C21 Investments’ Growth Accelerates with Expanded Nevada Footprint and Operational Scale

Fiscal 2026 marks a milestone year for C21 Investments with its third dispensary fully contributing to revenue growth and operational leverage in the Nevada cannabis market.

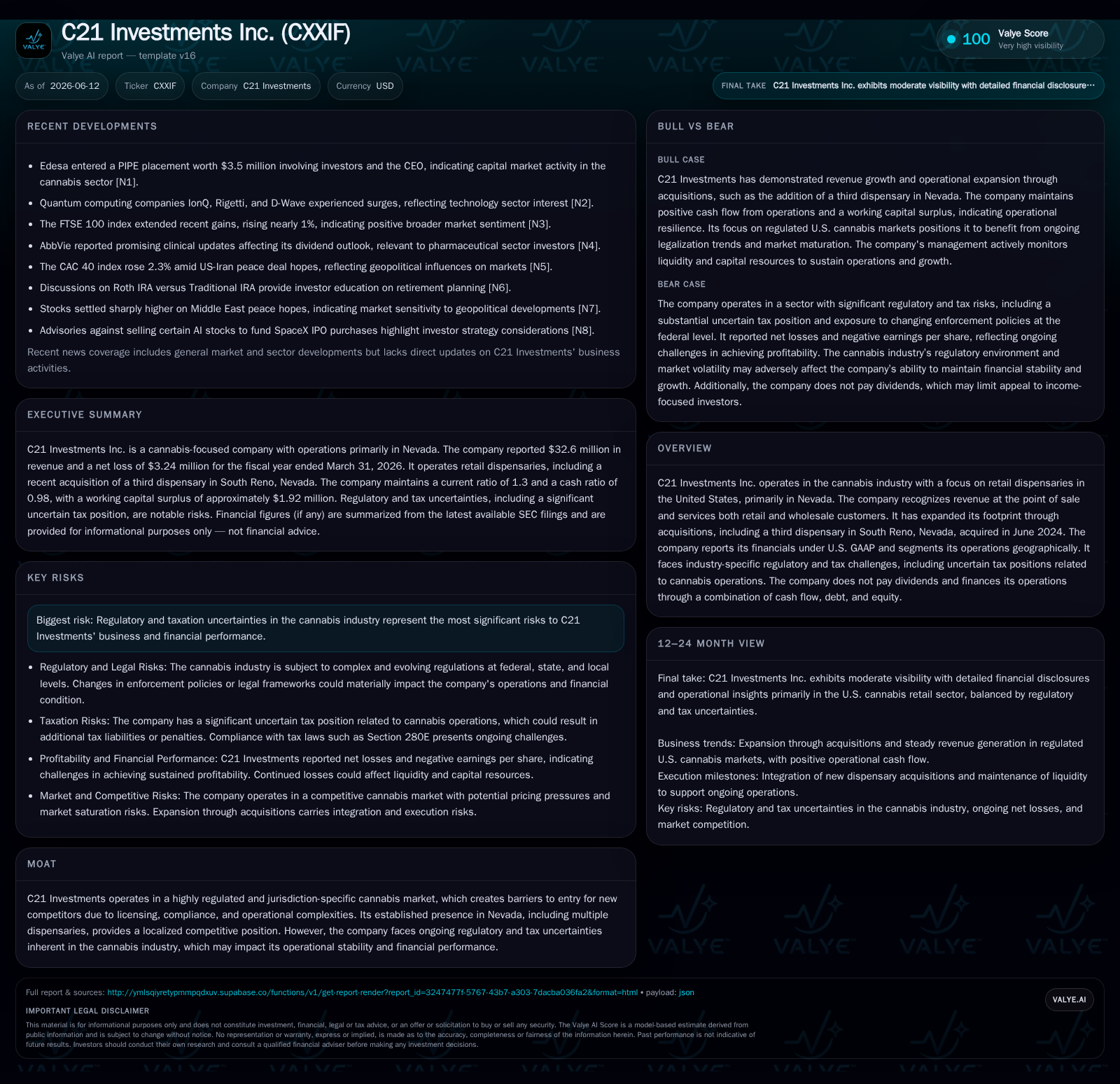

C21 Investments Inc. reported an 8.3% revenue increase to $32.6 million for the fiscal year ended March 31, 2026, driven mainly by the full-year operation of its third dispensary acquired in June 2024. Gross margins stabilized at 41.7%, reflecting economies of scale from cultivation expansion, while income from operations grew 78% despite taxation and regulatory headwinds. The company’s vertically integrated business model combines retail sales from three Nevada dispensaries with wholesale distribution via its cultivation operations. Regulatory complexity and substantial uncertain tax positions remain primary challenges impacting profitability and cash flow stability. Going forward, growth hinges on continued acquisitions, efficient scaling of cultivation, and evolving regulatory clarity.

Latest Quarterly Highlights: Operating Growth and Scale Effects

C21 Investments’ fiscal year ended March 31, 2026 showcased marked progress tied closely to its expanded retail footprint in Nevada. Total revenues climbed an appreciable 8.3% to $32.6 million compared to the prior fiscal year, chiefly reflecting the first full-year revenue impact from the South Reno dispensary acquired in June 2024 [S2][S1]. Despite a roughly 10% dip in sales at existing Nevada stores, the new location’s contribution offset softness in legacy same-store sales.

Gross profit improved by nearly $1.05 million to $13.61 million while maintaining a consistent gross margin percentage of 41.7%, mirroring last year’s result [S1]. This margin stability underscores successful economies of scale achieved through expanded cultivation capacity which lowered unit cost of cannabis production [S1]. Operating income surged by 78% to $2.28 million as higher gross profits were bolstered by a significant reduction in share-based compensation expenses (a sizeable non-cash cost) compared to FY2025 [S1]. Incremental costs related to general administration and operating leases increased modestly given the additional store overhead.

C21’s Business Model: Retail-Wholesale Integration in Nevada Cannabis Market

C21 Investments’ revenue is generated via two interlinked channels: retail sales through its network of three dispensaries located solely within Nevada—a highly regulated state market—and wholesale distribution stemming from its vertically integrated cultivation operations [S1][S2]. The company recognizes revenue primarily at the point of sale in dispensaries serving predominantly recreational cannabis customers under strict state licensing regimes.

Wholesale revenues are derived from internally cultivated cannabis sold either wholesale or supplied to own stores, helping control product quality standards and reduce dependency on third-party suppliers [S1]. The expanded cultivation facility supports downward pressure on the cost of goods sold (COGS), enhancing gross margin potential while aligning inventory management with compliance demands intrinsic to cannabis regulation [S1].

This integrated model enables C21 to manage product inventory more effectively against regulatory compliance costs tied to sourcing, storage, and transportation controls unique to the cannabis industry, positioning it strategically among local competitors within Nevada’s patchwork licensing landscape.

Competitive Dynamics and Industry Structure in Cannabis Retailing

The cannabis retail sector is shaped by stringent jurisdictional licensing requirements that limit new entrants and dictate operational scope [S1]. C21 operates exclusively in Nevada but benefits from barriers such as limited dispensing licenses that restrict market crowding—an advantage comparable conceptually to larger multi-state operators (MSOs) like Curaleaf Holdings that similarly leverage vertical integration but operate across multiple regulatory environments.

Peers like Trulieve exemplify heavy dispensary concentration paired with cultivation capabilities paralleling C21’s focus, whereas diversified operators such as Harvest Health & Recreation combine broader geographic reach with product manufacturing diversification. C21’s competitive moat rests primarily on localized expertise, regulatory navigation proficiency, and operational control over supply chain components within its territories.

However, systemic regulatory volatility especially concerning federal cannabis laws continues to inject uncertainty around operational continuity, banking access, and tax treatment—factors foundational to cost structures and capital availability [S26][S7].

Growth Drivers: Dispensary Acquisitions, Cultivation Scaling, and Regulatory Environment

The key levers propelling C21’s growth center on strategic acquisitions expanding dispensary count (now three stores), enabling higher aggregate retail volume despite some local declines; improving same-store sales is a soft spot but partially counterbalanced by expansion dynamics [S1]. The June 2024 acquisition of the South Reno store paid with cash and equity financing demonstrates management’s commitment to capitalizing on consolidation opportunities when accretive [S5].

Complementing this retail consolidation is an ongoing push for economies of scale within cultivation operations that lower unit costs through expanded production capacity—this vertical integration mitigates COGS pressures prevalent among peer retailers reliant on external sourcing [S1][S2]

Additionally, legislative developments affecting licensing fees, tax structures (notably Section 280E-related tax burdens), or banking access within Nevada could materially influence C21’s trajectory; sustained regulatory clarity remains a critical enabler for future expansion or margin stability [S26][S7]

Risks and Constraints: Regulation, Taxation, and Market Uncertainties

Among the salient risks facing C21 are high levels of taxation specific to the cannabis industry including uplifts associated with federal disallowances like IRC Section 280E which restrict deductibility of many operating expenses—resulting in large uncertain tax positions currently exceeding $13 million [S7][S6]. These tax liabilities suppress net income despite positive operating income growth.

Regulatory volatility adds layers of complexity impacting licensing renewals, compliance cost inflation (staff training, security protocols), product quality mandates, and banking restrictions that constrain financial flexibility [S26]. Moreover, consumer demand can be volatile due to competitive pricing pressures or shifts toward alternative consumption products such as edibles or concentrates.

The company’s capital structure includes debt raised specifically for recent acquisitions with monthly repayments ongoing; liquidity metrics reflect a current ratio around 1.3 indicating sufficient short-term resource coverage amid ongoing tax payments [F1][S5]

Federal cannabis prohibition risks persist as an overarching uncertainty potentially affecting long-term viability or access to capital markets should enforcement policies shift unfavorably.

Outlook: Milestones to Monitor in Fiscal Year 2027

Critical upcoming markers include monitoring same-store sales trajectories across existing dispensaries for signs of recovery or further erosion post pandemic-related disruptions; any announcements regarding additional acquisitions or expansions will signal strategic aggressiveness.

Regulatory changes concerning cannabis taxes or banking reform that reduce the burden of Section 280E or improve financial services access will substantially alter profitability outlooks.

Investors will also track quarterly cash flows closely given working capital cycles influenced heavily by inventory turnover rates under regulated constraints.

Financial Summary: Revenue Growth Balancing Profitability Pressures

Operating income improved significantly by nearly 78% climbing above $2.2 million reflecting better absorption of fixed costs and decreased share-based compensation expenses which had been elevated previously as a non-cash charge [F1][S19]. However overall net loss remained around -$3.24 million mainly driven by heavy income tax provisions totaling over $4.6 million linked primarily to cannabis-specific tax complexities [F1][S19].

Liquidity metrics indicate a current ratio of approximately 1.3 as of March 31, 2026, with current assets of $8.3 million exceeding current liabilities of $6.4 million, supportive of near-term obligations [F1]. Capital expenditures are moderate reflecting maintenance capex plus some investment supportive of franchise expansions but no major planned outlays disclosed beyond current levels [S5].

In sum, C21 Investments demonstrates advancing operational scale complemented by disciplined expense management though profitability is tempered extensively by structural taxation drawbacks inherent in U.S. cannabis businesses operating under federal prohibition.

This analysis is based on information publicly available as of June 2026 including C21 Investments' Form 20-F annual report for fiscal year ended March 31, 2026 and Form 6-K interim disclosures without any forward-looking investment advice or forecasts.

Financial position in context

Current assets of $8mm and current liabilities of $6mm imply a current ratio near 1.3x for 2026-03-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments