KRAKacquisition Corp Emerges with Strategic Prism Into Digital Asset Mergers

Following its successful IPO, KRAKacquisition Corp leverages a deep sponsor network to pursue transformative business combinations bridging decentralized and traditional finance.

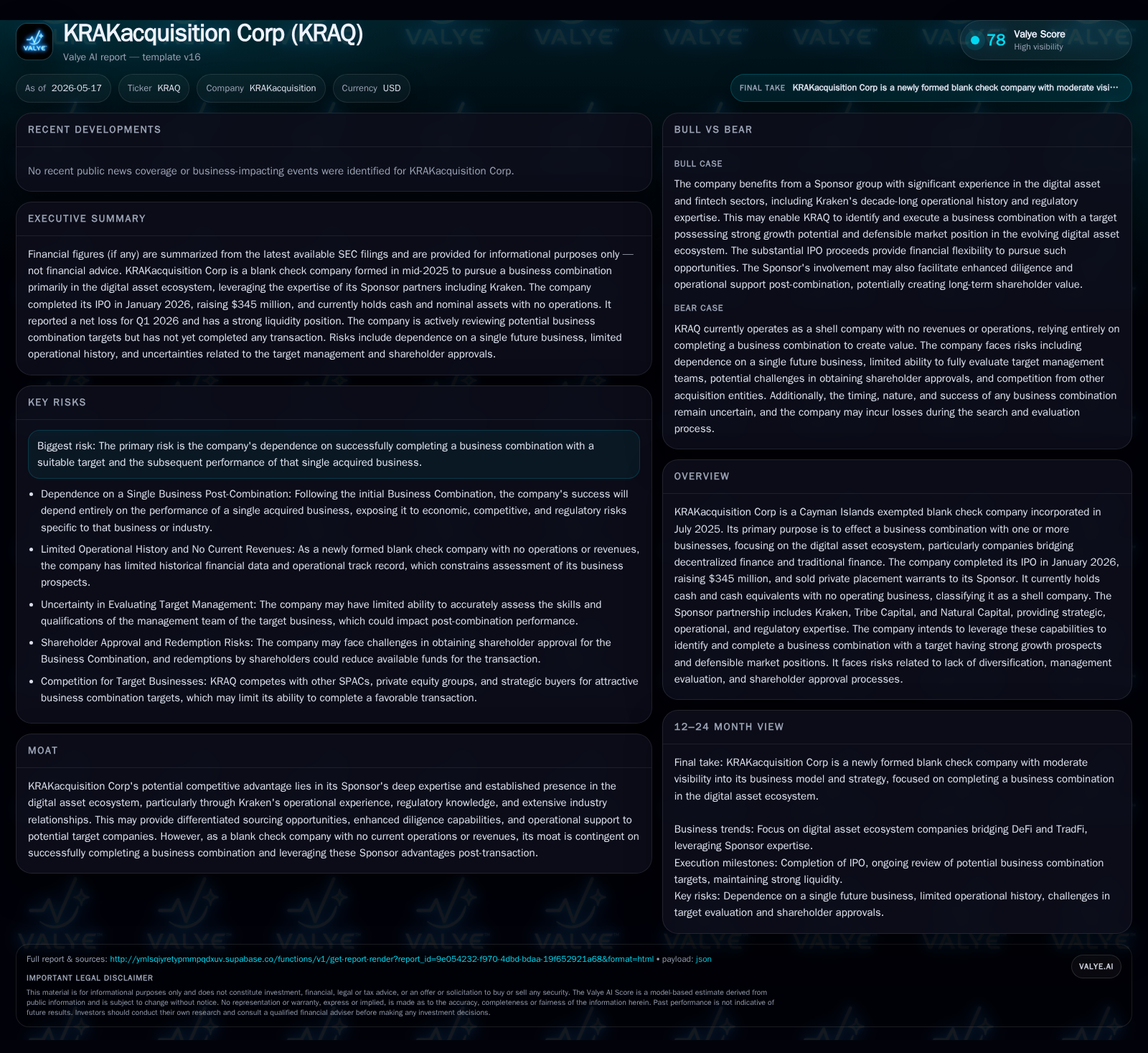

KRAKacquisition Corp, a Cayman Islands blank check company, reported in its latest 10-Q that it holds over $824,000 in cash and equivalents post its January 2026 IPO raising $345 million. The company currently operates without revenue or active business operations, focusing exclusively on identifying a digital asset ecosystem target for combination. Its unique sponsor consortium includes Kraken, Tribe Capital, and Natural Capital, offering operational, regulatory, and capital market expertise critical for deal sourcing and diligence. Despite a strong capital base and strategic inroads into DeFi-TradFi convergence sectors, the company's growth is contingent on consummating a suitable transaction amid competitive pressures and regulatory complexity.

Latest Quarterly Filing: Status and Significance

KRAKacquisition Corp’s May 15, 2026 Form 10-Q [S2] reiterates its position as a pure blank check company holding $824,617 in cash and equivalents as of quarter-end March 31, 2026 [F1]. Operating income was negative $10.9 million for the quarter reflecting pre-combination administrative expenses with no active revenue-generating operations [F1]. The company maintains a strong current ratio of approximately 7.72x driven by modest current liabilities relative to liquid assets [F1]. This financial posture underscores preparedness to deploy funds towards an initial Business Combination but also highlights complete operational reliance on executing this strategic transaction.

The filing confirms KRAQ’s adherence to Cayman Islands statutory governance while emphasizing the need to effectuate a merger or similar business combination with companies within the digital asset domain. The absence of ongoing operations validates its classification as a shell company with nominal assets primarily held in trusted escrow accounts pending investment deployment [S1],[S2].

Business Model and Sponsor Ecosystem

Incorporated in July 2025 as a Cayman exempted entity for acquisition purposes, KRAQ’s business model centers exclusively on facilitating a single initial business combination focused on bridging decentralized finance (DeFi) and traditional finance (TradFi) sectors [S1]. This typical SPAC model is augmented by its unusually potent Sponsor consortium comprising Kraken (Payward Inc.), Tribe Capital, and Natural Capital [S1],[S5],[S7]. Kraken provides industry-operational depth through its decade-plus experience operating global crypto platforms with multiple regulatory licenses spanning Europe, North America, Asia Pacific, and Bermuda [S7]. This equips KRAQ with superior market intelligence, credibility during due diligence efforts, and potential post-merger operational support rarely accessible to other blank check vehicles.

Tribe Capital adds venture capital prowess focused on fintech and crypto innovations while Natural Capital contributes strategic investment governance honed across SPACs and public markets [S1],[S5]. Together the Sponsor group synergizes capital access with operational rigor and regulatory navigation capabilities — an ecosystem advantage aimed at differentiating deal flow sourcing quality and execution precision.

This sponsorship creates valuable moat potential: enhanced deal diligence derived from Kraken’s operator lens transcends purely financial sponsor evaluations; deep industry relationships underpin preferential target referrals; regulatory experience facilitates viable public market transitions post-acquisition [S7]. However this moat is latent until consummation of a qualifying business combination occurs.

Industry Environment and Competitive Dynamics

The digital asset sector targeted is characterized by rapid technological change coupled with evolving regulatory frameworks that impose significant compliance costs on potential public companies [S14]. Candidate companies often face burdensome Sarbanes-Oxley Act implementation demands that can delay or deter SPAC mergers — constraining the addressable target universe [S8],[S14]. Moreover, accounting standard requirements for audited GAAP or IFRS financials create entry hurdles especially for smaller or earlier stage firms [S8].

Competition among acquisition entities is intense — other SPACs aiming at fintech/crypto segments alongside private equity players increasingly active in digital asset infrastructure create bidding pressure [S20]. KRAQ’s relatively large IPO war chest of $345 million offers advantages but also imposes discipline given redemption rights exercisable by public shareholders which could reduce available cash for acquisitions [S20]. The presence of warrants may introduce additional dilution considerations for sponsors and holders.

Because only around one-third of shares constitute quorum threshold for approval votes under Cayman law [S1], combined with the governance control exerted by Initial Shareholders including Founder Shares voting block, shareholder alignment complexity arises potentially affecting transaction timing or structure decisions.

Growth Drivers: Target Sourcing and Sector Outlook

KRAQ intends to focus investments primarily on enterprises accelerating the intersection of DeFi and TradFi — encompassing payment systems capable of tokenizing traditional assets, blockchain infrastructure providers facilitating programmable money flows, tokenization platforms bridging illiquid assets into tradable securities, and compliance technology mitigating regulatory risk [S1],[S5]. The thematic aligns with projected structural adoption trends within digital finance where interoperability between decentralized protocols and regulated financial systems is critical.

Target deal pipeline quality will hinge substantially on leveraging Kraken’s broad ecosystem access to identify proprietary opportunities not widely marketed. Success depends on executing accretive deals that can realize premium valuation uplifts through scale economies post-merger operational efficiencies supported by Sponsor expertise.

Unfolding regulatory clarity around digital asset exchanges globally may catalyze growth by enabling smoother transition pathways for targets into public markets. Additional growth vectors include integration potential across Kraken’s existing platform fostering synergies that enhance customer retention metrics or expand product suites.

Nonetheless these growth prospects remain entirely contingent upon closing an effective combination within required timelines given no current operating entities contribute revenues or cash flow.

Risks and Execution Challenges

Primary risks attend KRAQ’s all-in reliance on consummation of a favorable initial business combination within their authorized timeframe before trust funds must be returned to investors. Failure to complete the transaction would result in liquidation without shareholder value creation beyond IPO proceeds minus expenses [S1],[S14].

Governance provisions vest substantial influence in Founders whose shares automatically vote ‘for’ any proposed combination regardless of public shareholder opposition potentially diluting external investor power. This can raise concerns about deal pricing fairness or willingness to engage exit transactions appropriately aligned with minority investors’ interests [S1],[S14].

Potential delays or inability to source compliant targets accounting for SOX readiness or audited reporting requirements constrain available candidates further elevating execution risk relative to broader SPAC pool competition demanding similar digital asset sector deals [S8],[S14],[S20].

Post-business combination integration complexities also pose challenges especially if acquired firms are nascent or unproven commercially creating uncertainty around sustaining anticipated growth trajectories despite Sponsor operational guidance.

Upcoming Catalysts to Monitor

Key near-term milestones include announcements regarding definitive agreements or letters of intent with prospective targets signaling progress along the transaction timeline required under Cayman jurisdiction laws protecting shareholder interests [S2],[S3].

Monitoring shareholder meeting notices specifying vote procedures around the initial business combination approval is essential given the unique governance rights reserved for Sponsor Initial Shareholders alongside public investors vote counting rules under Cayman law [S1],[S3].

The March 19, 2026 8-K disclosed commencement of separate trading for Class A shares and warrants post-IPO units separation offers another liquidity event dimension influencing shareholder participation dynamics during transaction processing periods [S3],[S22]. Tracking warrant exercises volumes can provide insight into market sentiment toward planned combinations.

Regulatory filings disclosing material amendments around redemption rights timelines or fundraising activities including private placement warrants will act as barometers of strategic flexibility or capital structure shifts influencing deal-funding options ahead.

Financial Snapshot and Capital Position

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $824,617 | |

| 2026-03-31 | ||

| Total debt | $0 | |

| 2025-12-31 | ||

| Net debt | -$824,617 | |

| 2025-12-31 | ||

| Current assets | $894,264 | |

| 2026-03-31 | ||

| Current liabilities | $115,783 | |

| 2026-03-31 | ||

| Current ratio | 7.72x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value | Period Ended |

|---|---|---|

| Cash & Equivalents | $824,617 | |

| 2026-03-31 | ||

| Total Debt | $0 | |

| 2025-12-31 | ||

| Current Assets | $894,264 | |

| 2026-03-31 | ||

| Current Liabilities | $115,783 | |

| 2026-03-31 | ||

| Current Ratio | 7.72x | |

| 2026-03-31 | ||

| Operating Income | -$10,965,430 | |

| 2026-03-31 |

This concise financial picture sourced from the latest quarter filing [F1],[S2] highlights KRAQ's pristine balance sheet positioned solely with cash reserves intended for acquisition deployment. Zero debt mitigates leverage risks pre-combination though operating expenses continue contributing to net losses due to administrative overhead inherent in maintaining SPAC status without revenue streams yet realized. Overall capital adequacy supports ongoing search effort continuity though ultimate value creation depends critically on successfully structuring accretive deal terms.

This analysis has been prepared exclusively based on available SEC filings dated up through May 17, 2026 ([S1]-[S29]) supplemented by companyfacts XBRL data ([F1]). It does not provide investment advice or recommendations but aims to present an informed industry analyst perspective grounded in verified disclosures regarding KRAKacquisition Corp's operating status, strategic positioning, competitive context, growth outlooks, risks, upcoming milestones, and financial health.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments