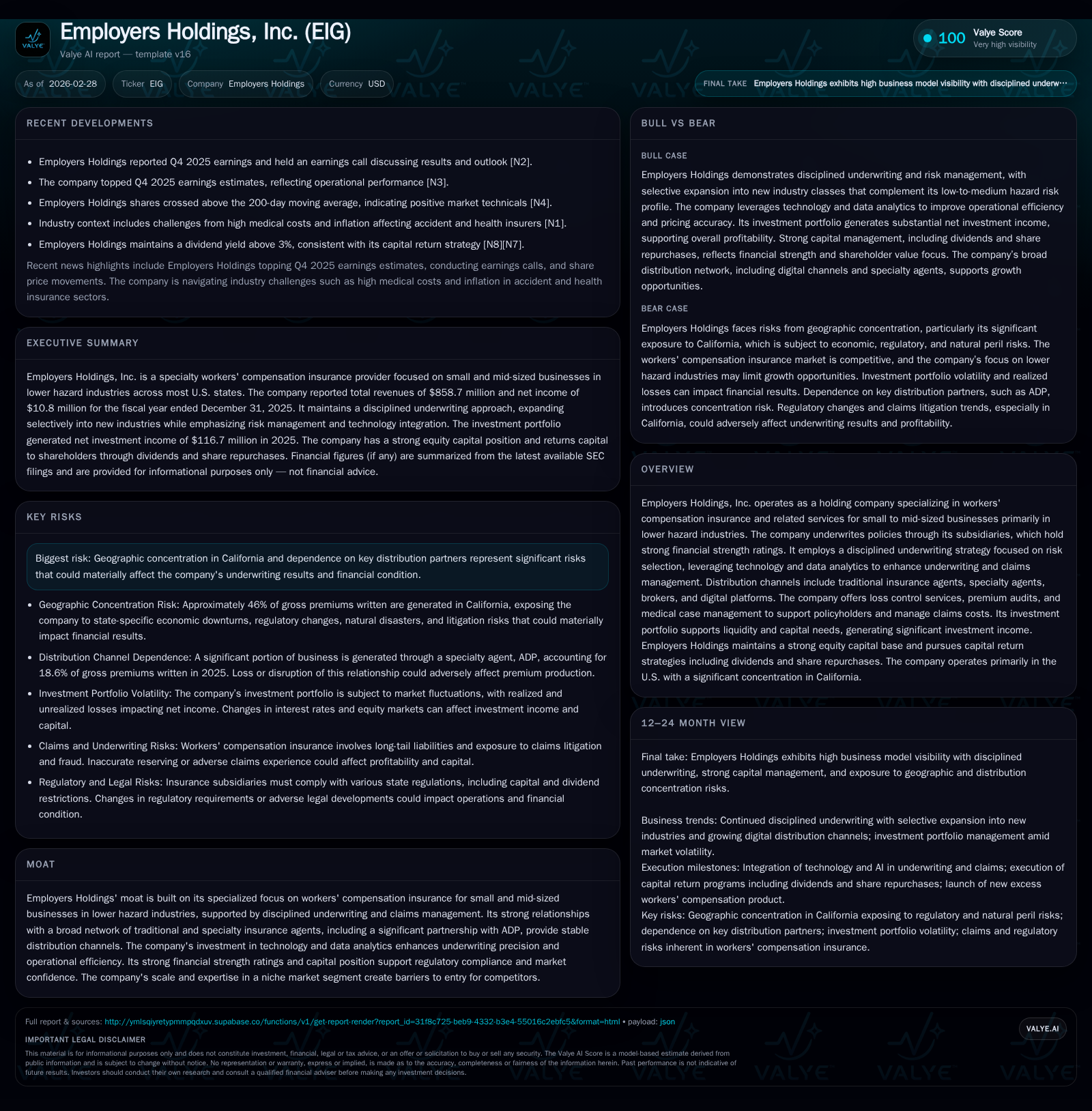

Employers Holdings: Earnings Volatility and Strategic Growth in Workers' Compensation Insurance

The firm demonstrates steady top-line performance despite significant net income contraction, driven by underwriting challenges and strategic capital management.

Employers Holdings, Inc. reported stable revenue near $859 million in 2025 but experienced a steep 91% drop in net income to $10.8 million amid underwriting loss pressures. The company maintains a disciplined underwriting focus on small to mid-sized businesses in lower hazard industries, leveraging traditional and specialty agent relationships, including a notable ADP partnership. A newly introduced excess workers' compensation product aims to diversify growth beyond core markets. Capital allocation remains active with sustained dividends and aggressive buybacks despite earnings volatility. Geographic concentration in California and distribution partner dependency continue to temper growth outlook and risk profile.

Financial Performance Review: From Stable Revenues to Earnings Downturn

Employers Holdings demonstrated resilience in its top-line performance for fiscal year 2025, posting revenue of approximately $858.7 million—a marginal decline of about 2.5% compared to the prior year’s $880.7 million [F1]. However, this relative stability belied significant profitability challenges as net income suffered a precipitous drop from $118.6 million in 2024 to only $10.8 million in 2025, translating into a nearly 91% decrease [F1] [N1] [N2]. This divergence between revenue steadiness and earnings collapse reflects deteriorating underwriting results amidst persistent loss pressures.

The company’s Management Discussion and Analysis (MD&A) highlights that combined ratio expansion was central to this earnings compression [S1]. Underwriting losses increased due predominantly to higher claims frequency and severity within certain industry segments underwritten by the company. While investment income remained robust—supported by elevated interest rates—the underwriting impairments overwhelmed overall profitability [S24]. Operating cash flow similarly contracted from $76.4 million in 2024 down to approximately $44.7 million in the latest period [F1], reflecting these operational strains.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 859 | 11 | 45 | 100000 | -2.5% | -90.9% |

| 2024 | 881 | 119 | 76 | 100000 | +3.5% | +0.4% |

| 2023 | 851 | 118 | 49 | 0 | +19.3% | +144.0% |

| 2022 | 714 | 48 | 100 | 100000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 30 | 183 | 45 |

| 2024 | 30 | 43 | 76 |

| 2023 | 30 | 76 | 49 |

| 2022 | 90 | 30 | 100 |

Source: SEC companyfacts cache [F1].

Table summarizes key annual financial metrics showing top-line consistency amidst earnings volatility.

Underwriting Discipline and Competitive Landscape Impacting Growth

Employers Holdings operates with a laser focus on a single insurance line: workers' compensation insurance tailored primarily to small and mid-sized enterprises within lower hazard classifications [S1] . This disciplined approach constitutes the backbone of its moat—a niche specialization allowing granular risk segmentation and conservative pricing.

The underwriting model employs data-driven risk selection emphasizing businesses predicted to yield loss ratios beneath industry averages by restricting coverage predominantly to the lower four of seven hazard groups [S21]. Such selectivity supports stability but constrains growth potential by limiting addressable markets.

Competition remains intense from multi-line insurers who leverage cross-selling benefits, often offering bundled policies which reduce Employers’ ability to compete solely on price [S1]. Moreover, reliance on agents and brokers introduces further dynamics; notable partnerships such as with Automatic Data Processing (ADP)—the largest payroll services provider—accounted for approximately 18.6% of premiums written in fiscal year 2025, underscoring both strategic opportunity and concentration risk [S8]. Dependency on such channel partners has intrinsic vulnerability since distribution is non-exclusive and competitors compete aggressively for agent allegiance.

Pricing pressures emerge amid these conditions as competitors with broader product suites can subsidize workers’ compensation offerings at compressed margins or losses to capture market share [S1]. Nonetheless, Employers seeks differentiation through service quality, technology-enabled ease of doing business, and claims management expertise, aiming for persistency over pure price competition.

Strategic Product Expansion and Emerging Market Opportunities

In February 2026, Employers launched an excess workers’ compensation product targeted at self-insured enterprises across several U.S jurisdictions, marking a deliberate push beyond traditional product boundaries concentrated mostly on primary coverage for smaller businesses [S1] [N1] .

This product introduction signals pursuit of diversification avenues within controlled risk parameters—potentially broadening fonts of premium growth while leveraging underwriting knowledge accrued over years.

However, given the entrenched geographic concentration—California alone contributed approximately 46% of gross premiums written during fiscal year 2025 [S20]—and limited industry vertical expansion so far, this initiative faces structural headwinds that may temper near-term material upside before scale is established.

Forecast Notes: What Investors Should Monitor Post-Q4 Results

Explicit forward-looking guidance has not been extensively provided; nonetheless, management commentary underscores priority areas warranting scrutiny: evolving combined ratio trajectory reflecting claims inflation or moderation; expenditure trends around technology enhancements aimed at claims adjudication efficiency; renewal retention rates tracking efficacy of customer engagement amid competitive pressures; and distribution partner dynamics especially involving ADP’s small business unit [N1] [N2].

Successful execution against these vectors is critical given the looming challenges embedded within the underwriting environment.

Capital Structure and Liquidity Management: Navigating Debt Covenants and Surplus

Employers Holdings maintains financial prudence evidenced by an unleveraged balance sheet with zero borrowings drawn under its $25 million revolving credit facility throughout calendar year ending December 31, 2025 [S4] [S5]. The company's subsidiaries hold strong AM Best "A" (Excellent) ratings reaffirmed recently enhancing borrowing capacity terms including reduced margins under its Credit Agreement refinancing arrangements [S6] [S19].

Liquidity reserves reside mainly within insurance subsidiaries holding statutory admitted assets surpassing immediate payout needs with total cash plus investments summing more than $2 billion systemwide at year-end [S7], enabling robust claims settlement capability.

Federal Home Loan Bank membership gives access to collateralized advances totaling approximately $35 million with favorable fixed rates maturing between late-2026 through mid-2029 aligning well with liability profiles providing strategic liquidity cushions beyond operating cash flows.

Dividend payments by subsidiaries remain constrained by state regulatory solvency requirements though aggregate ordinary dividend capacity approximates $77 million per annum distributable upstream after board approval mitigating holding company funding risks relative to operational needs including capital returns or acquisition activities [S6].

Shareholder Returns Profile: Dividends, Buybacks, and Return on Equity

Despite dramatic earnings contraction in fiscal year 2025 compounded by underwriting loss impacts, Employers Holdings preserved stable dividend payments totaling $29.9 million consistent with prior years demonstrating commitment to shareholder distributions reflective of long-term cash flow generation capabilities rather than transient profit swings [F1] [S14].

Contrastingly, stock repurchase activity accelerated markedly with $182.8 million expended during the year versus $42.6 million in prior year supported by healthy free cash flow approximated at $44.6 million (operating cash flow less capex) albeit lower than historical peaks reflecting cost control amidst cyclical pressures [F1] [S15].

Return on equity remains muted near approximately 1%, sharply reduced from double-digit levels seen previously due largely to current income compression although book equity declined moderately reflecting buybacks net of retained earnings replenishment effects [F1]. Such capital allocation signals a tactical decision privileging opportunistic share valuation support balancing sustainable dividend policy.

Risk Factors Spotlight: California Concentration and Distribution Dependency

Material risks center on heavy exposure to Californian market concentration where nearly half the premiums are generated exposing Employers Holdings to multiple localized vulnerabilities including adverse regulatory changes impacting claim costs or benefit structures; heightened litigious claim environments including cumulative trauma litigation trends; natural disaster susceptibility notably wildfire risks; and economic shifts affecting customer base viability tied disproportionately to tourism-dependent sectors within the state economy [S9] [S16].

Further operational risk arises from reliance on concentrated distribution cohorts—with ADP representing nearly one-fifth of gross premiums—which while affording scale also imposes counterparty concentration risk especially if strategic realignments occur or competitive disintermediation transpires.

Contemporaneously, digital distribution channels continue evolving but currently contribute just under ten percent of premiums supporting incremental diversification yet necessitating ongoing investment for competitive parity or advantage angles.[S8]

Conclusion

Employers Holdings embodies a specialized niche insurer contending with cyclically elevated underwriting challenges evidenced starkly in its recent earnings volatility juxtaposed against steady revenue streams sustained through longstanding agent partnerships bolstered by technology investments for credibility preservation.

The firm’s pivot into excess workers’ compensation products presents foundational groundwork for measured diversification though overshadowed in short term by geographic concentration risks primarily dictated by Californian exposures alongside considerable distributor dependency notably via ADP partnerships.

Capital stewardship exemplifies conservatism balancing shareholder returns via consistent dividends complemented by opportunistic buybacks fueled predominantly through sound operating cash flow generation underpinning liquidity buffers well aligned with regulatory mandates.

Close monitoring should emphasize combined ratio movement supporting earnings recovery trajectories alongside retention rates within competitive pricing landscapes potentially intensified by multi-line insurer incumbents leveraging economies-of-scale not accessible to single-line specialists such as Employers.

Continued deployment into digital platforms coupled with artificial intelligence-powered underwriting enhancements will be integral in securing incremental competitive differentiation essential for sustainable growth amid intensifying national industry competition.

Disclaimer: This analysis is provided solely for informational purposes without any explicit or implicit endorsement or recommendation regarding Employers Holdings securities or other investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments