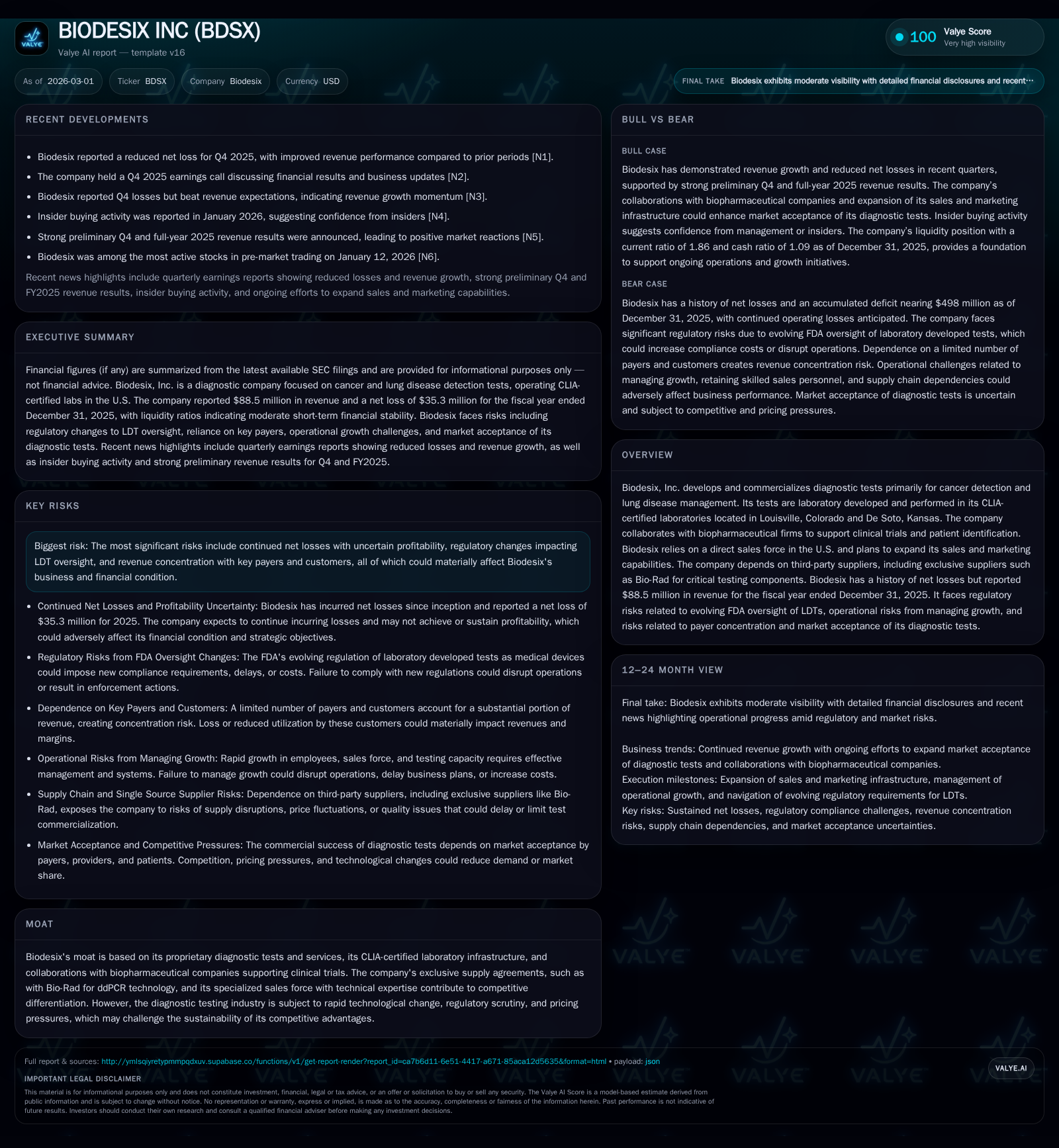

Biodesix's Financial Trajectory: High Growth Meets Ongoing Profitability Hurdles and Evolving FDA Oversight

Biodesix’s substantial revenue expansion contrasts with persistent net losses amid regulatory shifts and operational dependencies shaping its strategic outlook.

Biodesix has demonstrated robust revenue growth over recent years, driven primarily by its proprietary diagnostic tests for cancer and lung diseases. Despite top-line momentum, the company continues to report significant operating and net losses, although these have narrowed year-over-year. Regulatory changes targeting laboratory-developed tests (LDTs) and concentration risks with major payers and suppliers remain key challenges. Biodesix’s capital structure includes debt covenants that restrict financial flexibility, underscoring the importance of cash flow management as it expands its U.S. sales force and pursues biopharmaceutical collaborations.

Robust Revenue Growth: The Upside of Proprietary Diagnostics

Biodesix has achieved a striking revenue ramp over the four-year span ending December 31, 2025. Revenues nearly doubled on average every two years, climbing from $38.2 million in FY2022 to $88.5 million in FY2025 according to filings [F1]. This ~24% year-on-year growth in the latest fiscal year underscores strong market acceptance of their proprietary cancer diagnostics portfolio including lung cancer-focused assays performed in CLIA-certified facilities in Colorado and Kansas [N1][S1]. The company leverages laboratory-developed tests (LDTs) characterized by exclusive supply relationships — most notably Bio-Rad’s ddPCR technology — which support test specificity but also add operational complexity.

Growth drivers largely stem from penetrative commercialization efforts across clinical segments and biopharmaceutical collaborations that advance companion diagnostics within targeted patient populations [N1][N2]. Despite nascent profitability metrics, expanding revenues signal emerging leverage potential if scaling can moderate fixed costs.

Profitability Trends: Operating Losses Narrow but Persist

While topline gains are notable, Biodesix remains entrenched in operating deficits that have improved modestly but still weigh on financial health. Operating income improved approximately 19% year-over-year from -$50.6 million in FY2022 to -$27.9 million in FY2025 [F1]. Net losses followed a similar trajectory with the FY25 shortfall at $35.3 million compared to $65.4 million three years earlier.

Persistent net losses reflect amplified research & development outlays to drive test innovation and maintain compliance amidst increasing regulatory complexity plus elevated marketing expenses supporting U.S. sales force expansion [N1][S1][S4]. Further pressure arises from administrative costs linked to public listing requirements and underlying scale limitations inherent to the LDT laboratory model.

Moreover, operating cash flow remains deeply negative at -$23.3 million in FY2025 with free cash flow similarly challenged after minimal capital expenditure investment during the year (approximately -$23.5 million) [F1]. This cash burn dynamic emphasizes a continuing need for external financing or sustained revenue growth acceleration for earnings inflection.

Historical Financial Performance

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 88 | -35 | -23 | -28 | +24.1% | +17.9% |

| 2024 | 71 | -43 | -49 | -34 | +45.3% | +17.7% |

| 2023 | 49 | -52 | -23 | -41 | +28.5% | +20.3% |

| 2022 | 38 | -65 | -45 | -51 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -24 | 1430.6 |

| 2024 | -52 | -205.6 |

| 2023 | -46 | -1138.6 |

| 2022 | -48 | -317.6 |

Source: SEC companyfacts cache [F1].

Evolving Regulatory Landscape for Biodesix’s LDTs

The company faces an unstable regulatory environment intensified by potential FDA oversight expansion over laboratory-developed tests (LDTs). Although a March 31, 2025 court ruling vacated prior FDA final rules subjecting LDTs to medical device premarket controls, ambiguity remains as the FDA asserts authority over certain components like reagents or instrumentation sourced externally — components integral to Biodesix’s assays [S1][S5][S6][S17].

Such regulatory flux introduces risks including delayed product launches due to protracted review timelines or increased compliance costs that could impact product margins adversely. Additionally, evolving Medicare/Medicaid reimbursement policies heighten uncertainty around payer coverage decisions essential for diagnostic adoption and revenue sustainability.

Regulatory shifts require continuous engagement by Biodesix’s compliance teams alongside strategic adaptation of test offerings that meet new standards without incurring prohibitive overhead or curtailing innovation pace.

Customer and Supplier Dependencies: Concentration and Supply Chain Sensitivities

Revenue concentration raises operational vulnerabilities for Biodesix given reliance on a few large payers constituting over one-third of total revenues—some accounting individually for up to 32–39% share—according to segment disclosures [S11][N1]. The loss or non-renewal of contracts with these significant customers could materially impair revenue visibility.

On the supply side, exclusivity agreements—particularly with Bio-Rad supplying ddPCR testing reagents—introduce another layer of dependency that constrains production flexibility and may expose Biodesix to supplier pricing pressures or logistics disruptions impacting test availability [S29]. These dynamics enforce a delicate balance between leveraging specialized inputs that provide competitive differentiation while managing countermoves through alternate sourcing or inventory buffers.

Future Growth Catalysts and Market Risks: Sales Expansion and Competitive Pressures

Looking forward, Biodesix plans accelerated commercialization backed by an expanded direct sales team targeting greater penetration in U.S.-based cancer diagnostics markets where reimbursement dynamics are complex yet lucrative if navigated effectively [N1][N3]. Moreover, collaboration strength with biopharmaceutical partners supporting clinical trial enrollment remains pivotal—as companion diagnostics increasingly influence precision oncology treatment pathways.

The William Blair upgrade signals external confidence premised on Biodesix’s differentiated pipeline and market positioning despite acknowledged risks [N3]. Insider buying activity further suggests management conviction toward near-term value creation bets amidst competitive headwinds driven by rapid technological evolution among diagnostics peers requiring continual innovation investment [N5][S1].

Capital Allocation Overview: Cash Flows, Debt Covenants, and Returns

Financial stewardship faces scrutiny as ongoing losses depress equity position which was slightly negative (-$2.47 million) by December 2025 contrasting prior positive equity balances [F1]. The Perceptive Term Loan Facility structuring caps capital agility via stringent covenants mandating minimum cash reserves and trailing revenue thresholds restricting discretionary expenditures beyond core operations [S4].

Capital expenditures plummeted nearly 92% from $22.9 million in FY2023 down to just $0.26 million last fiscal year—a decisive pivot toward conserving liquidity within tight funding constraints while focusing on sustaining operating capacity rather than equipment expansion [F1]. Operating cash flows remain significantly negative indicating a continued financing requirement until sustainable profitability emerges.

Returns measures like ROE lack meaningful positive readings due to cumulative deficits reflecting early-stage scale investments without earnings leverage so far manifesting fully.

Key Milestones to Watch: Clinical Trials, FDA Approvals, and Sales Force Expansion

Absent explicit forward guidance from public disclosures or earnings commentary, critical future progress points emerge analytically around successful acquisition of regulatory clearances expanding diagnostic indications beyond current panels plus subsequent reimbursement endorsements from Medicare/Medicaid payers enhancing volume uptake [N2][S1].

Commercial benchmarking includes monitoring sales force productivity enhancements as personnel additions yield broader geographic reach alongside pipeline updates concerning companion diagnostic developments supporting partner drug trials securing market validations.

Observers should also track legislative developments affecting LDT governance as future FDA rulemaking or congressional initiatives might abruptly shift compliance cost structures or market access parameters.

This analysis synthesizes publicly available financial data alongside regulatory filings and earnings commentaries without prescribing investment actions. All figures are directly referenced from official SEC filings or verified disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments