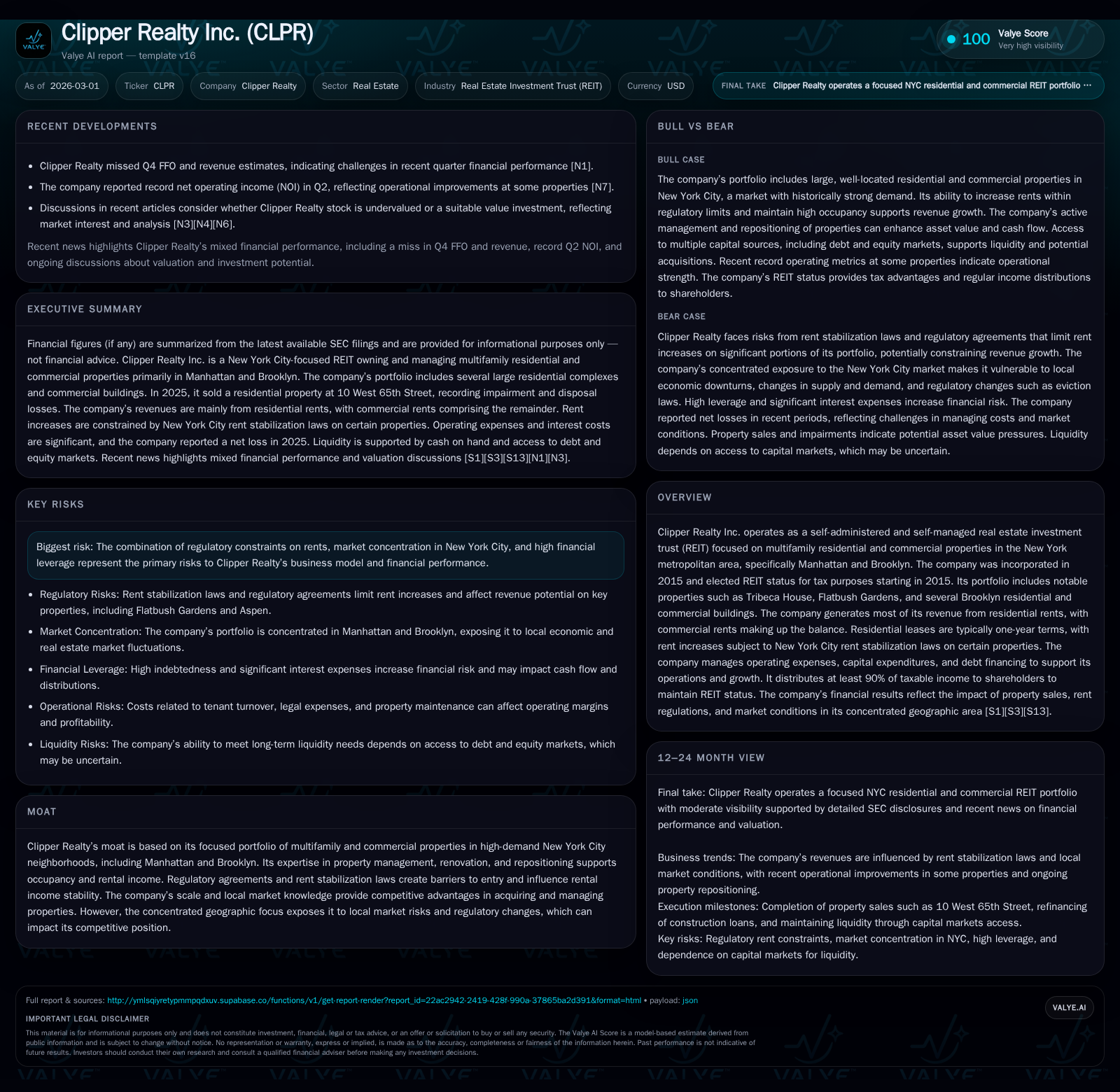

Clipper Realty’s Fiscal Turnaround and Portfolio Focus in New York’s Regulated Market

Clipper Realty manages growth and capital under NYC’s rent stabilization constraints, leveraging local expertise and selective refinancing strategies.

Clipper Realty Inc. operates a concentrated portfolio of multifamily and commercial properties primarily in Manhattan and Brooklyn, navigating New York City's complex regulatory environment. Fiscal 2025 marked a financial turnaround with operating income of $4.18 million despite ongoing rent regulation pressures and heavy capital expenditures. The firm's growth prospects depend on managing rent-stabilized assets, controlling costs, addressing elevated leverage through refinancing and asset sales, and sustaining distributions amid cash flow constraints.

Historical Performance and Revenue Drivers Through Recent Years

Clipper Realty's financial trajectory from 2018 through 2025 illustrates distinct recovery dynamics shaped by its focused NYC multifamily portfolio. Revenue expanded by approximately 9.8% year-over-year up to FY2019 reported at $30.6 million [F1], signaling steady growth from its residential leasing base concentrated mainly in Brooklyn and Manhattan. Operating income showed volatility with a steep decline leading into FY2025 when it stood at $4.18 million after prior years' fluctuations [F1]. This reflects increased cost absorption driven by regulatory compliance investments and asset repositioning.

Operating cash flow mirrored this trend; CFO was robust at $31.86 million in FY2024 before declining to $22.57 million in FY2025 amid intensified capital spending [F1]. Capital expenditures surged by over 50% year-over-year, reaching nearly $69.7 million at the latest fiscal year-end, underscoring strategic reinvestment efforts particularly in assets like Flatbush Gardens and Dean Street [F1]. These dynamics contextualize margin pressures alongside top-line resilience primarily fueled by residential rents.

Historical performance (annual)

| FY | CFO ($mm) | OpInc ($mm) | Capex ($mm) |

|---|---|---|---|

| 2025 | 23 | 4 | |

| 2024 | 32 | 41 | 70 |

| 2023 | 26 | 33 | 46 |

| 2022 | 20 | 28 | 52 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 18 | |

| 2024 | 18 | -38 |

| 2023 | 17 | -20 |

| 2022 | 17 | -32 |

Source: SEC companyfacts cache [F1].

Note: The sharp decline in operating income between FY2024 and FY2025 likely reflects restructuring expenses or impairments without specific line item disclosures available [F1].

Impact of Rent Stabilization and Regulatory Agreements on Rental Income

The company's revenue is heavily influenced by New York City's comprehensive rent regulation framework which constrains rent increases and affects occupancy economics across its multifamily portfolio [S1],[S18]. Key assets like Flatbush Gardens operate under a forty-year Article 11 agreement with the NYC Department of Housing Preservation mandating rents aligned with median income groups while providing supplemental Section 610 rental assistance for tenants receiving government subsidies [S1]. This support supplements base rents but restricts resets to market rates.

Further constraints arise from the Housing Stability and Tenant Protection Act of 2019 (HSTP), which caps annual rent increases at approximately 3% for one-year leases and up to about 4.5% for two-year leases effective October 1, 2025 [S1]. Certain newer developments such as Tribeca House have fewer restrictions but are subject to recently enacted "Good-Cause eviction" protections introduced in April 2024 that could impact turnover profitability [S1]. Additionally, properties like Dean Street benefit from a tax abatement program requiring affordability set-asides that temper market-rate potential [S1].

These regulatory layers require Clipper to carefully balance compliance with revenue optimization through turnover management, tenant retention programs, and renovation-driven value enhancement strategies.

Growth Prospects within a Concentrated NYC Multifamily Portfolio

Clipper Realty's expansion remains geographically concentrated primarily in Brooklyn and parts of Manhattan [N1],[S4],[S5],[S6]. This concentration enables deep local market expertise facilitating opportunistic repositioning initiatives such as the Dean Street high-rise development financed through substantial bridge loans totaling approximately $142 million drawn mostly at closing [S4][S5][S8].

Recent divestitures, including the sale of the Midtown Manhattan property at 10 West 65th Street, have provided liquidity for upgrades or potential pipeline expansion [N1],[S6]. Lease extensions with key tenants like Equinox at Tribeca House through August 2040 stabilize cash flows but limit rental growth unless incremental increases can be negotiated within regulatory caps accounting for inflationary pressures [S12].

Development projects supported by tax incentive programs—such as Section 421(a) abatements tied to affordability requirements—reflect an approach blending growth ambitions with regulatory compliance mandates typical of the NYC environment [S1],[S18]. These initiatives carry standard construction risks plus leasing timing uncertainties affecting funds from operations pacing.

Recent Quarterly Earnings Trends and Market Sentiment Insights

In February 2026, Clipper reported Q4 results missing Funds From Operations (FFO) and revenue estimates, underscoring challenges balancing cash flows against heavy capex outlays and leasing headwinds [N1],[S3]. Market perspectives vary; some investors consider current valuation levels undervalued relative to net asset value given stabilized regulated rents while others caution on covenant stress points linked to leverage highlighted in lender communications [N2],[N4],[N6].

FFO remains a critical metric for REIT investors emphasizing recurring adjusted earnings excluding non-cash depreciation yet incorporating normalized operating expenses [N1][S3]. Consequently, quarterly FFO deviations warrant scrutiny given their importance to sustaining dividend distributions.

Capital Structure, Liquidity, and Debt Refinancing Strategies

As of December 31, 2025, Clipper’s net indebtedness stood near $1.28 billion (net of issuance costs), secured mainly by its properties; equity was negative approximately -$30.7 million reflecting cumulative deficits or impairments over time [F1],[S4]. Major mortgages include Flatbush Gardens ($329 million maturing mid-2032 at ~3.13% interest) plus other Brooklyn holdings with interest rates clustered roughly between ~3%–6% per annum [S19][S20].

The Company refinanced Dean Street property construction financing with a bridge loan facility up to $160 million—mostly drawn ($141.75M)—complemented by mezzanine financing bearing higher all-in rates (~13%) due to risk premiums on SOFR-indexed loans plus margins [S5][S14]. Loan covenants require compliance with debt service coverage ratios, minimum net worth thresholds (disputed but currently considered met), insurance carrier rating standards, escrow accounts including cash management accounts serving as default buffers [S15][S17].

Despite these controls, Clipper faced bond acceleration risks on its municipal office property at Livingston Street triggered by lease expirations pending new tenant arrangements; ongoing negotiations with special servicers aim to mitigate immediate liquidity pressures while preserving operational continuity [S21][S22].

Dividend Policy, Cash Flow Challenges, and Shareholder Returns

Maintaining REIT status requires distributing at least ninety percent of taxable income annually—a requirement Clipper meets regularly evidenced by dividends paid totaling about $18.45 million in FY2025 [F1],[S16]. However, capital expenditures exceeding operating cash flow produced negative free cash flow near -$47 million most recently when subtracting capex from CFO [F1], highlighting pressures on available distributable cash.

The absence of recent share repurchases indicates prioritization of balance sheet repair over shareholder returns via buybacks during this period [F1]. Sustaining dividends amid ongoing reinvestment needs may necessitate additional equity issuances or further asset sales—options challenged by current credit markets and regulatory uncertainties.

What to Watch: Future Milestones and Regulatory Developments

Upcoming financial disclosures will clarify whether recent Q4 underperformance represents temporary adjustments or signals deeper operational hurdles—monitoring FFO trends against lease renewals within allowable increases is essential for assessing sustainable distributions going forward [N1],[S18].

Lease negotiations for City-occupied commercial spaces such as those at Livingston Street will materially impact revenue stability.

Potential legislative changes affecting rent stabilization—extensions or amendments to the Housing Stability & Tenant Protection Act or new eviction moratoriums—could influence turnover costs or renter demand patterns impacting occupancy metrics over time.

Operational investments aimed at scaling property management personnel may temporarily raise overhead but intend to support longer-term stabilized returns assuming steady borough-specific fundamentals.

Risks From Geographic Concentration and Financial Leverage

Clipper Realty’s exclusive focus on NYC multifamily neighborhoods exposes it to heightened regulatory complexity relative to broader REIT peers resulting in limited yield elasticity during downturns or policy shifts [S18]. Elevated leverage amplifies risk profile; covenant breaches already noted could accelerate deleveraging via forced sales or restructurings potentially eroding equity holders’ positions .

Local market disruptions—including tenant protection law amendments or macroeconomic shocks affecting demand/supply balance—may disproportionately impair occupancy compared with more diversified portfolios.

Vigilant liquidity management alongside proactive lender engagement remains critical amid cautious acquisition strategies.

Disclaimer: This analysis is based solely on provided sources including SEC filings ([F1], [S#]) and recent news ([N#]). No projections have been fabricated beyond stated evidentiary grounding nor does it constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments