Cytokinetics Shifts from R&D to Commercial with MYQORZO Launch and Strategic Partnerships

The transition centers on its FDA-approved MYQORZO launch, alongside global partnerships and a complex capital structure under financial strain.

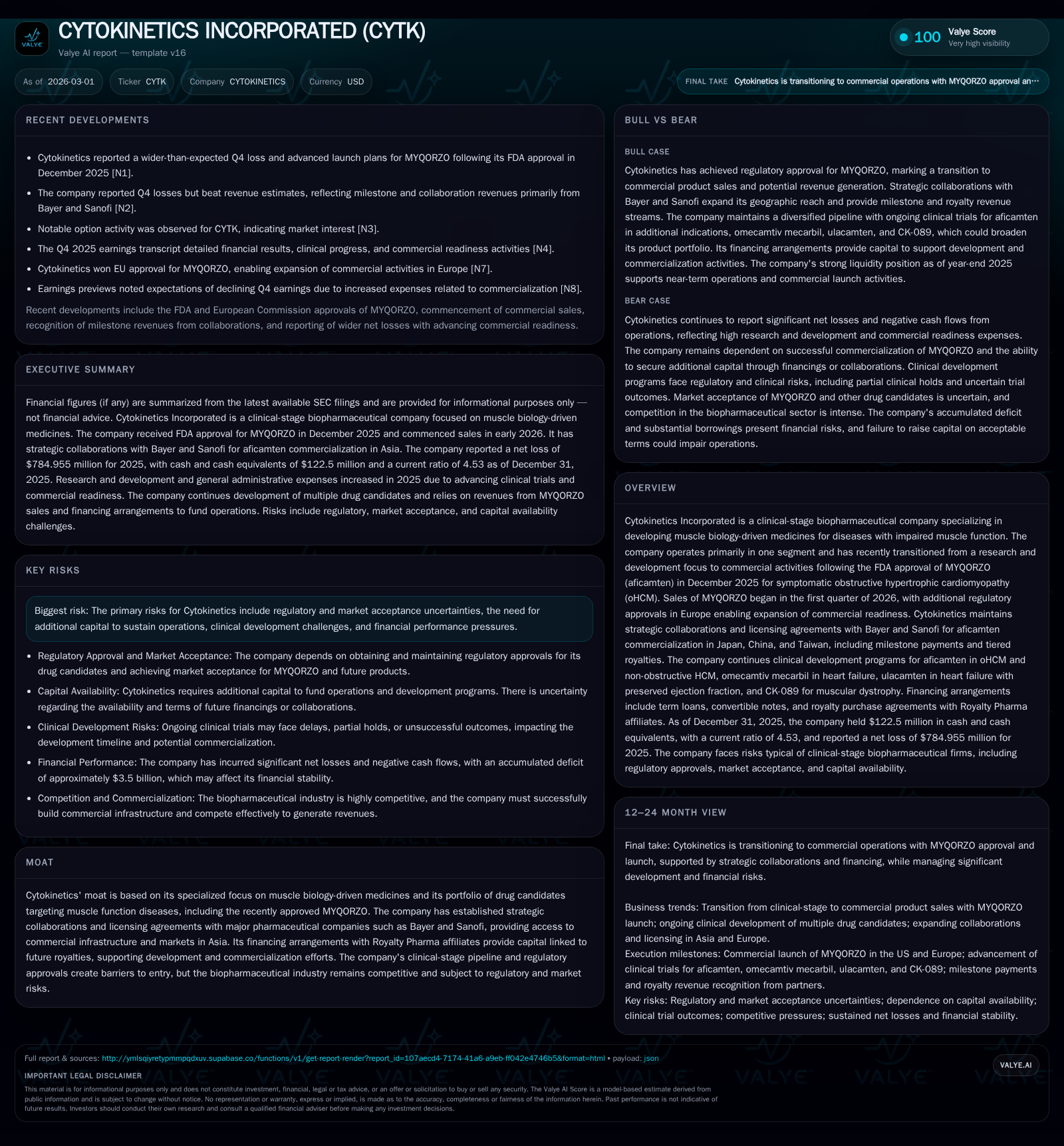

Cytokinetics Incorporated has transitioned from a research-focused stage to active commercialization following the December 2025 FDA approval of MYQORZO (aficamten) for obstructive hypertrophic cardiomyopathy. Sales began in early 2026 with European regulatory approvals supporting expansion outside the US. Strategic licensing partnerships with Bayer and Sanofi target Asian markets. Despite this milestone, Cytokinetics faces significant financial pressures from sustained net losses, heavy cash burn, and over $1.3 billion in borrowings including convertible notes and term loans. Liquidity remains a focal point as the company balances capital allocation toward commercial infrastructure while advancing pipeline clinical programs.

From Clinical Trials to Market: The Lift-Off of MYQORZO

Cytokinetics marked a significant transformation with the FDA's approval of MYQORZO (aficamten) in December 2025 for treating symptomatic obstructive hypertrophic cardiomyopathy (oHCM) ([N9]; [N7]). This approval shifted the company's focus from clinical-stage research and development toward active commercialization. Sales efforts began in early 2026 primarily within the U.S., complemented by European Commission regulatory approvals received shortly thereafter, facilitating initial entry into Germany with plans for expansion across major European territories ([N9]; [S10]).

The drug’s novel mechanism targeting muscular biology provides a competitive moat typical of specialty biopharma. Cytokinetics also leveraged strategic partnerships with Bayer and Sanofi for Asian markets such as Japan, China, and Taiwan through licensing agreements that include upfront payments, milestones, and tiered royalties tied to sales performance ([N9]; [S1]). These collaborations extend geographic coverage beyond North America/Europe and provide financial support for scale-up.

Revenue Profile and Operating Results Through Recent Years

Prior to commercialization, Cytokinetics' revenues were primarily from strategic alliances rather than product sales. Historical revenue declined markedly from $106 million in 2016 to approximately $13 million in 2017 due to research-phase focus ([F1]).

Operating losses have deepened over recent years, with operating income deteriorating from -$324 million in 2022 to -$612 million in 2025 ([F1]). Net income followed similar trends, reaching nearly -$785 million last year.

Operating cash flow reflected increasing cash burn: -$299 million (2022), worsening annually before hitting -$510 million in 2025 ([F1]). Capital expenditures surged by over fivefold between 2024 and 2025 as commercial infrastructure needs grew.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -785 | -510 | -612 | 25 | -33.2% |

| 2024 | -590 | -396 | -536 | 4 | -12.0% |

| 2023 | -526 | -414 | -496 | 1 | -35.3% |

| 2022 | -389 | -300 | -324 | 11 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -535 | 119.0 |

| 2024 | -400 | 435.5 |

| 2023 | -416 | 136.2 |

| 2022 | -311 | 360.5 |

Source: SEC companyfacts cache [F1].

Note: Latest revenue figure available is historical (2017); recent top-line primarily collaboration-based prior to commercialization ([F1]; [S2]).

Commercial Growth Catalysts: Partnerships and Global Reach

Strategic alliances underpin Cytokinetics’ commercial strategy. Licensing deals with Bayer and Sanofi provide upfront fees plus milestone payments linked to development progress and sales volumes in Asia-Pacific markets ([N9]; [S2]). These partnerships facilitate expansion where direct sales operations are less feasible.

Royalty monetization agreements have also provided capital supporting R&D funding alongside launch expenses ([S18]; [S24]). Bayer’s pharmaceutical presence combined with Sanofi’s regional reach broadens MYQORZO distribution outside US/Europe.

Regulatory Approvals and Geographic Expansion Opportunities

Following FDA approval in December 2025, European Commission authorization enabled marketing of MYQORZO for symptomatic oHCM patients ([N9]). This timely regulatory progression aligns with PDUFA target dates, accelerating regional acceptance.

Future regulatory milestones include additional indications such as non-obstructive hypertrophic cardiomyopathy along with submissions for other territories as disclosed by the company ([N7]; [S5]). The phased rollout corresponds with typical pharma commercialization approaches optimizing reimbursement readiness.

Financial Health Check: Cash, Debt, and Liquidity Dynamics

At December 31, 2025, Cytokinetics held $122.5 million in cash plus approximately $1.1 billion in short- and long-term investments totaling about $1.22 billion liquid assets ([S4]; [F1]). This liquidity contrasts with borrowings exceeding $1.3 billion — including term loans ($297.6M), convertible notes ($890.6M), plus liabilities related to royalty purchase agreements ($137.2M) ([F1]; [S6], [S18], [S19]).

Working capital remained robust at $714.5 million supported by current assets well above liabilities despite ongoing operating losses ([F1]; [S21]). However, accumulated deficits near $3.5 billion weigh heavily on equity which was negative approximately $660 million at year-end ([F1]).

Debt leverage partly stems from Royalty Pharma-related financing structures designed as non-dilutive capital but imposing repayment obligations contingent on drug success — illustrating complex pharma funding balancing risk among investors ([S13], [S14], [S18], [S24]).

Capital Allocation and Return Metrics: Past Trends and Present Strategies

Capital deployment prioritizes pipeline advancement plus commercial infrastructure rather than dividends or share repurchases — none reported recently per available data ([F1]). Negative free cash flow approximates half a billion dollars (-$534M), reflecting significant outflows driven by R&D intensity coupled with rising SG&A related to commercial transition ([F1]; [S2]).

Given extensive negative retained earnings and negative equity book value, return on equity metrics are not meaningful if estimated ([F1]). Reinvestment focuses on late-stage clinical programs including aficamten extension studies alongside next-generation muscle biology therapeutics.

Risks, Legal Challenges, and Market Acceptance Factors

A pending stockholder class action lawsuit alleges misleading statements about aficamten NDA timing potentially affecting investor confidence; the case is unsettled pending motions after the lead plaintiff amended complaint deadline March 10, 2026 ([S7]; [S12]).

Regulatory risks persist given potential delays or denials inherent in drug approval processes while market uptake uncertainties coupled with reimbursement challenges could temper revenue ramps early post-launch ([S5], [S12]).

Continued financing needs remain critical should cash burn outpace revenues; future fundraising could dilute shareholders or impose restrictive covenants impacting operational flexibility ([S2], [S6], [S17]).

Upcoming Milestones and Pipeline Development to Watch

Beyond oHCM indication expansion for aficamten/MYQORZO lie planned Phase III studies targeting non-obstructive hypertrophic cardiomyopathy treatment broadening patient reach ([N7]; [N2]). Work continues on omecamtiv mecarbil — a cardiac myosin activator targeting heart failure — with pivotal trials ongoing alongside licensing deals aimed at Asian markets poised for future contributions ([N2]; [S16]).

Additional regulatory submissions anticipated over coming quarters accompanied by pivotal efficacy/safety data releases will be critical for evaluating pipeline sustainability versus reliance on MYQORZO’s early commercial reception.

This analysis is based solely on information provided by company filings ([F1], [S#]) and public news sources ([N#]) as of March 2026 without speculative projections or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments