NETSCOUT Systems Advances Enterprise Network Intelligence With Strengthened Q3 Traction

NETSCOUT's Q3FY2026 results showcase growth in Smart Data adoption and AI integration reinforcing its presence in network observability and cybersecurity.

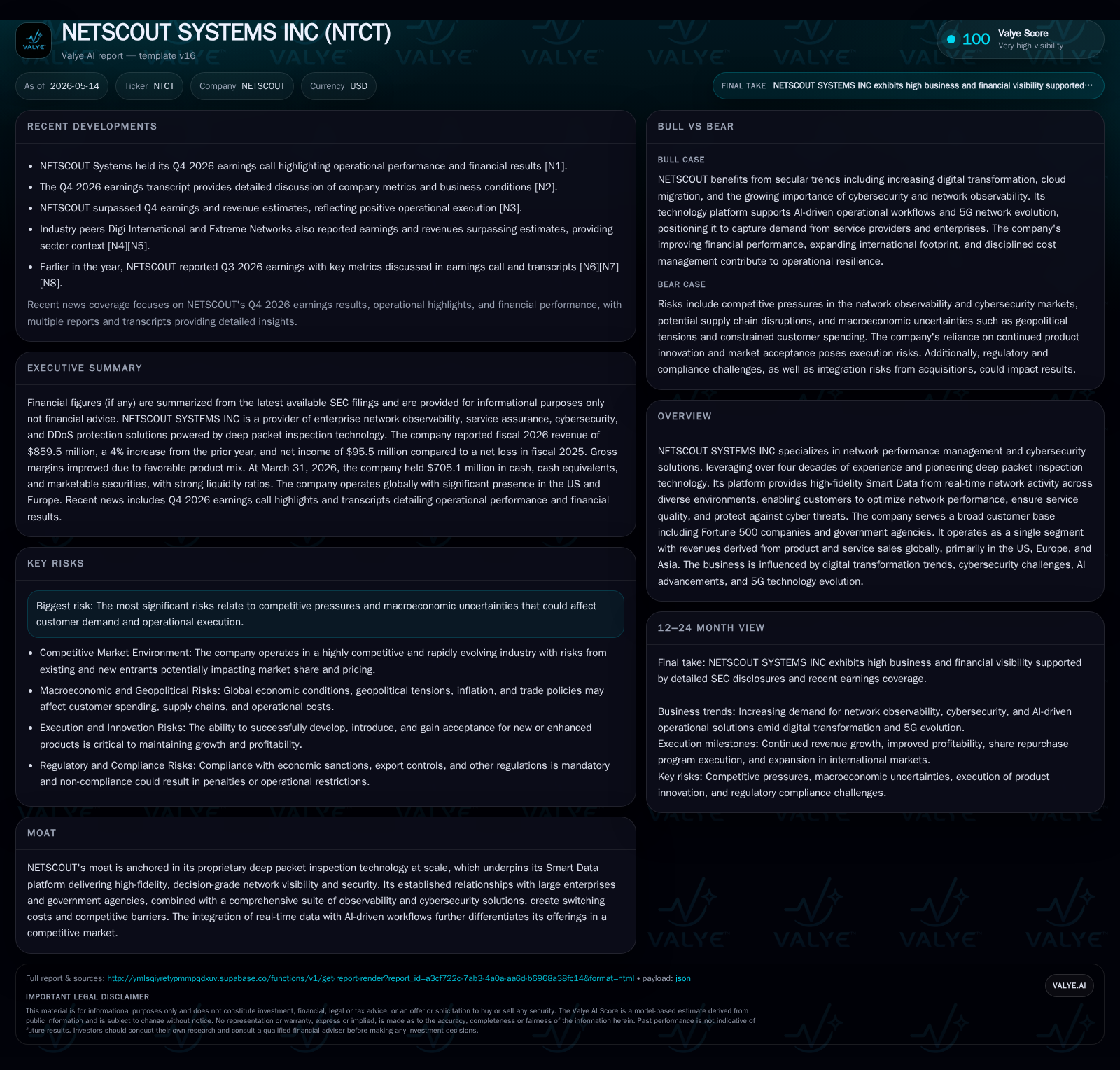

In its latest quarter ended March 31, 2026, NETSCOUT reported solid revenue growth supported by its proprietary deep packet inspection technology and expanding AI-driven analytics within its Smart Data platform. The company’s core business model leverages high-fidelity network visibility solutions mainly serving large enterprises and government clients, creating strong switching costs amid competitive cybersecurity and observability markets. Key growth drivers include broadening penetration of digital transformation initiatives, 5G technology deployment, and escalated cybersecurity spend. Risks remain around intensifying competition and macroeconomic pressures affecting IT budgets. NETSCOUT’s robust balance sheet, with over $586 million in cash, supports ongoing strategic investments and share repurchases.

Latest Quarterly Operating Update and Strategic Implications

NETSCOUT Systems’ Q3 fiscal 2026 results filed on February 5, 2026 via Form 10-Q reveal a steady ascent in revenue driven by both product and service lines. The company reported operating income of approximately $109.8 million for the quarter ending March 31, edging into positive territory after prior losses tied to goodwill impairments cleared from recent periods [F1][S2]. Revenue strength is attributed to robust demand for enterprise service assurance and cybersecurity solutions amid expanding network complexities. An accompanying May 7, 2026 Form 8-K reaffirmed this momentum with announcements emphasizing wins in new contracts and expanded scope with existing large customers that underpin a favorable near-term outlook [S3].

This uptick notably aligns with broader shifts towards increasing enterprise investments in traffic intelligence amid rising cyber threats. NETSCOUT highlights accelerating adoption of its Smart Data solutions enhanced through artificial intelligence workflows that facilitate predictive insights — fostering deeper customer engagement while improving operational efficiencies [S3][N2]. The latest earnings call underscored these themes pointing to durable demand despite macroeconomic headwinds that impact discretionary IT budgets generally [N1]. Such sustained execution provides context for NETSCOUT’s trajectory to consolidate competitive positioning.

Business Model and Differentiated Product Offering

At its core, NETSCOUT monetizes through a unified segment selling network performance management combined with cybersecurity offerings based on its flagship Smart Data platform. This platform ingests real-time network telemetry using proprietary deep packet inspection (DPI) technology at scale — a capability developed over four decades — enabling customers excellent visibility across complex multi-domain environments including cloud edges, data centers, enterprise networks, and carrier infrastructures [S1]. Products combine hardware appliances, software licenses, SaaS components, together with professional services supporting deployments and customized integrations.

Revenue streams bifurcate between tangible product sales—such as DDoS mitigation appliances—and recurring service contracts including software subscriptions for continuous threat detection or traffic analytics. Much of the customer base consists of Fortune 500 firms as well as U.S. government agencies operating mission-critical infrastructure, resulting in high retention due to entrenched switching costs tied to system complexity and depth of data fidelity required for decision-making [S1]. These integrated solutions provide a defensible moat given competitors often cannot replicate the scale or granularity of DPI-powered Smart Data nor the seamless fusion with AI-enhanced workflows.

Additionally, integrating cybersecurity capabilities—covering attack detection to rapid incident response—into the observability stack positions NETSCOUT uniquely among peers who might offer only point solutions or lack real-time data granularity. This unified approach not only optimizes network health but emboldens security posture—a critical duality amid evolving threat landscapes.

Competitive Context in Network Observability and Cybersecurity

The market landscape pits NETSCOUT against legacy incumbent rivals specializing in network management (such as Cisco’s observability suites), specialized cybersecurity vendors focusing on threat intelligence platforms, plus emerging startups leveraging cloud-native analytics. While pricing pressure persists across vendor categories given commoditization tendencies in some instrumentation areas, NETSCOUT’s DPI-driven Smart Data value proposition commands pricing resilience through differentiated technical capability coupled with tightly integrated SLAs tailored to large-scale enterprises [S1].

High switching costs arise because deep systems integration requires substantial upfront setup, customization for client-specific workflows, training personnel in operational analytics tools, plus ongoing tuning — collectively discouraging customers from migration absent critical lapses or cost differentials. Capacity-wise, the platform scales well amid the proliferation of data volumes generated by 5G rollouts and edge computing initiatives but depends on continuous R&D investment to keep pace with evolving protocols and emerging threat vectors especially targeting hybrid cloud topologies [N4][N5].

This dynamic fosters a competitive moat while engendering innovation pressure requiring agile product development cycles to maintain differentiation.

Key Growth Drivers: Smart Data, AI Integration, and Market Dynamics

Several structural tailwinds concurrently underpin NETSCOUT’s growth runway:

- Smart Data Penetration: Adoption metrics suggest growing footprint within existing accounts via upsell of AI-augmented analytics modules driving higher recurring revenue contribution alongside perpetual license renewals [S2][S3].

- AI-Driven Workflow Automation: Enhanced automation embedded into observability pipelines improves mean-time-to-detection/resolution (MTTD/MTTR), an increasingly valuable KPI for large networks coping with complexity; this innovation smooths renewal cycles while attracting new logos seeking predictive capabilities beyond legacy monitoring techniques [S3].

- Digital Transformation Investments: Broad shifts such as cloud migrations to hyperscalers or private clouds amplify demand for scalable telemetry collection covering hybrid-multicloud environments—core use cases for DPI-powered visibility platforms like those offered by NETSCOUT [S1].

- Cybersecurity Spend Escalation: Evolving regulatory environment plus sophisticated attack vectors increase budgets earmarked for integrated defense mechanisms combining network visibility with threat intelligence—a sweet spot for NETSCOUT offerings.

- 5G Technology Rollout: Both telco carriers and enterprise verticals deploying 5G infrastructure boost demand for granular traffic monitoring platforms capable of dissecting new protocol stacks at scale—again favoring seasoned DPI specialists.

These drivers reflect secular rather than cyclical forces anchoring long-term expansion opportunities measurable through contract renewals rates, average deal sizes progressing towards managed services components, geographic market penetration especially in Asia-Pacific regions showing early uptick [S8][N3].

Risks and Constraints: Competitive Pressures and Macroeconomic Factors

Despite foundational strengths there are material risk factors to consider:

- Intensified Competition: Entrants leveraging cloud-native architectures or advanced AI-only approaches could erode differentiation if NETSCOUT experiences slower adaptation cycles; meanwhile traditional large-scale vendors wield strong distribution or bundling advantages challenging market share gains [S1].

- Pricing Pressure on Renewals: Customers facing IT budget constraints under macroeconomic slowdown may seek higher discounting on software renewals or shift towards lower-cost alternatives affecting margin profiles.

- Supply Chain Complexity: Hardware appliance components remain partly subject to global component shortages which could strain delivery timelines impacting customer satisfaction.

- Regulatory & Geopolitical Factors: Expanding international operations expose the company to export controls risk as well as compliance overheads that may affect sales cycles especially within government-related segments [S12].

These risks necessitate vigilant execution particularly around balancing R&D investments against margin preservation while sustaining go-to-market effectiveness under varying economic climates.

Milestones to Monitor: Guidance, Contract Wins, and Innovation Pipeline

Key upcoming indicators relative to company trajectory include:

- Next quarterly earnings guidance updates reflecting pipeline conversion rates post recent contract wins disclosed in Q4 events filings providing early signals of traction continuity ([S3],[N1],[N2]).

- New product launches embedding advanced machine learning enhancements scheduled within upcoming R&D roadmaps hinting at further Smart Data differentiation ([S9],[S23]).

- Geographic expansion progress notably within Asia-Pacific markets where digital infrastructure investments are accelerating ([S8]).

- Renewal rates on multi-year agreements reflecting switching cost durability alongside upsell success.

- Integration milestones linking DPI data outputs seamlessly into broader enterprise automation ecosystems critical to staying ahead competitively.

Tracking these measures offers tangible insight into maintaining sustainable growth amidst competitive pressures.

Financial Overview: Liquidity, Profitability, and Capital Allocation

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $586mm | |

| 2026-03-31 | ||

| Current assets | $868mm | |

| 2026-03-31 | ||

| Current liabilities | $470mm | |

| 2026-03-31 | ||

| Current ratio | 1.85x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

NETSCOUT finished Q3 FY2026 in a strong financial position bolstered by significant liquidity:

| Metric | Amount (USD) |

|---|---|

| Cash & Equivalents | $586.5 million |

| Current Assets | $867.9 million |

| Current Liabilities | $470.1 million |

| Operating Income FY26Q3 | $109.8 million |

The current ratio of approximately 1.85x underscores ample short-term coverage ability highlighting prudent working capital management [F1]. Additionally, no borrowings were outstanding under the $600 million revolving credit facility as of March 31, indicating solid financial flexibility paired with disciplined capital allocation policies including ongoing open-market share repurchases totaling around one million shares during Q3 FY2026 endorsing shareholder value strategies without compromising liquidity buffers [F1][S6].

Profitability improvements stem largely from enhanced product mix favoring higher-margin software licensing revenues plus operational leverage gained through tighter expense control post restructuring initiatives completed in prior periods [F1][S2].

Such financial footing arms NETSCOUT with resources necessary for sustained investment into innovation trajectories critical amid rapidly evolving network observability demands.

This analysis synthesizes NETSCOUT Systems Inc.’s latest SEC disclosures alongside sector-specific insights reflecting current market dynamics without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments