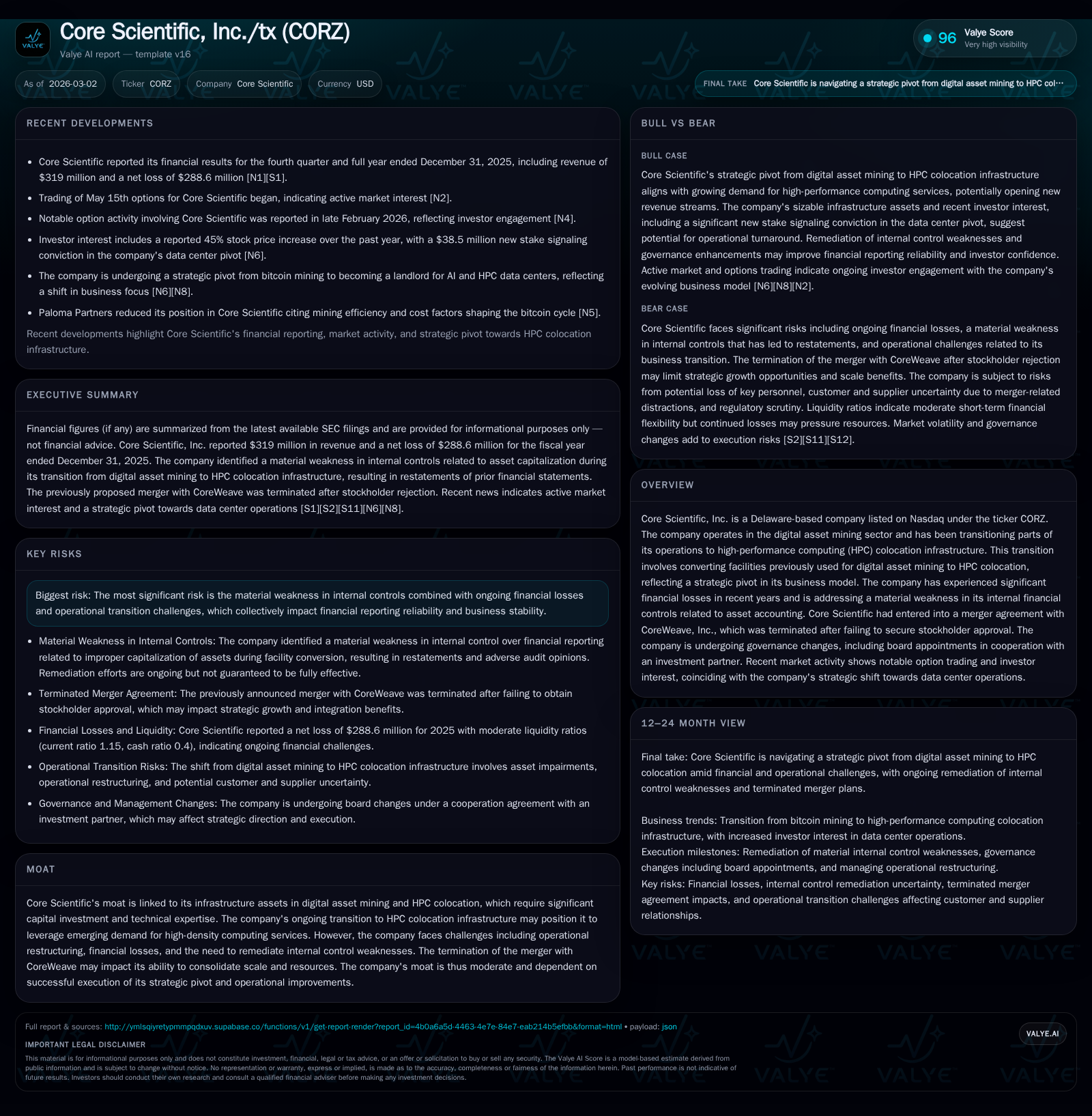

Core Scientific’s Shift from Bitcoin Mining to HPC Colocation Tests Financial and Operational Resilience

Facing steep revenue declines and operational restructuring, Core Scientific aims to capitalize on burgeoning high-density colocation demand despite legacy challenges.

Core Scientific, a once-pure digital asset miner, is pivoting aggressively toward high-performance computing (HPC) colocation infrastructure in response to crypto market volatility and evolving industry dynamics. Despite a substantial revenue drop in 2025 driven by winding down mining operations, management is monetizing a growing colocation footprint anchored by a major contract with CoreWeave. However, significant financial losses, a material weakness in internal controls related to asset accounting, and a failed merger deal weigh on near-term stability. Capital expenditures spiked sharply as facility conversions ramp up, while operational cash flow strengthened, reflecting transitioning business lines. Key milestones will revolve around successful facility conversions, expanding colocation revenues beyond a single dominant customer, and shoring up governance.

Company Summary and Business Model Evolution

Core Scientific, Inc., incorporated in Delaware and publicly traded on Nasdaq (CORZ), has transitioned from predominantly operating high-power bitcoin mining data centers to focusing largely on provisioning high-density colocation infrastructure tailored for high-performance computing (HPC) workloads, including AI applications [S1]. The firm owns or leases ten data centers across seven U.S. states with approximately 1.4 gigawatts of gross utility power capacity—a sizeable asset base developed initially for mining operations but now undergoing conversion to meet the needs of compute-intensive customers [S1].

Historically focused on cryptocurrency mining and hosting third-party miners, management initiated a strategic pivot starting in early 2024 toward enabling HPC colocation services. This pivot involves transforming existing facilities—formerly optimized for bitcoin mining—into specialized data centers supporting dense computational loads consistent with AI model training and inference demands [S1]. This evolution reflects broader industry shifts where cryptocurrency market volatility has prompted mining operators to diversify asset utilization amidst rising demand for AI computing infrastructure [N4].

Historical Financial Performance and Growth Drivers

The company reported substantial declines in revenue from $511 million in FY2024 down to $319 million in FY2025 (a -37.5% decline) as it scaled down bitcoin mining operations while ramping its nascent colocation business [F1]. Operating income deteriorated sharply from a loss of $65 million in FY2024 to a significantly larger operating loss of $246 million in FY2025 (a -275.6% change), reflecting both decreased mining-related earnings and elevated expenses related to facility conversions [F1]. Net losses remained sizeable but relatively stable at around negative $289 million in FY2025 compared to negative $291 million in FY2024 [F1].

Operating cash flow exhibited impressive growth: rising from $43 million in FY2024 to $278 million in FY2025, signaling improved cash generation linked to expanded HPC leasing activities despite overall losses [F1]. Conversely, capital expenditures surged dramatically—from $95 million in FY2024 to an outsized $729 million in FY2025—due primarily to extensive investment requirements associated with transforming mining facilities into high-performance colocation data centers [F1]. Equity remained deeply negative at approximately -$963 million by end-2025 indicating continued capital structure strain amid restructuring efforts [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($bn) | CFO ($mm) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 319 | -0.3 | 278 | -0.2 | -37.5% | +0.9% |

| 2024 | 511 | -0.3 | 43 | -0.1 | +1.6% | -18.1% |

| 2023 | 502 | -0.2 | 65 | 0.0 | -21.5% | +88.5% |

| 2022 | 640 | -2.1 | 205 | -2.1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -451 | 30.0 |

| 2024 | -52 | 30.9 |

| 2023 | 49 | 41.3 |

| 2022 | -179 | 524.3 |

Source: SEC companyfacts cache [F1].

Note: Operating income YoY figures are volatile due to business transition impacts.

Future Growth Prospects and Strategic Catalysts

Management’s key growth driver is the planned full conversion of all mining-oriented assets into HPC-focused high-density colocation facilities over the next three years [S1]. The contractual relationship with CoreWeave is central: initially inked for only 16 MW at Austin facilities early in 2024, it expanded dramatically via options exercised through early 2025 reaching nearly 590 MW of leased customer power capacity [S1]. This validates demand from a leading AI cloud player but entails concentration risk as CoreWeave currently accounts for all of the company’s HPC colocation revenue [S1].

Expansion beyond CoreWeave forms a critical future growth lever but remains unproven. Management is actively seeking additional site acquisitions and new power infrastructure opportunities to broaden its footprint beyond existing locations [S1]. Successful scaling depends on overcoming construction delays, supply chain pressures for specialized equipment such as transformers and generators, government permitting challenges, and climate-related disruptions—all noted risks associated with facility buildouts [S1].

Operationally, the company intends to continue limited digital asset mining only at converted facilities during transitional periods or under existing hosting contracts but expects this segment's contribution to decline meaningfully relative to HPC colocation revenue [S1]. Year-over-year top-line comparison metrics will likely remain inconsistent until the transition matures.

Milestones and What To Watch

Key portfolio milestones include:

- Completion timelines for converting significant megawatt capacity into fully operational HPC-ready colocation infrastructure.

- Growth trajectory of billable customer power capacity beyond the current dominant client CoreWeave.

- Resolution status of the material weakness related to internal financial controls highlighted by failure to properly impair demolished assets during conversion—a factor that triggered restatements of prior financial filings [S7][S14].

- Impact on liquidity and capital structure especially given record capital expenditures and sustained net losses.

- Board composition evolution following agreement with Two Seas Capital which included board appointments aimed at strengthening governance amid strategic shifts [S10][S17].

- Potential renewed interest or alternative partnerships following the failed October 2025 merger vote involving CoreWeave that would have accelerated scale consolidation [S13].

Absence of formal forward-looking guidance necessitates close monitoring of quarterly earnings calls and investor communications for updated commentary.

Returns and Capital Allocation

Return metrics point toward continued operational challenges despite improving operating cash flow ($278 million in FY25). Free cash flow remains negative given massive capex outlays ($729 million), resulting in an approximate free cash flow deficit exceeding $450 million annually [F1]. Equity remains deeply negative at about -$963 million implying ongoing balance sheet repair is essential.

The company has not paid dividends nor materially engaged in share repurchases recently; instead it focuses capital primarily on infrastructure development [S5][S6][S8][S9][S11][S12][S13][S17]. This allocation reflects strategic prioritization but imposes pressure on liquidity; current ratio stands near 1.15 providing some short-term buffer but requiring vigilant cash management given spending trajectory [F1].

ROE calculations are unreliable due to negative equity but indicate strained profitability relative to book value base.

Operational Risks and Governance Challenges

A pronounced risk remains around internal accounting controls tied specifically to asset accounting during facility conversion—the improper capitalization of assets scheduled for demolition led auditors to issue adverse opinions on internal controls for fiscal years ending December 31, 2024 and December 31, 2025 [S7][S14]. Management is implementing remediation plans but such weaknesses heighten execution risk.

The failed merger with CoreWeave after shareholder rejection complicates strategic consolidation aimed at achieving scale advantages critical for competing effectively against hyperscalers entering AI compute space [S13]. Governance adjustments including new independent board members nominated with input from institutional investor Two Seas aim to stabilize leadership during this uncertain phase; notable departures such as Chairman Jordan Levy not standing for re-election underscore leadership transitions [S10][S17].

Industry Context Analysis

The transformation from crypto mining rigs—which serve highly volatile markets—to HPC data centers aligns Core Scientific with macro trends favoring AI workload growth accelerated by generative AI adoption worldwide. This sector demands extreme power density per rack (often several kW per square foot), robust cooling solutions including liquid cooling adoption accelerating, reliable grid connections often paired with onsite generation backups or sustainability initiatives targeting carbon-neutral commitments being key enterprise client expectations.

While competitors include diversified large cloud providers deploying proprietary data centers along with emerging specialized AI-driven colo providers like CoreWeave itself or regional players focused on electricity cost arbitrage zones, few traditional crypto miners have successfully pivoted—a move that could define industry survivorship at the intersection of blockchain legacy assets converging with AI compute expansion.

Conclusion

Core Scientific stands at a critical inflection point dictated by its ability to transform capital-heavy bitcoin mining assets into competitive high-density HPC data centers serving burgeoning AI workloads. Revenue contraction thus far reflects deliberate wind-downs but heavy capex burdens underline that profitability remains elusive pending full conversion execution.

Concentration risk due to dependence on a single major customer—CoreWeave—in its nascent HPC segment highlights vulnerability pending diversification success. Compounding commercial uncertainties are operational control deficiencies that constrain investor confidence and pose risks around timely financial reporting improvements.

Success hinges upon executing complex physical infrastructure projects amidst supply chain constraints, proving viability outside singular long-term contracts, remediating governance issues transparently, and sustaining liquidity amidst ongoing losses—all factors that will define whether Core Scientific can emerge resiliently as an AI-era digital infrastructure player.

This report focuses exclusively on factual analysis derived from publicly available regulatory filings and reported financials without investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments