Ceragon Networks Ltd. Faces Revenue Contraction and Margin Pressure While Expanding via Strategic Acquisitions

The company leverages acquisitions to bolster its product portfolio amid challenging revenue trends and rising operating expenses.

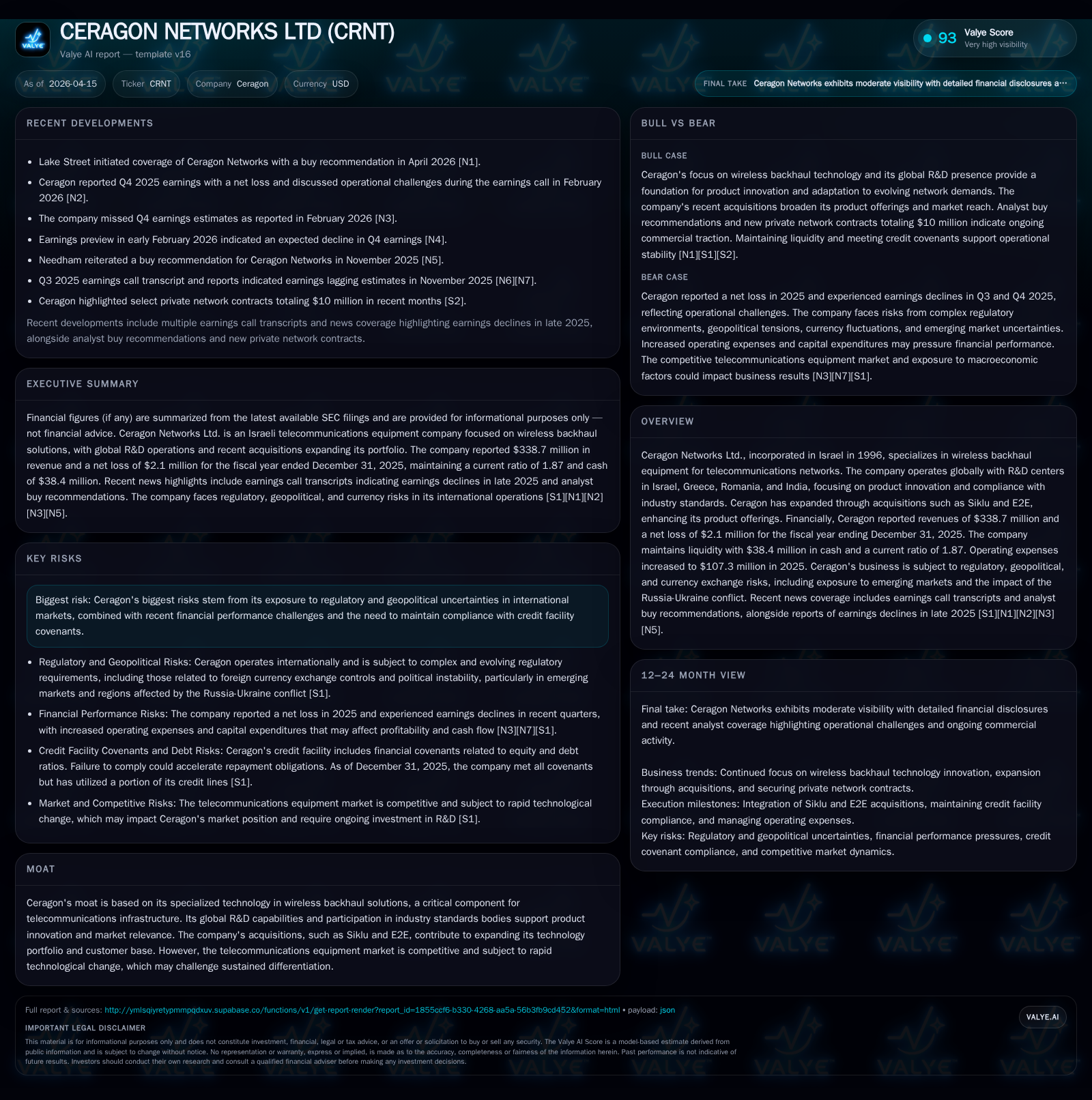

Ceragon Networks Ltd., a specialist in wireless backhaul equipment, reported a revenue decline to $339 million in 2025 from $394 million in 2024, driven by softer demand in key markets. Despite increased operating expenses and a modest net loss of $2.1 million in 2025, Ceragon maintained positive operating cash flow of $31.6 million and liquidity of $38.4 million. Strategic acquisitions of Siklu and E2E expanded its technology capabilities in multi-gigabit wireless fiber and private networks for critical sectors. Going forward, growth hinges on integrating these acquisitions, navigating geopolitical risks notably in EMEA, and managing financial covenants tied to its credit facility.

Company Overview

Ceragon Networks Ltd., established in Israel in 1996, focuses on providing wireless backhaul solutions crucial for telecommunication infrastructure globally [S1]. Its technology enables high-capacity, reliable wireless transport that supports network evolution toward advanced services such as 4G and 5G [S9]. The company conducts research and development across multiple international centers including Israel, Greece, Romania, and India – reflecting a commitment to innovation and adherence to industry standards [S1], [S11].

Ceragon has strategically augmented its capabilities through the acquisitions of Siklu Communication Ltd., a multi-gigabit wireless fiber connectivity provider acquired in December 2023, and End 2 End Technologies LLC (E2E), an integrator focused on private networks for energy and utilities sectors completed in January 2025 [S9]. These moves broaden the company’s product offerings and market reach.

Historical Financial Performance

From fiscal years 2023 through 2025, Ceragon exhibited fluctuating revenue trends marked by a peak in 2024 followed by contraction in the latest year (see Table below). Revenue grew from approximately $295 million in 2022 to $394 million in 2024 but declined by over 14% to about $339 million in 2025 [F1], [S9]. The decline was primarily due to softer demand across certain geographic regions including India and Latin America as well as competitive pressures.

Operating income followed a similar trajectory: negative in 2022 (-$10.9M), recovering substantially through 2023 ($21.2M) and peaking at a robust level in 2024 ($38.7M), before sharply contracting by over 80% to $7.25 million in FY25 [F1]. Net income mirrored this pattern with profitability attained during two consecutive years before slipping into a modest loss of $2.1 million last fiscal year.

Operating cash flows have remained positive and notably exceeded net earnings since recovery commenced post-2022 losses, with FY25 cash from operations at $31.56 million supporting capital expenditures near $13.6 million [F1]. This operational cash generation cushioned the impact of earnings volatility.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 339 | -2 | 32 | 7 | -14.1% | -108.7% |

| 2024 | 394 | 24 | 26 | 39 | +13.5% | +286.9% |

| 2023 | 347 | 6 | 31 | 21 | +17.6% | +131.6% |

| 2022 | 295 | -20 | -5 | -11 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 18 | -1.2 |

| 2024 | 12 | 14.5 |

| 2023 | 21 | 4.6 |

| 2022 | -15 | -16.4 |

Source: SEC companyfacts cache [F1].

Note: Current ratio derived from available balance sheet data [F1]

Market Segmentation & Major Customers

Ceragon operates globally but reports significant revenue exposure from major customers: In FY25, three customers alone accounted for nearly half the total revenues combined (20.7%,19.6%,7.6%) [S4]. Geographic segmentation shows North America as a key region contributing about $112.8 million or one-third of total revenues, followed by India with approximately $116.7 million [S13]. Emerging markets contribute materially but carry heightened risks.

Recent Acquisitions Enhancing Growth Prospects

The acquisition of Siklu added multi-gigabit "wireless fiber" urban connectivity products complementing Ceragon’s traditional microwave backhaul technology – potentially leveraging growing demand for urban fixed wireless access where fiber deployment is constrained [S9]. Similarly, E2E’s private network expertise targets energy/utilities verticals that require customized communication infrastructures for mission critical operations.

These strategic additions bolster product differentiation and enable expansion into fast-growing niches beyond core macro-cell transport—the latter typically characterized by intense competition and commoditization risks.

Operational Challenges & Risks

Ceragon faces notable operational headwinds such as geopolitical uncertainties prominently arising from Russian invasions affecting European markets where the company operates substantial business segments [S18], fluctuating foreign currency exposures given global sales presence necessitating hedging strategies via derivatives [S12], and complex evolving regulatory requirements imposing both compliance costs and legal challenges including ongoing class action litigation related to disclosure allegations spanning several years with potentially material liability exposure [S18].

These issues juxtapose growing demands on operating expense control amid investments for R&D innovation where annual operating expenses increased to roughly $107 million in FY25 from about $98 million prior year reflecting cost inflation plus acquisition integration outlays [F1],[S11].

Liquidity & Capital Structure

Ceragon maintains solid liquidity standing with approximately $38.4 million cash on hand as of end-December ’25 alongside credit facilities aggregating nearly $118 million [$77M loans + ~$41M bank guarantees] extended through June ’26 under an arrangement safeguarded by customary asset charges [S6,S7,S10]. Utilization remains modest with only $19 million deployed against loan facilities at low-to-mid single-digit interest rates (4.94%-6.44%) signaling prudent leverage management [F1],[S10].

Financial covenants embedded within credit arrangements require maintenance of minimum equity thresholds excluding intangibles as well as ratios limiting net financial debt per working capital/accounts receivable—criteria successfully met through FY25 without breaches reported [S10],[S12],[S22].

Capital Allocation & Shareholder Returns

Ceragon has historically financed operations via IPO proceeds supplemented by periodic follow-on offerings, option exercises, operating cash flow generation, as well as bank loans secured through their revolving credit facility [S22]. Dividends do not appear significant or declared recently per filings while equity incentive plans remain active post-2024 adoption promoting employee retention aligned with long-term innovation goals [S21].

No material share repurchases are indicated suggesting capital conservation focus amid ongoing investment needs.

Future Outlook: Catalysts & Constraints (Analysis)

Growth Drivers:

- Synergistic integration of Siklu’s "wireless fiber" technology may unlock urban market penetration opportunities ideally suited for fixed wireless access deployments.

- E2E acquisition positions Ceragon well within critical infrastructure verticals demanding proprietary private networking solutions.

- Continued investment in R&D potentially yields new generation wireless backhaul product refreshes catering to evolving telecom standardization driving upsell potential.

Potential Headwinds:

- Persistent macroeconomic uncertainties coupled with regional geopolitical risk (esp EMEA/Europe markets) may depress capex budgets across telecom operators impacting order flow.

- Competitive dynamics within wireless backhaul equipment space exert margin pressure possibly amplified if product differentiation fails post acquisitions.

- Currency volatility might impact reported results despite hedging programs given substantial emerging market revenue fraction exposing earnings variability.

- Ongoing legal proceedings generate distraction load plus contingent financial exposure quantification challenges reducing risk appetite from financial partners.

- Credit facility maturity approaching mid-2026 requires refinancing or deleveraging action potentially under tighter terms hindering financial flexibility if performance deteriorates.

Key Milestones To Monitor:

- Quarterly revenue trend stabilization or resurgence affirming successful acquisition integrations.

- R&D pipeline announcements showcasing innovative deployments relevant to key customer segments.

- Updates on class action status resolving uncertainty surrounding contingent liabilities.

- Disclosure regarding refinancing / extension plans related to credit facility maturity timeline gauging covenant sustainability.

- Changes within major customer portfolios signaling business concentration risk evolution.

Conclusion

Ceragon Networks stands at an inflection point balancing near-term headwinds reflected in declining revenues and compressed profits against strategic acquisition-fueled expansion into differentiated product niches promising longer-term growth avenues grounded on sustained R&D efforts globally. Maintaining financial discipline amid external uncertainties while effectively leveraging combined portfolio innovations will critically influence its competitive positioning going forward. The company's ongoing compliance with credit facility covenants preserves liquidity flexibility but requires vigilant monitoring given looming maturities. Shareholders should closely track integration results alongside evolving geopolitical influences shaping telecom capital expenditures around the world.

This report is designed solely for informational purposes without recommendation or solicitation regarding the purchase or sale of securities or other financial instruments.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments