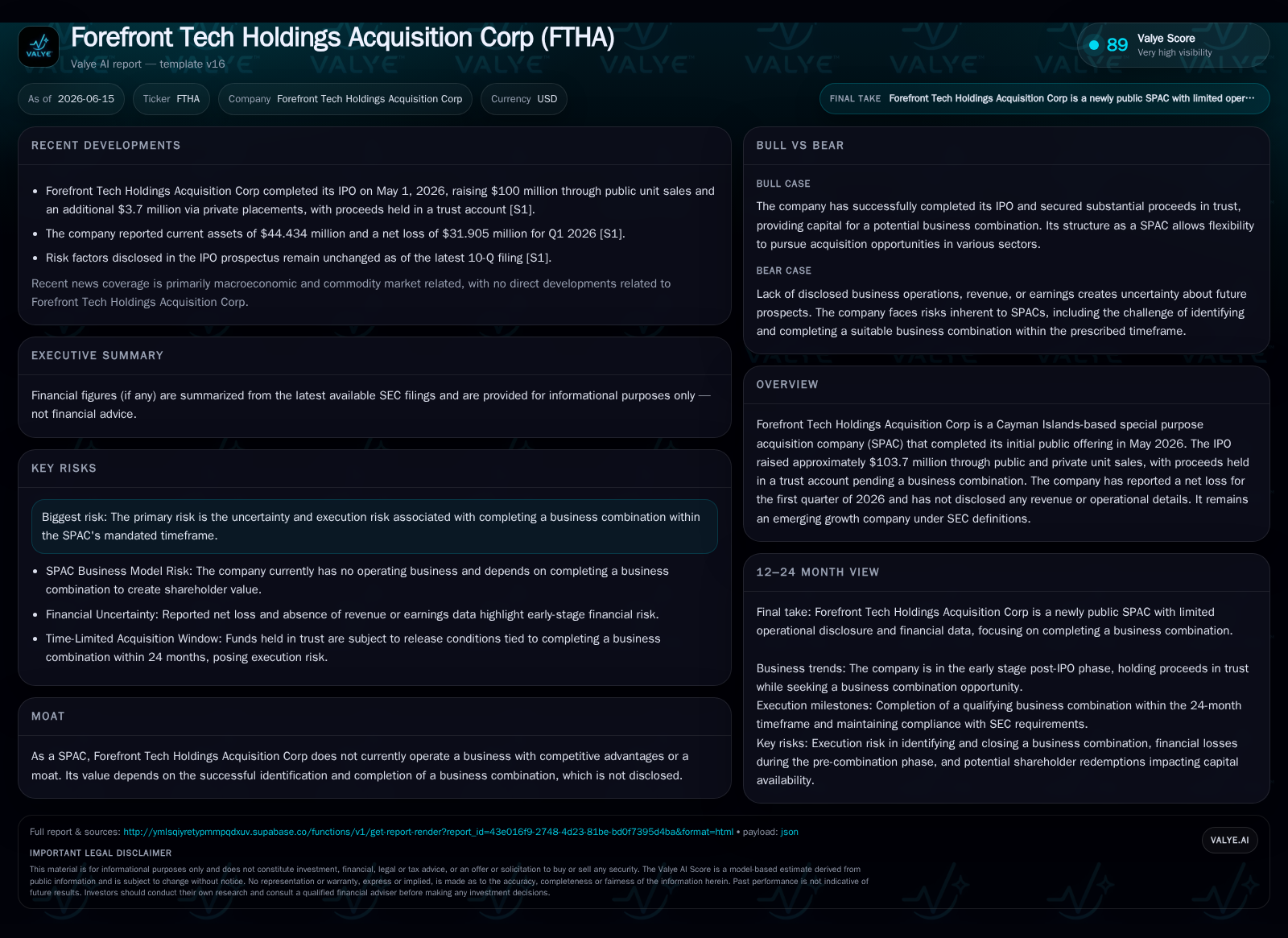

Forefront Tech Holdings Acquisition Corp's Initial Milestone: SPAC IPO Completion and Capital Structure Overview

Forefront Tech Holdings Acquisition Corp has finalized its IPO, raising $103.7 million to underpin its SPAC life cycle and future business combination efforts.

Forefront Tech Holdings Acquisition Corp completed its initial public offering on May 1, 2026, successfully raising approximately $103.7 million through the sale of public and private placement units. The proceeds are held in a trust account, earmarked for consummating a business combination within the permitted timeframe. The company remains an emerging growth entity with no operating revenues and reported a modest $31,905 net loss in Q1 2026 reflecting pre-combination administrative expenses. Positioned within the competitive SPAC ecosystem, Forefront's path hinges on identifying an attractive target and executing the de-SPAC transaction amid typical risks including shareholder redemptions and regulatory oversight.

IPO Completion Secures $103.7 Million Capital Raise

Forefront Tech Holdings Acquisition Corp officially launched its SPAC journey with the completion of its initial public offering (IPO) on May 1, 2026. According to SEC filings [S3][S6], the company issued 10 million units priced at $10 each to raise $100 million from public investors. Simultaneously, private placement sales conducted with Next Lion Sponsor Holdings LLC (the sponsor) and BTIG, LLC (underwriter) added another 370,000 units for $3.7 million in gross proceeds. Thus, total capital raised reached approximately $103.7 million.

Each unit consists of one Class A ordinary share coupled with one-half redeemable warrant exercisable at $11.50 per share [S9]. This structured composition grants holders potential future upside exposure upon successful business combination execution while imposing dilution risk later if warrants are exercised.

The entirety of the IPO proceeds was deposited into a U.S.-based trust account managed by Odyssey Transfer and Trust Company as trustee [S11]. Funds held therein will remain restricted until either Forefront consummates an initial business combination or redeems shares if unable to do so within the mandated 24-month window. This trust structure is standard within SPAC frameworks to protect investor capital while dealmaking progresses.

SPAC Business Model and Forefront’s Current Operational Status

As a Cayman Islands-incorporated special purpose acquisition company, Forefront's operations are narrowly scoped to facilitating a de-SPAC merger that takes a privately held target public [S2]. Typical of such entities early in their lifecycle, Forefront has not generated any operating revenues and recorded a net loss of approximately $31,905 for the quarter ended March 31, 2026 [F1]. These losses largely represent standard administrative expenditures including legal fees and underwriting costs incurred pre-combination.

The company maintains an emerging growth company status under SEC definitions [S3], affording certain reporting accommodations during this formative phase. At this juncture, Forefront holds no commercial assets or competitive advantages (moats), anchoring its value proposition solely on successfully completing an accretive merger with a suitable private enterprise.

Capital Structure: Units, Warrants, Sponsor Contributions, and Trust Account Mechanics

The economic interests of Forefront’s public investors derive primarily from ownership of units composed of ordinary shares plus warrants exercisable at $11.50 per share—above the initial unit price—allowing investors to gain on deal success while providing upside leverage [S9]. The warrants constitute half per unit sold; hence each unit entitles holders to purchase an additional share at the specified strike price later, potentially diluting equity post-transaction.

Sponsor economics include private placement units totaling 355,000 sold at $10 per unit generating roughly $3.55 million in additional capital alongside underwriting participation by BTIG with units worth approximately $0.15 million [S13]. These sponsor private placements typically come with promote structures granting sponsors equity interest above common shareholders once deals close.

Crucially, all capital raised—including sponsor contributions—is sequestered in the trust account pending either a de-SPAC transaction closure or orderly liquidation if no deal occurs in about two years [S11]. This guardrail ensures limited downside for public shareholders but also sets up redemption rights enabling shareholders to exit before combinations perceived as unfavorable.

Industry Dynamics: Positioning Among Peer SPACs and Underwriting Landscape

Forefront aligns with a cohort of Cayman Islands-domiciled technology-sector-focused SPACs competing to identify dynamic targets amidst robust private-market innovation cycles. Firms like Pershing Square Tontine Holdings exemplify comparably sized peers navigating similar lifecycle stages with substantial capital bases and prominent sponsors.

Underwriting support from BTIG LLC situates Forefront within established execution channels prevalent among Nasdaq-listed SPACs [S3][S9], ensuring efficient distribution of units at IPO pricing terms consistent across recent deals. Subsequent financing rounds such as PIPE placements await post-announcement to augment capital structures further and enhance transaction feasibility.

Growth Catalysts: Target Identification, Market Conditions, and PIPE Financing Potential

Value creation beyond IPO hinges heavily on Forefront’s sponsor team sourcing compelling acquisition candidates amid heightened demand among private companies seeking expedited access to public equity markets through alternative listing routes offered by SPACs. Market receptivity towards speculative growth plays another critical role influencing timing and terms available.

PIPE financings commonly provide supplementary funds post-business combination announcement by institutional investors looking for structured entry points; availability thereof can materially improve deal attractiveness by bolstering balance sheets ahead of market debut.

Operational KPIs related to velocity of deal pipeline progress—measured via time-to-business combination—and shareholder redemption rates post-announcement will serve as leading indicators for future performance potential.

Risks Spotlight: Timing Execution, Shareholder Redemptions, and Regulatory Frameworks

Forefront’s foremost risk concerns failing to consummate a qualifying business combination within the stipulated approximate two-year horizon imposed on SPACs—defaulting into wind-down scenarios where residual trust assets revert shareholders pro rata [S2][S12]. Increasing shareholder redemptions during voting phases threaten diminishing available funds for deployment even when deals materialize.

Regulatory oversight intensifies compliance demands on disclosure rigor during combinations; evolving SEC scrutiny may elevate transaction costs or slow approvals impacting SPAC timelines adversely. Dilution considerations from warrants exercised alongside sponsor-related promote interests potentially dilute returns for public shareholders if not carefully managed throughout deal structuring.

Broader macroeconomic volatility also impinges upon appetite for speculative investment vehicles like SPACs which can lead to depressed valuation multiples when target companies transition publicly.

What To Watch: Business Combination Timeline and Investor Approval Milestones

Critical forward-looking markers include announcements identifying specific private targets accompanied by detailed merger agreements triggering formal shareholder votes required under NASDAQ rules and SEC mandates. Redemption levels exercised during these votes directly influence transaction viability due to their impact on trust funds.

Subsequent warrant exercise activity post-deal offers insight into investor confidence in combined entity prospects while providing internal liquidity signals that may impact share price dynamics.

Tracking these milestones diligently will illuminate Forefront’s execution discipline against peers competing in this crowded marketplace poised for accelerated deal flow.

Concluding Financial Snapshot

As verified in recent filings [F1][S3], Forefront maintains approximately $103.7 million of cash held exclusively in trust accounts earmarked for future merger transactions while reporting minimal net losses around $31,900 through Q1 2026 attributable solely to non-operational expenses typical of pre-deal-stage SPACs. This financial profile underscores a clean balance sheet supporting runway toward target acquisition activities balanced against steady operational burn reflective of governance overheads common across newly formed blank-check issuers.

While devoid of commercial revenues or structural moats today, Forefront’s valuation trajectory strongly correlates with its ability to identify an accretive partner quickly and navigate complex approval processes effectively amidst evolving regulatory landscapes shaping the broader special purpose acquisition company industry segment.

Disclaimer: This analysis is informational only and does not constitute investment advice or research view regarding securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments