Blue Water Acquisition III’s Path to Acquisition: Financial Flexibility and Strategic Sponsor Changes

Blue Water Acquisition Corp. III maintains solid liquidity and transitions in sponsor ownership as it prepares for a pivotal business combination phase.

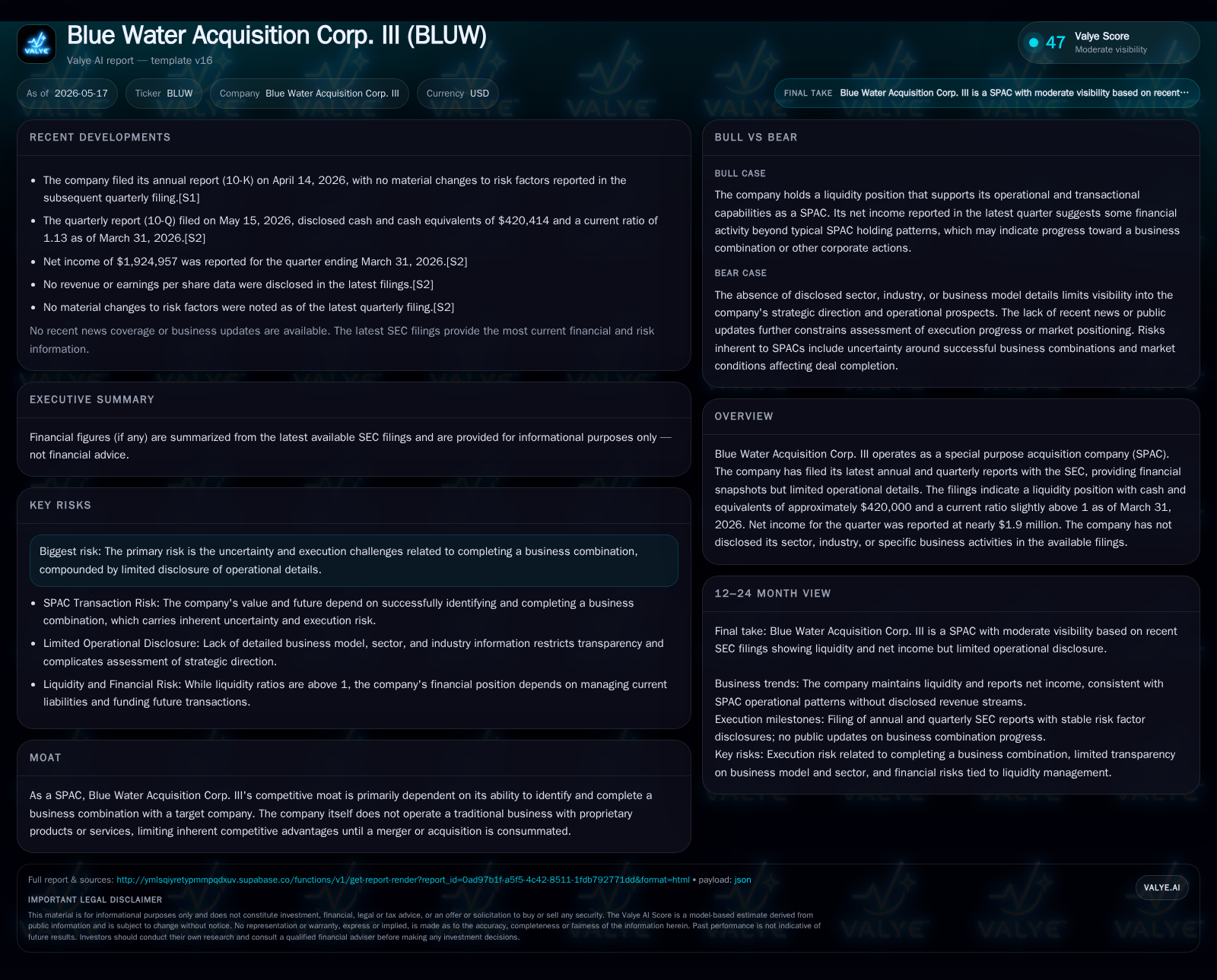

Blue Water Acquisition Corp. III's latest quarterly report reveals a stable liquidity position with cash reserves around $420,000 and a current ratio of 1.13, alongside net income of roughly $1.9 million, reflecting the typical financial activity of a SPAC pre-acquisition. Notably, the company underwent significant sponsor changes late in 2025, marking a strategic shift in governance and operational control. Its future growth hinges on successfully completing a business combination, though execution risks remain inherent to the SPAC model amid regulatory and market pressures.

Quarterly Operating Update Highlights

Blue Water Acquisition Corp. III's most recent quarterly filing dated May 15, 2026 (10-Q) discloses a liquidity position characterized by approximately $420,414 in cash and equivalents as of March 31, 2026 [F1][S2]. The company's current ratio stands at a modest but positive 1.13 [F1], indicating just sufficient current asset coverage over current liabilities ($495,814 vs. $439,786) [F1]. Net income for the quarter approximates $1.9 million [S2], consistent with normal financial activities common to SPACs (such as interest income or gains on invested trust proceeds) rather than operational earnings since Blue Water III has yet to consummate an acquisition or generate operating revenue.

This snapshot reflects the standard state of a pre-business combination SPAC: minimal operating expenditures relative to capital management activities while the company advances toward deal identification. There is no disclosed revenue-generating activity as Blue Water III remains focused on its merger search.

Business Model: SPAC Framework and Investor Proposition

Blue Water Acquisition Corp. III functions exclusively as a special purpose acquisition company (SPAC). In this capacity, it raises capital through an initial public offering (IPO) of units comprising one Class A ordinary share and one-half redeemable warrant exercisable at $11.50 per share [S1][S11]. Sponsors hold Class B ordinary shares carrying governance control rights but typically no economic rights until a merger consummates.

Revenue streams do not exist in the traditional sense before completing a business combination; the firm’s value creation depends entirely on its ability to identify and merge with an attractive private company or asset [S1]. Post-merger, Blue Water III would transition into an operating entity generating direct revenues from its acquired business.

Investors participate hoping that the new combined entity will deliver long-term value exceeding the SPAC's trust account liquidation value plus warrant potential. Until then, the company’s financial results mostly reflect administrative expenses offset by income on trust assets.

Competitive Dynamics in the SPAC Market

The SPAC market environment remains highly saturated with numerous vehicles competing for quality acquisition targets. While early SPAC booms yielded substantial capital inflows into high-growth sectors, increased regulatory scrutiny and investor skepticism have heightened transaction discipline in recent years [S7][S1].

Blue Water III lacks any innate competitive advantage beyond its sponsor group’s network strength and reputation for sourcing viable deals promptly [S1]. This structural limitation means its ultimate success depends heavily on effective deal sourcing amidst intense competition from other active SPACs.

Regulatory reforms tightened disclosure standards and imposed more rigorous timelines on SPAC mergers post-2024 market excesses, adding execution complexity [S7]. Accordingly, sponsors must balance aggressive deal-making against stringent compliance requirements.

Sponsor Transitions and Their Strategic Implications

A key recent development is Blue Water III’s strategic sponsor shift formalized through a Purchase Agreement executed November 25, 2025 [S11]. The original sponsor transferred all Class B ordinary shares (6,325,000 shares) and private placement units (430,000 units) to Yorkville BW Acquisition Sponsor LLC — the 'New Sponsor' — who now holds controlling rights over board appointments and corporate governance.

This transaction resulted in wholesale resignations of prior directors and officers at closing with subsequent appointments by the new sponsor team enhancing alignment toward merger execution [S19][S24]. The New Sponsor also executed a Joinder to become party to registration rights agreements while foregoing lock-up obligations previously imposed under predecessor agreements.

Complementing this change was issuance of updated Indemnity Agreements covering directors/officers appointed post-November 25 [S12], together with a $500,000 convertible unsecured promissory note issued January 26, 2026 for working capital purposes [S14][S26]. These measures provide operational flexibility while preserving governance risk mitigation.

Growth Drivers: Potential for Successful Business Combination

Blue Water III’s near-term value inflection remains tied exclusively to consummating a qualifying business combination within prescribed timelines generally restricted by trust account liquidation dates (often two years from IPO).

The new sponsorship enhances access to proprietary deal flow pipelines via Yorkville Advisors’ broader investment network potentially improving target sourcing quality compared to prior sponsorship structures [S11]. Adequate working capital via the promissory note supports diligence costs without immediate liquidity pressures [S26].

Success factors hinge on negotiating favorable valuations reflecting reasonable equity stakes post-merger plus shareholder approvals triggered by proxy filings once targets are announced [S2][S1]. Positive investor sentiment following announcement events can sharply re-rate trading multiples above trust liquidation values.

Risks and Constraints Surrounding Deal Execution

Execution uncertainty remains pervasive given typical SPAC lifecycle risks including delays or failures in identifying suitable acquisition candidates capable of satisfying shareholder vote thresholds within mandated periods [S7][S13]. The company acknowledges no material changes in risk profile since last annual report but retains exposure to:

- Regulatory changes potentially delaying merger approvals or increasing disclosure burdens;

- Conflicts of interest between sponsor incentives versus public shareholders;

- Illiquidity or valuation compression if market conditions deteriorate prior to deal announcements;

- Potential dilution effects from warrant conversions or working capital note conversions upon combination completion.

Lack of sector-specific disclosure further amplifies ambiguity around possible verticals targeted limiting advance evaluation clarity.

Key Milestones and What To Watch Next

As Blue Water III progresses across Q2-Q3 2026, market participants should monitor critical milestones such as:

- Public disclosure of definitive agreements securing target mergers;

- Proxy circular filings detailing transaction terms;

- Amendments or extensions filed relating to trust account lifespan if deals delay beyond initial windows;

- Warrants exercise activity signaling shareholder engagement;

- Board or management composition adjustments linked to specific target integration plans.

Adherence to these timeline constraints will materially influence fundraising success post-announcement as well as shareholder confidence before votes.

Financial Snapshot: Liquidity, Capital Structure, and Recent Results

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $420414 | |

| 2026-03-31 | ||

| Current assets | $495814 | |

| 2026-03-31 | ||

| Current liabilities | $439786 | |

| 2026-03-31 | ||

| Current ratio | 1.13x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Blue Water Acquisition Corp. III maintains sufficient liquidity headroom to support ongoing search costs without imminent financing pressure. The presence of moderate debt largely corresponds with working capital notes extended by sponsors rather than traditional lending facilities [F1][S26].

Net income reported reflects expected earnings from trust investments rather than operational performance given the nature of the entity. Maintaining positive net assets relative to liabilities supports continuity until business combination concludes.

Disclaimer: This analysis is presented solely for informational purposes without investment advice or recommendations. It summarizes publicly filed documents focusing on operational characteristics and strategic context at the time indicated by latest disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments