Confluent’s Data Streaming Growth Slows with Costs and Consumption Challenges Ahead

The data streaming pioneer sustains growth amid margin pressures and macroeconomic headwinds while preparing for an IBM acquisition.

Confluent, Inc. has demonstrated solid revenue growth driven by its Confluent Cloud and Bring Your Own Cloud (BYOC) offerings, benefiting from the foundational technology of Apache Kafka. Despite improving operating losses and positive operating cash flow growth in 2025, profitability remains elusive amid ongoing investments and competitive pressures. The company's shift to a consumption-based sales model affects near-term revenue visibility, compounded by cautious enterprise IT spending. The pending merger with IBM introduces execution risks but also hints at a strategic pivot toward scale. Monitoring future adoption rates, consumption patterns, and integration milestones will be critical for assessing Confluent's trajectory post-acquisition.

Company Overview and Historical Performance

Confluent, Inc., founded in 2014 by key figures behind Apache Kafka such as Jay Kreps and Neha Narkhede, has emerged as a significant player in the data streaming platform sector. Its primary offerings include Confluent Cloud and Bring Your Own Cloud (BYOC) solutions which allow real-time data streaming and analytics in cloud environments [S1]. The company services enterprise and public sector customers globally.

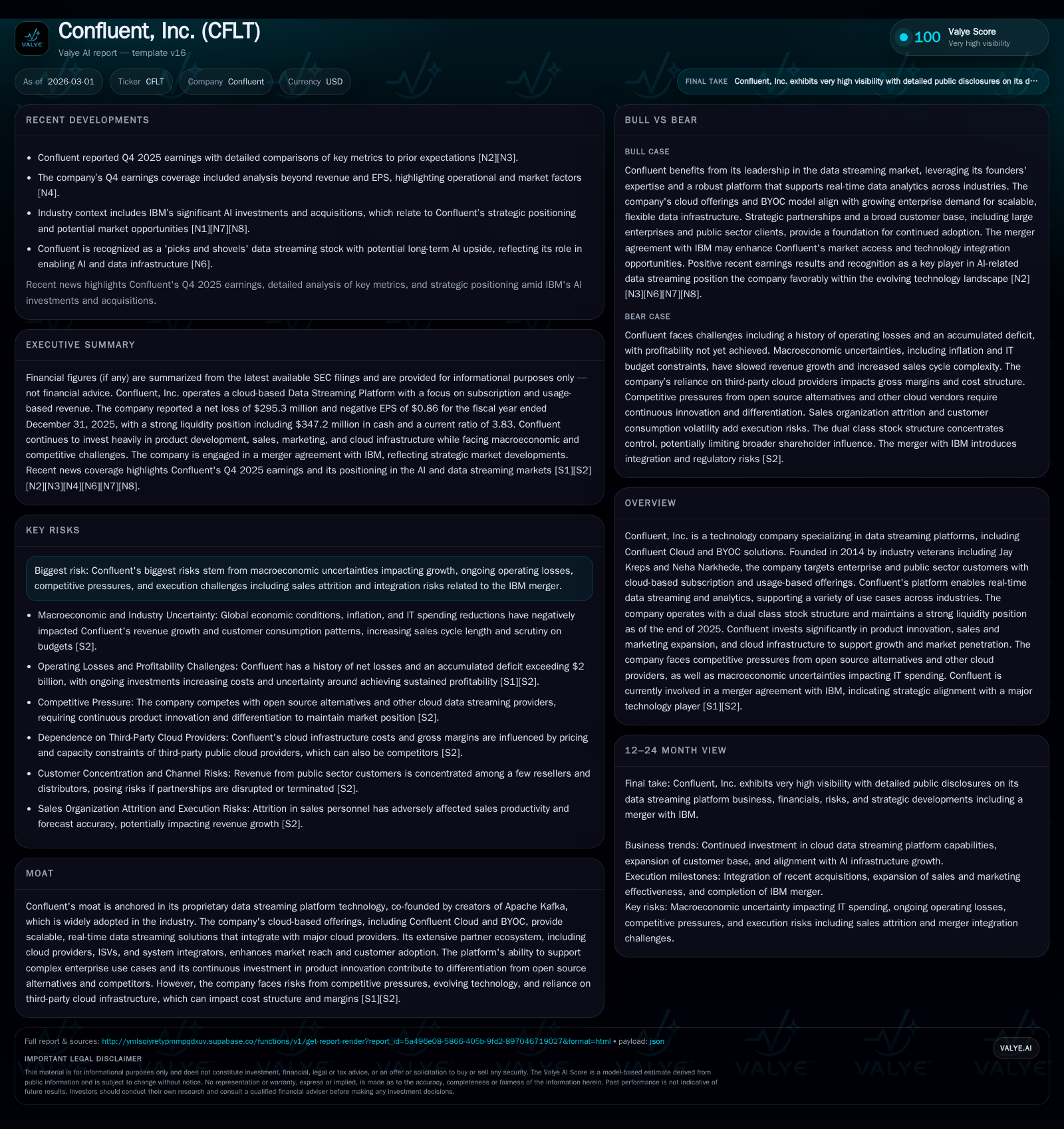

Financially, Confluent has exhibited consistent revenue growth over recent years, supported by expanding adoption of its platform. Operating losses have narrowed moderately—from approximately -$478.8 million in 2023 to -$380.1 million in 2025—reflecting an incremental improvement of about 9.3% year-over-year [F1]. Net losses followed a similar trajectory: from roughly -$442.7 million in 2023 down to -$295.3 million in 2025.

A critical turning point came in operating cash flow (CFO), which swung from negative $103.7 million in 2023 into positive territory by $64.3 million in 2025—a nearly 92% year-over-year increase—signaling better cash generation despite ongoing investments [F1]. Capital expenditures have remained relatively small but rose about 40% to $3.6 million in 2025, reflecting increased spending on infrastructure supporting cloud products [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -295 | 64 | -380 | 4 | +14.4% |

| 2024 | -345 | 33 | -419 | 3 | +22.1% |

| 2023 | -443 | -104 | -479 | 3 | +2.2% |

| 2022 | -453 | -157 | -463 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 61 | -25.3 |

| 2024 | 31 | -35.9 |

| 2023 | -106 | -54.6 |

| 2022 | -161 | -58.8 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures are not available within provided data; focus is on profitability and cash flow metrics.

Business Model Nuances and Market Position

Confluent's business relies on subscription-based cloud revenue complemented by variable usage fees tied to Confluent Cloud consumption [S16][S21]. The transition towards a consumption-oriented sales model since 2024 has introduced short-term revenue visibility challenges due to lower initial usage from new customers and elongated adoption curves [S14][S16]. This shift aligns with broader SaaS trends where monetization increasingly depends on real-time usage rather than upfront commitments.

The company’s moat centers on its proprietary enhancements atop Apache Kafka technology—the latter being an industry open source standard for event streaming [S25]. Notwithstanding this entrenched position, Confluent faces growing competitive risks from both open source implementations managed internally by enterprises and fully managed services offered directly by public cloud providers like AWS (MSK), Microsoft Azure Event Hubs, and Google Cloud Pub/Sub [S25]. These competitors enjoy potential platform-level advantages.

To counter these threats, Confluent invests heavily in differentiating features, seamless multi-cloud capabilities through BYOC, partner ecosystems encompassing ISVs and system integrators, as well as developer community engagement [S1][S25]. However, reliance on third-party cloud infrastructure introduces cost uncertainties impacting margins.

Growth Drivers and Constraints

Future growth hinges on several vectors:

- Increased Customer Consumption: Upselling existing customers by expanding use cases for real-time streaming remains paramount. This includes enabling complex enterprise workflows beyond initial onboarding [S16][S21].

- New Customer Acquisition: Expanding the installed base in targeted segments including large enterprises and SMBs through tailored marketing and accelerated sales ramping [S7][S21].

- Product Innovation: Continuous enhancement of platform features to sustain differentiation against competitive offerings is critical [S1][S25].

- Partner Ecosystem Expansion: Leveraging alliances with major cloud providers and global systems integrators to extend market reach.

Conversely, growth is tempered by:

- Macroeconomic Uncertainty: Persistent IT budget caution across industries has led to longer sales cycles and lowered consumption expansions among existing clients [S2][S27].

- Execution Risks Related to IBM Merger: The December 2025 merger agreement with IBM introduces integration complexities which could divert management focus or disrupt operations temporarily [S6][S8].

- Competitive Pressures: Open source alternatives combined with incumbent cloud providers’ offerings create pricing pressures and require ongoing differentiation efforts [S2][S25].

- Pricing Strategy Challenges: Limited historical experience setting optimal pricing under inflationary/recessionary pressures adds uncertainty to future margins [S17][S21].

Capital Allocation and Returns

As of December 31, 2025, Confluent holds a strong liquidity position with cash & equivalents totaling approximately $347 million against current liabilities of $681 million yielding a current ratio near 3.83x [F1][S23]. Equity stands at nearly $1.17 billion.

Return metrics indicate negative approximate ROE of about -25%, consistent with the firm’s investment-heavy trajectory focused on long-term market leadership rather than near-term profitability [F1]. Importantly free cash flow—operating cash flow less capex—is positive at roughly $60.7 million for fiscal year 2025 signaling healthy cash conversion improving over past years [F1].

The company does not currently pay dividends nor engage in share repurchases; capital allocation prioritizes product innovation funding, scalable infrastructure buildout including cloud operations support, and sales & marketing expansion according to SEC filings through early 2026 [S4][S6][S9][S12][S15][S18]. Executive compensation policies emphasize long-term equity incentives aligned with shareholder value creation [S19][S26].

Strategic Outlook Amid IBM Acquisition

The pending acquisition by IBM—approved by shareholders as of February 12, 2026—is slated to close mid-year barring regulatory hurdles [S6][S8]. This transition marks a strategic inflection point for Confluent potentially unlocking synergies such as access to IBM’s broad client base across industries including financial services and government sectors.

Post-merger priorities likely include integrating product offerings with IBM's hybrid cloud portfolio while addressing risks related to cultural fit retention of key personnel including founders and rationalization of overlapping functions [N4][S11]. Maintaining momentum during this period is critical given macroeconomic headwinds already slowing demand expansion.

Key Milestones To Monitor (Analysis)

Without explicit forward guidance disclosed post-earnings [N1][N2], market watchers should track:

- Adoption rates of Confluent Cloud new usage accounts post-shift to consumption models.

- Expansion frequency of use cases per existing enterprise customer indicating platform stickiness.

- Margin progression as economies of scale offset cloud infrastructure costs.

- Integration updates regarding IBM transaction closing timing and operational effects.

- Competitive developments particularly responses from hyperscalers embedding Kafka-compatible or alternative streaming solutions.

- Sales cycle duration trends reflecting IT budget sentiment changes globally.

Conclusion

Confluent stands as a compelling innovator in the high-growth data streaming sector with foundational technology credibility derived from Apache Kafka origins. Its revenue gains paired with narrowing losses and positive cash flow mark progress toward a mature business model albeit challenged by evolving customer purchasing patterns and intensifying competition from deep-pocketed cloud incumbents.

The forthcoming ownership change via IBM acquisition introduces both potential upside via scale benefits as well as execution risk that bears watching closely. Ultimately the company’s ability to accelerate consumption expansion among its growing customer base while managing costs will dictate its path toward sustained profitability within an increasingly crowded streaming landscape.

This report is intended solely for informational purposes based on publicly available filings as of early 2026 without providing investment advice or recommendations regarding any securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments