Dolphin Entertainment Sharpens Focus on Digital Brand Experiences in Q1 2026

Latest quarterly results reveal ongoing liquidity pressures but underscore strategic emphasis on expanding digital and special projects.

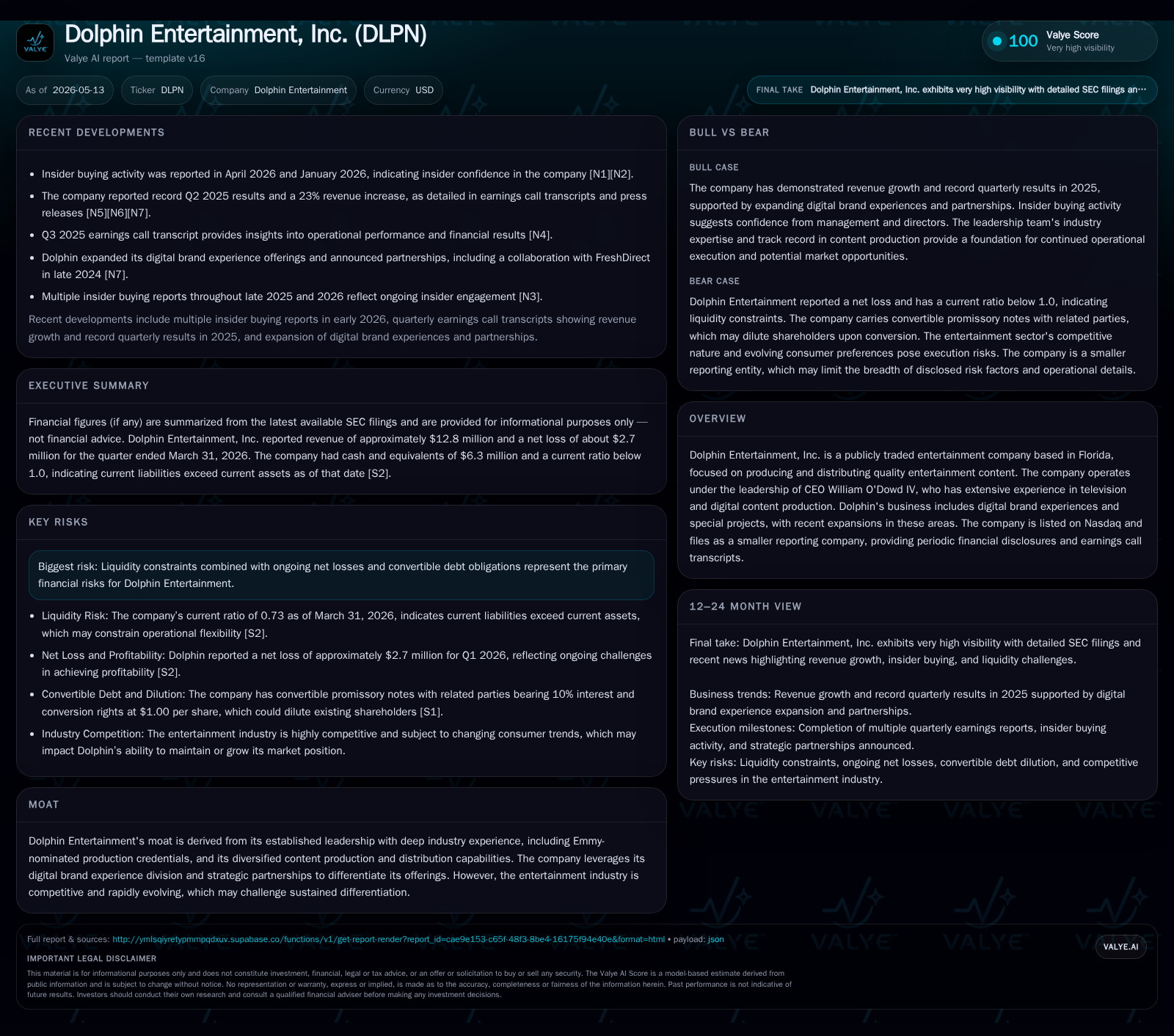

Dolphin Entertainment’s Q1 2026 filing shows a cash position of $6.28 million amid a current ratio of 0.73, indicating liquidity stress despite limited total debt. The company continues to leverage its Emmy-recognized leadership to grow digital brand experiences and special project initiatives, core components of its content production and distribution business model. While the industry’s competitive and rapidly evolving nature challenges sustained differentiation, strategic partnerships and insider buying suggest confidence in growth opportunities. Key risks remain centered on liquidity constraints and operational execution as Dolphin navigates an evolving entertainment landscape.

Latest Quarterly Operating Overview: Q1 2026 Performance Highlights

At quarter-end March 31, 2026, Dolphin Entertainment reported cash and equivalents of $6.28 million juxtaposed against current liabilities totaling approximately $27.14 million, resulting in a current ratio of just 0.73 [S2][F1]. This signals that short-term liabilities significantly outweigh liquid assets, underscoring near-term financial stress.

Despite these liquidity challenges, Dolphin maintains very modest total debt at roughly $88,000 as of mid-2025 [F1], reflecting limited leverage but failing to alleviate cash burn concerns given large operating liabilities. The Q1 filing also incorporates an earnings press release emphasizing ongoing investments in the company’s content production capabilities and expansions into digital brand experiences and special projects as primary operational focuses [S3].

The persistence of net losses compounds the liquidity narrative; while explicit quarterly income data is sparse, historical context positions Dolphin within a trend of negative bottom line outcomes driven by reinvestment commitments and slower revenue scaling [F1][S2]. The limited leverage offers some breathing room but does not fully offset the impact from working capital deficits.

Business Model and Product Offering: Content Production Meets Digital Brand Innovation

Dolphin Entertainment operates principally as a producer and distributor of entertainment content, headquartered in Florida under the leadership of CEO William O'Dowd IV, who possesses deep television and digital production experience including Emmy-nominated credentials [S1]. The company distinguishes itself through a bifurcated approach combining traditional content creation with innovative digital brand experiences.

Revenue mechanics hinge on client engagements for media projects spanning film production, event programming, branded digital content, and bespoke special projects. The latter categories have seen recent expansion, reflecting broader industry trends toward immersive brand storytelling across platforms. Customers—likely studios, brands seeking promotional material, and distributors—pay Dolphin for project-based assignments often involving contractual terms unique to each initiative.

Margins fluctuate depending on project mix; digitally focused services can command premium pricing linked to specialized capabilities and creative reputation but may face scalability limits given resource intensity and bespoke nature. The reliance on well-connected leadership facilitates client retention and strategic partnerships enabling competitive differentiation in an otherwise commoditized producer market.

Industry Structure and Competitive Positioning: Navigating an Evolving Entertainment Market

Within the broader entertainment ecosystem, Dolphin occupies a niche segment focused on content augmentation through branded digital experiences rather than mass market broadcast or streaming studio production giants [S1]. This positioning exposes the company to intense competition from larger studios with vast capital resources as well as agile boutique firms specializing in fast-turnaround digital content.

Significant industry dynamics include growing consumer migration to streaming platforms accelerating demand for diverse original content but also intensifying cost pressures. Technological advances in AR/VR and interactive media increasingly redefine audience engagement standards. Regulatory factors are less pronounced but ongoing intellectual property rights management remains critical.

Given its scale relative to major competitors, Dolphin lacks significant pricing leverage but compensates through nimble adaptation to client needs via highly customizable digital branding projects that rely heavily on skilled creative talent rather than volume production capacity [S1].

Growth Drivers: Strategic Expansion in Digital Content and Special Projects

Growth avenues center around amplifying the company’s footprint in the digital brand experience segment alongside nurturing its pipeline of special projects media assignments. These efforts capitalize on shifting consumer preferences toward immersive branded storytelling integrating social media synergy.

Recent insider buying activity noted by Nasdaq sources provides a positive signal regarding management’s confidence about growth potential in this division [N1]. The company’s ongoing strategy includes forging strategic partnerships to diversify revenue streams beyond traditional entertainment production into integrated marketing-aligned offerings.

Execution success in these areas is measurable via upcoming contract wins, project backlog announcements or renewed collaborations with known clients—operational KPIs that would provide clearer visibility into trajectory.

Additional growth depends on responding adeptly to evolving technological platforms (e.g., mobile-first video content) where Dolphin’s creative expertise can secure differentiated standing against competitors with less bespoke capability.

Risks and Challenges: Liquidity Constraints, Net Losses, and Debt Obligations

A pressing concern exposed in recent filings is liquidity insufficiency driven by current liabilities outpacing assets substantially at quarter-end March 31, 2026 (current ratio at only 0.73) [F1][S2]. This gap threatens operational flexibility unless cash flows improve or refinancing occurs.

Though outright debt levels are low—with total debt near $88 thousand—the presence of convertible promissory notes carrying circa 10% interest imposes recurring cash interest burdens compounded by principal repayment timing extending several years ahead per amendments noted in prior filings [S23][S21].

Additionally, sustained net losses erode equity buffers limiting resilience amidst shifting demand or execution setbacks typical within fast-evolving entertainment markets.

Competitive constraints may inhibit pricing power improvement while high dependency on select project revenues could increase business volatility risk profiles. Constant pressure exists on achieving operational efficiencies without sacrificing creative output quality essential for customer retention.

What to Watch Next: Upcoming Milestones and Operational Benchmarks

Investors should monitor Q2 2026 earnings disclosures for any signals addressing changes in working capital management or indications of improved cash flow generation relative to Q1’s liquidity squeeze [S3].

Announcements related to new project launches or material partnership agreements will serve as meaningful markers validating growth strategies within digital experiences expansion. Insider transactions should continue being tracked as they often presage management sentiment shifts [N1].

Contract renewals with existing clients or penetration into new market segments will be critical KPIs revealing sustainability prospects amid competitive headwinds.

Any adjustments to convertible note terms or notable changes in capital structure would materially impact financial risk assessments going forward.

Latest Financial Snapshot: Balance Sheet and Liquidity Analysis

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $6mm | |

| 2026-03-31 | ||

| Current assets | $20mm | |

| 2026-03-31 | ||

| Current liabilities | $27mm | |

| 2026-03-31 | ||

| Current ratio | 0.73x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) |

|---|---|

| Cash & Equivalents | 6.28 million |

| Total Debt | 88.3 thousand |

| Current Assets | 19.7 million |

| Current Liabilities | 27.1 million |

| Current Ratio | 0.73 |

This snapshot underscores constrained liquidity despite substantial asset holdings likely tied up in receivables or longer duration investments not readily convertible to cash within the next year [F1].

Disclaimer: This analysis is based solely on publicly available SEC filings and credible news sources as of May 13, 2026. It does not constitute investment advice or recommendations regarding Dolphin Entertainment's securities or operations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments