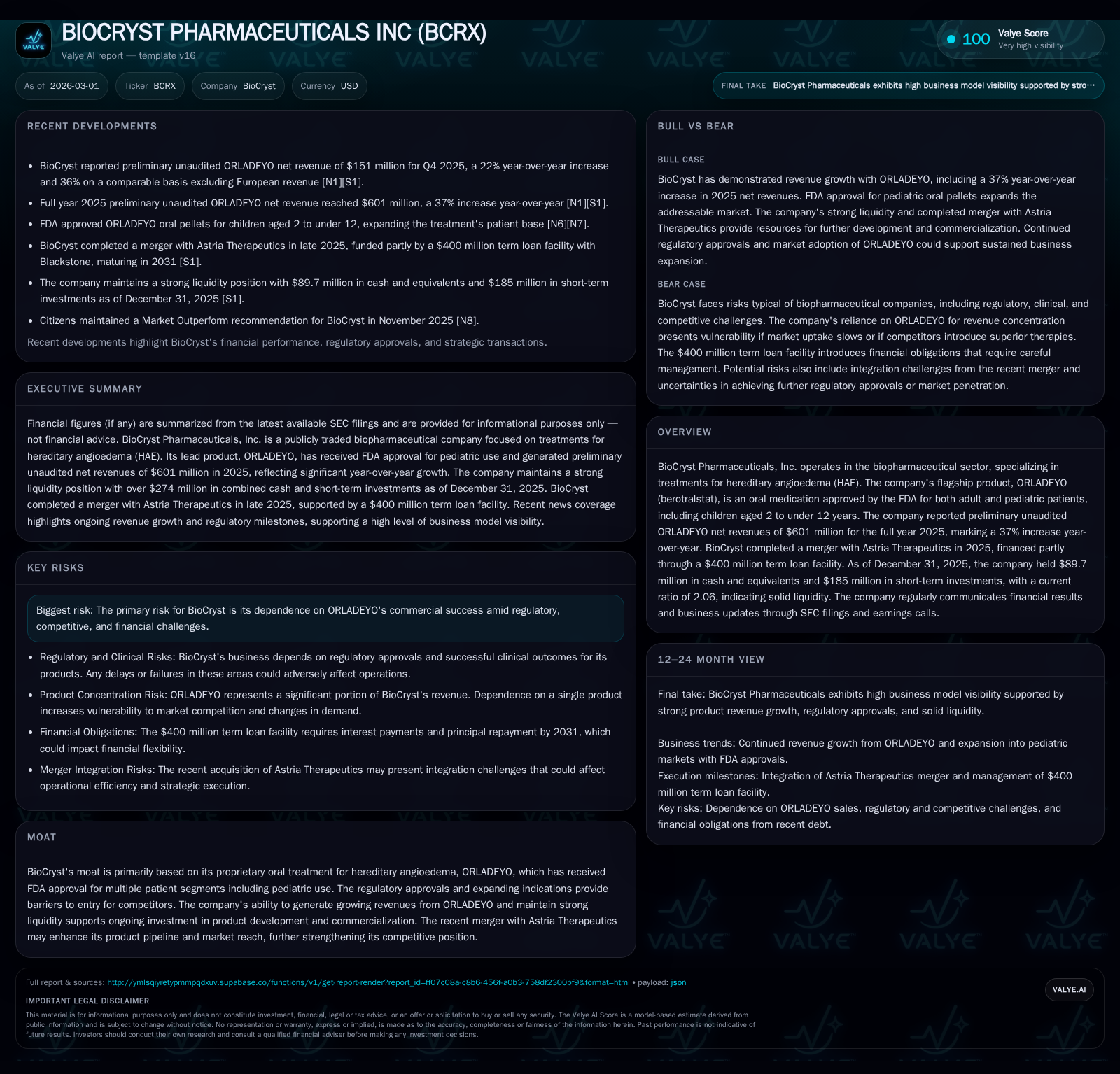

BioCryst's Transition to Profitability Backed by ORLADEYO Growth and Astria Integration

BioCryst Pharmaceuticals reversed years of losses in 2025 propelled by strong ORLADEYO sales growth and a strategic merger with Astria Therapeutics.

BioCryst Pharmaceuticals reported a remarkable turnaround in fiscal year 2025, posting $341 million in operating income after years of substantial losses. This shift was driven primarily by a 37% year-over-year surge in revenues from its oral hereditary angioedema (HAE) treatment, ORLADEYO, alongside strategic expansion via the merger with Astria Therapeutics. The merger, financed through a $400 million term loan, supports pipeline diversification but introduces leverage considerations. Strong liquidity metrics and substantial operating cash flow underpin BioCryst's improved financial footing, although risks remain tied to ORLADEYO’s market performance and regulatory environment.

Trajectory of Growth: From Operating Losses to Robust Income

BioCryst Pharmaceuticals experienced a significant financial turnaround in FY2025, shifting from sustained operating losses to an operating income of $340.99 million as reported in the latest annual filing [F1]. This represents a dramatic improvement compared to operating losses of $2.54 million in FY2024 and deeper deficits in prior years. Net income similarly turned positive at $263.86 million for FY2025 versus negative $88.9 million the previous year [F1]. Operating cash flow also rebounded strongly to $347.37 million from negative cash flows in preceding years [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 264 | 347 | 341 | +396.9% |

| 2024 | -89 | -52 | -3 | +60.8% |

| 2023 | -227 | -95 | -104 | +8.3% |

| 2022 | -247 | -162 | -148 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -221.4 |

| 2024 | 18.7 |

| 2023 | 49.7 |

| 2022 | 83.9 |

Source: SEC companyfacts cache [F1].

*ORLADEYO net revenue for full year 2025 as preliminarily reported by the company constitutes the majority of total revenue [N1][F1].

ORLADEYO’s Commercial Momentum Driving Revenue Expansion

The cornerstone of BioCryst's recovery is its oral hereditary angioedema therapy ORLADEYO (berotralstat). Preliminary unaudited figures indicate net revenues near $601 million for FY2025—a 37% increase year-over-year [N1][F1]. Excluding European revenues due to restructuring agreements enhances comparable growth to approximately 43% on a like-for-like basis [S9].

FDA approvals expanding ORLADEYO’s indication to pediatric patients aged 2 through under 12 years significantly enlarge its addressable market segment and strengthen its competitive positioning [N1][S1]. This regulatory progress provides barriers against immediate generic or alternative oral C1 inhibitor therapies.

A recent wholesale acquisition cost increase implemented early in 2026 aims to support ongoing commercial viability amid competitive pressures [S26]. Continued uptake rates will be critical to sustaining this momentum.

Astria Therapeutics Merger: Strategic Rationale and Impact

In January 2026 BioCryst finalized its acquisition of Astria Therapeutics through a stock-and-cash merger designed to diversify its therapeutic pipeline beyond ORLADEYO [S6][S24]. Astria merged into BioCryst as a wholly owned subsidiary with former Astria shareholders receiving shares plus cash consideration per merger terms detailed in regulatory filings.

This transaction broadens BioCryst’s product portfolio while mitigating concentration risk from reliance on a single blockbuster product. The deal was predominantly financed via a $400 million term loan facility with quarterly interest-only payments extending over five years at an interest rate based on SOFR plus approximately 4.5% margin [S6][S7][S8].

The merger lays groundwork for potential synergistic benefits including cross-selling opportunities and enhanced innovation pathways.

Financial Health Post-Merger: Liquidity and Capital Structure Analysis

As of December 31, 2025—prior to closing the merger—BioCryst reported cash and equivalents totaling roughly $89.7 million alongside short-term investments approximating $185 million. Current assets stood at about $404 million against current liabilities near $196 million yielding a solid current ratio of approximately 2.06 [F1].

The loan agreement imposes customary covenants restricting asset disposals outside ordinary course activities and limits dividend payments or other restricted equity distributions absent lender consent [S6][S8]. A pay-in-kind interest option is available for up to two years post-closing providing some near-term cash flow flexibility at the cost of incremental interest expense.

Prepayment penalties decline over time but could disincentivize early debt repayment absent excess free cash flow availability.

Risks Shaping BioCryst’s Competitive and Regulatory Environment

Key risks include dependency on ORLADEYO’s sustained commercial success amid an evolving competitive landscape featuring emerging oral HAE therapies [S4][S5]. Regulatory exclusivity offers temporary protection; however patent expirations or biosimilar entry could impact midterm revenue stability.

Intellectual property litigation risks exist but no material adverse rulings are currently disclosed.

Concentration risk is heightened given reliance on reimbursement frameworks for high-cost specialty therapies targeting rare diseases with limited patient populations subject to shifting clinical guidelines and payer policies.

Compliance with debt covenants post-Astria transaction warrants monitoring though headroom currently exists.[S6]

Future Growth Catalysts and Market Opportunities for ORLADEYO

Expansion into pediatric indications enhances overall addressable market size supporting long-term revenue growth potential toward or beyond analyst-discussed billion-dollar sales targets for chronic HAE prophylaxis treatments [N4][N5].

Additional catalysts include successful commercial scale-up outside the U.S., integration benefits from Astria’s assets enabling product lifecycle extensions or complementary assets within the franchise [N3].

Label expansion efforts into related rare bradykinin-mediated angioedema conditions remain under evaluation but face high regulatory scrutiny.

Global payer cost controls and intensifying competition may constrain uptake velocity despite first-mover advantages.

Capital Allocation Priorities: Evaluating Cash Flow and Shareholder Returns

Capital allocation currently prioritizes reinvestment toward growth initiatives over dividends or buybacks consistent with industry norms for late-stage biotech firms ramping commercial operations.

Operating cash flow generation reached approximately $347 million in FY2025 enhancing financial flexibility for R&D investment and debt servicing.[F1]

No recent dividends or share repurchase programs have been announced.

Negative shareholders' equity of about -$119 million reflects accumulated deficits despite transitioning profitability,[F1] suggesting return-of-capital measures remain distant.

Estimated free cash flow approximates operating cash flow given typical low capital expenditure intensity.

Analyst Expectations and What to Monitor Going Forward

Recent earnings results exceeded consensus estimates fueling optimism around sustainable profitability anchored by growing ORLADEYO revenues coupled with strategic M&A diversification.[N1][N3]

Upcoming milestones include FDA reviews related to label expansions especially pediatric safety/efficacy data updates alongside European commercialization strategies following divestiture activities.[N1]

Integration progress with Astria remains critical as synergy realization may materially influence medium-term financial outcomes.[N3]

Market uptake dynamics under evolving competition will provide directional insights into pricing power retention and payer acceptance.

Investors should monitor quarterly disclosures detailing regional/patient segment revenues alongside operational expense trends assessing margin sustainability post-turnaround.

This analysis is based on data available as of February 2026 sourced from SEC filings and company disclosures. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments