Zoned Properties Eyes Strategic Shift as Management Buyout Nears Closing

The company is advancing a management buyout and asset liquidation amid regulatory challenges in the cannabis real estate niche.

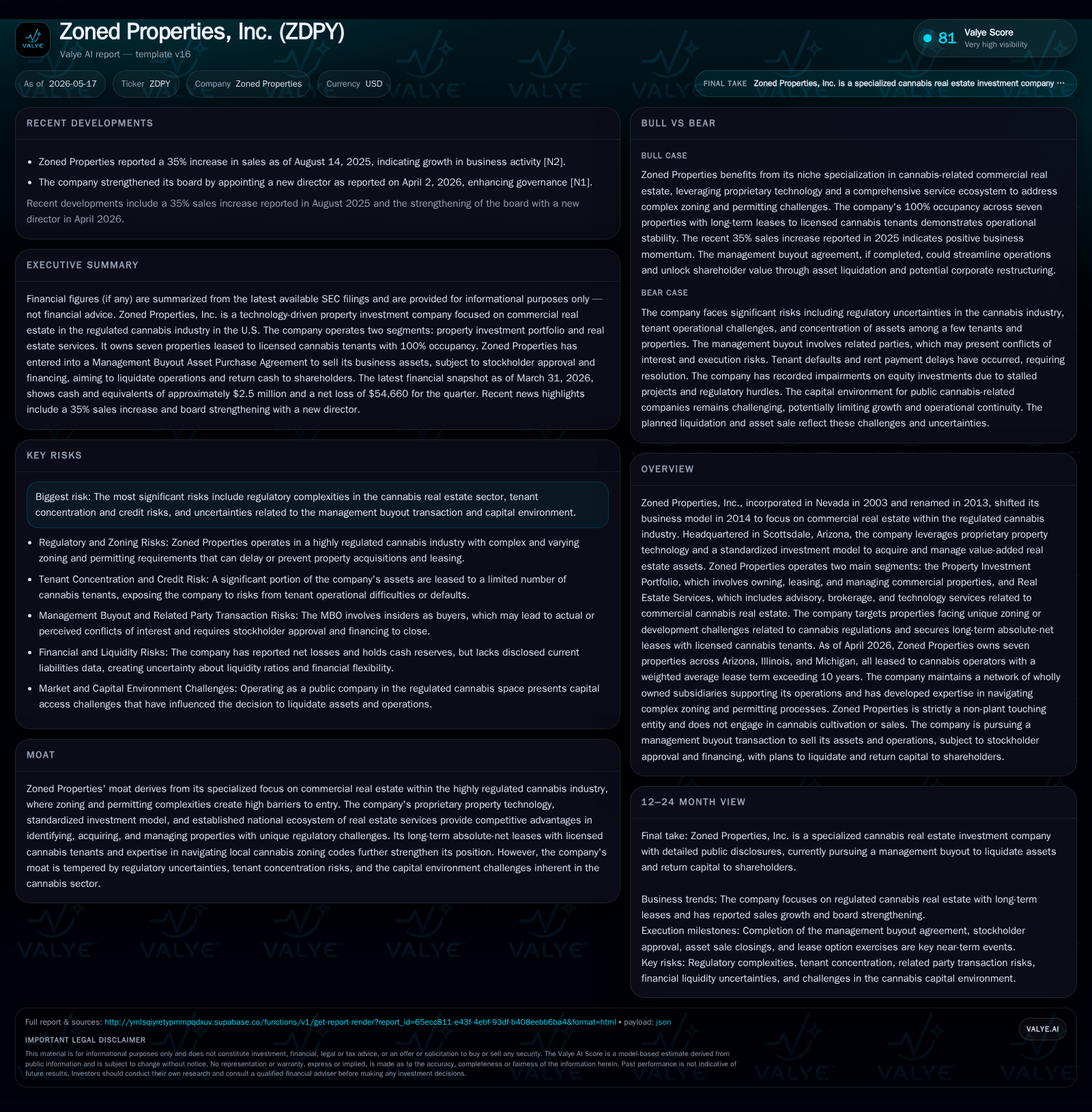

Zoned Properties, Inc. disclosed in its Q1 2026 10-Q and recent 8-K filings that it is progressing toward completing a management buyout (MBO) scheduled by the end of 2026. The MBO involves selling substantially all assets, including seven commercial properties leased primarily to cannabis operators, reflecting a strategic pivot due to capital constraints and regulatory uncertainties within the cannabis property sector. Zoned's dual-segment model—property investment with absolute-net leases and real estate services supported by proprietary technology—has created a differentiated niche underpinned by high zoning barriers. However, tenant concentration risks, financing challenges, and heavy reliance on key executives pose significant headwinds during this transformative phase.

Latest Quarterly Update and Management Buyout Progress

In its latest 10-Q filing dated May 15, 2026 [S2] and accompanying 8-K press release [S3], Zoned Properties detailed critical developments shaping its near-term trajectory: the company continues to execute on an announced management buyout (MBO) agreement entered earlier in January 2026 [S10]. The MBO involves selling substantially all assets—including seven commercial properties primarily located in Arizona and Illinois—to BPB Partners, LLC, an entity owned by Zoned's CEO Bryan McLaren and other executives. The purchase price is approximately $7 million less assumed debt obligations.

This transaction reflects a fundamental strategic shift driven by persistent financing difficulties and regulatory constraints within the emerging cannabis real estate sector. Zoned disclosed continuing asset sales of key properties (notably those in Chino Valley, Kingman, and Green Valley) under a structured plan designed to consolidate ownership ahead of MBO closing, contingent upon buyer securing adequate financing and obtaining stockholder approvals [S4][S25]. The closing window targets end-2026 but permits extensions.

Despite modestly positive cash flow from operations reported for fiscal year-end 2025 ($781k), recurring net losses persisted through that period [$F1]. The company emphasizes that unless the MBO transaction completes successfully with asset liquidation, continued operations are financially unsustainable given current capital market reluctance to engage in federally illicit but state-sanctioned cannabis industries [S1][S8]. The filings repeat warnings about substantial doubt regarding going concern status absent closure.

Zoned Properties’ Business Model and Product Offering

Zoned Properties operates a bifurcated business model with two primary segments: the Property Investment Portfolio and Real Estate Services [S1].

Property Investment Portfolio: Zoned directly owns commercial real estate tailored to the needs of licensed entities within regulated cannabis markets. These properties face intricate local zoning restrictions—a niche where Zoned leverages its expertise. The company secures long-term absolute-net leases with tenants who handle cultivating, processing, or dispensing cannabis products but where Zoned itself remains strictly "non-plant touching." These absolute-net lease agreements transfer most property-level financial responsibilities to tenants, stabilizing income streams despite regulatory uncertainty.

Real Estate Services: Complementing ownership activities, Zoned offers advisory, brokerage, and proprietary technology services aimed at facilitating cannabis-compliant transactions across states. This includes leveraging a proprietary technology platform designed to navigate complex permitting frameworks and standardize investment evaluation models.

Collectively, these segments seek to address unique cannabis zoning challenges while managing properties for optimal operational value through a network of subsidiaries within Arizona and broader U.S. markets [S1][S11]. The company underscores its reliance on due diligence processes focused on tenant creditworthiness given high industry volatility.

Competitive Positioning within Cannabis Real Estate

Zoned's moat derives predominantly from regulatory complexity creating natural entry barriers: consistently evolving municipal ordinances restrict where cannabis operations may occur—including prohibitions near schools or residential zones—and mandate protracted permitting timelines uncommon in traditional commercial real estate markets [S1][S27]. These factors concentrate expertise demand in this segment.

Proprietary property technology platforms and an established service ecosystem further differentiate Zoned versus typical CRE investors lacking specialized knowledge of local cannabis laws. However, competition intensifies as more market entrants — including independent investors, hedge funds targeting marijuana real estate plays, hard money lenders, or even licensed operators themselves — recognize opportunities in this fragmented sector [S27].

Capital access remains impaired by federal prohibition status; most banks refuse lending or impose onerous terms due to CSA classification of cannabis. Thus Zoned’s ability to scale organically or prudently capitalize acquisitions suffers vs generalist peers with broader collateral bases or more conventional clientele [S8]. This distinctive positioning pits high regulatory barriers against challenging financing environments.

Growth Opportunities Driven by Regulatory Tailwinds and Service Expansion

While growth remains constrained presently by cautious capital markets and political uncertainty around federal cannabis reform, gradual progressive legalization at state levels could expand demand significantly for specialized zoning-compliant real estate solutions.

Expansion of the advisory segment leveraging technology platforms promises ancillary revenue diversity beyond asset ownership returns. Additional states legalizing recreational cannabis or refining "green zoning" hubs could generate new leasing pipelines or consulting engagements.

Moreover, improvements upstream in banking reform or federal policy easing would unlock broader institutional capital participation—a material positive catalyzing property acquisition velocity and portfolio diversification.

However, no explicit guidance in recent filings forecasts accelerated growth absent execution of the MBO transaction which effectively signals winding down core public business operations for now [S1][S8].

Risks: Regulatory Flux, Tenant Concentration, and Capital Access

Key risks highlighted across recent filings revolve around intrinsic vulnerability to regulatory fluctuations impacting zoning approvals or tenant licenses[S1]. Complex permitting exposes investments to extended lead times or local policy reversals impeding leasing performance.

Tenant concentration risk is acute: most leases are tied to few licensed cannabis operators subject to compliance pitfalls or financial volatility under state laws. Any significant tenant default would severely impact rental income given lack of diversification.

Furthermore, funding uncertainty pervades as federal prohibitions restrict access to traditional mortgages or secured loans.

Governance risks also arise from the related-party nature of MBO parties who hold executive roles within the company potentially generating conflicts of interest during deal execution [S29].

Upcoming Milestones and What to Monitor Next

Critical event markers include:

- Stockholder vote on approving the MBO agreement required under Nevada law anticipated before mid-2026 deadlines [S6][S23].

- Financing contingency resolution by BPB Partners crucial to triggering closing scheduled for late 2026 with contractual allowance for certain timeline extensions contingent on deposit payments for select assets [S4][S25].

- Execution or lapse of tenant purchase options on three Arizona properties by April-June 2026 impacts portfolio composition immediately preceding transaction close [S1].

- Potential reverse merger or corporate restructuring post asset sale completion envisaged as public entity wind-down pathway [S4].

- Lease renegotiations potentially needed should operating assumptions shift after ownership transfers. These milestones will be primary demand-side indicators signaling transactional progress along with any updates regarding regulatory licensing or capital availability disclosures.

Current Financial Position and Capital Structure Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $2.5mm | |

| 2026-03-31 | ||

| Total debt | $7.7mm | |

| 2026-03-31 | ||

| Net debt | $5.2mm | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

A snapshot from the latest quarter ending March 31, 2026 reveals a constrained financial foundation:

| Metric | Value (USD) | As of |

|---|---|---|

| Cash & Equivalents | 2,500,758 | |

| 2026-03-31 (Q1) | ||

| Total Debt | 7,683,254 | |

| 2026-03-31 (Q1) | ||

| Net Debt | 5,182,496 | |

| 2026-03-31 (Q1) |

Overall liquidity remains tight without prospect of on-market equity raises given limited investor appetite for publicly traded entities in this complex niche industry segment under federal noncompliance constraints.[S8]

Disclaimer: This report is for informational purposes only; it does not constitute investment advice or recommendations. All data cited are sourced exclusively from public SEC filings dated through May 15, 2026 ([S1]–[S29], [F1]). Analysis herein reflects publicly available evidence without speculative forecasts beyond documented facts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments