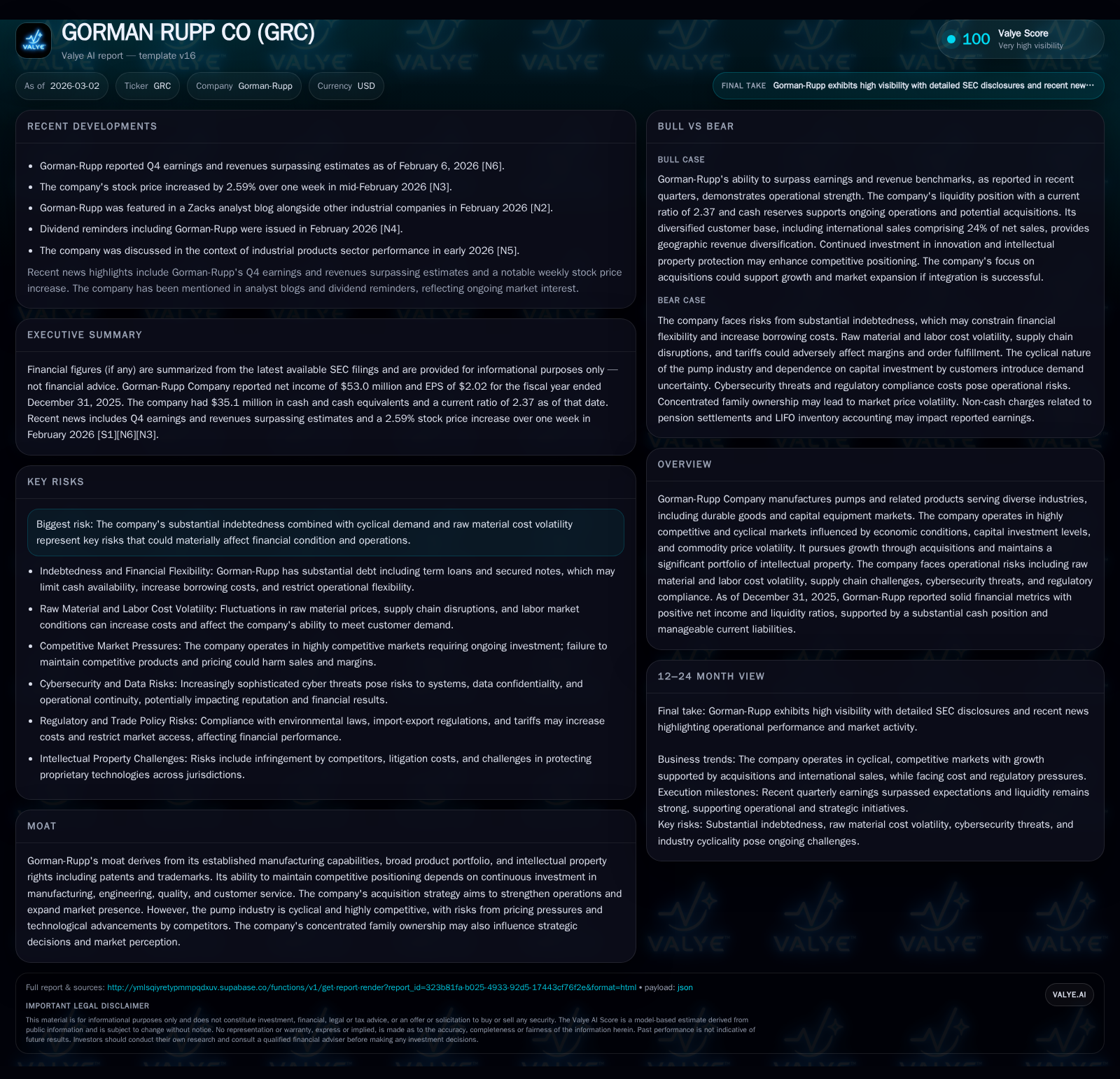

Gorman-Rupp’s Strategic Acquisitions and Operational Resilience Boost Profitability

The company's solid earnings growth, disciplined capital management, and acquisition-driven expansion underscore its competitive standing despite cyclical industry challenges.

Gorman-Rupp Company demonstrated robust financial performance in 2025, marked by a 4.3% increase in operating income to $95.4 million and a net income surge of 32.2% to $53 million [F1]. This was achieved despite largely flat revenues, reflecting operational efficiencies and effective margin management. The firm's strategy to fuel growth through targeted acquisitions adds complexity and leverage pressures but offers expanded market reach. Capital allocation remains conservative with strong free cash flow generation supporting dividends amid manageable debt levels. Key risks include raw material price volatility, regulatory compliance costs, and cybersecurity exposures. Monitoring top-line resilience and integration outcomes will be critical for sustaining progress.

Revenue and Profitability Trends Reflect End-to-End Operational Strength

Over the past several years, Gorman-Rupp Company has navigated a challenging cyclical industrial landscape characterized by relatively stable top-line figures but meaningful improvements along the profitability and cash flow lines. The revenue base stood at approximately $379 million in fiscal year (FY) 2017 and remained relatively flat into FY 2025 with just a minor contraction of about 0.7% year-over-year (YoY) compared to the immediate prior year [F1]. Despite this top-line stagnation, operating income exhibited resilience with a pronounced upward trend culminating in $95.4 million in FY 2025—a 4.3% increase YoY—illustrating robust margin enhancement initiatives.

Net income saw an even more notable ascent rising by roughly 32.2% YoY to $53 million during FY 2025 [F1], underscoring benefits derived from both operating efficiencies and favorable cost management amidst input price fluctuations. Cash flows from operations also expanded significantly by around 52% compared to the previous period reaching $106 million [F1]. Meanwhile, the company delivered capex compression of nearly 37% relative to earlier years—a tactical move supporting free cash flow conversion while restraining fixed asset growth [F1]. This capex discipline is salient given the capital-intensive nature typical of durable goods manufacturing where investments in production capacity can often pressure margins if not carefully managed.

With shareholders’ equity growing steadily from roughly $331 million in FY 2022 to about $415 million by FY 2025, an approximate return on equity (ROE) near 12.8% emerges [F1], reflecting consistent profit generation relative to invested capital underpinned by operational rigor.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 53 | 106 | 95 | +32.2% |

| 2024 | 40 | 70 | 91 | +14.8% |

| 2023 | 35 | 98 | 87 | +212.2% |

| 2022 | 11 | 14 | 40 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 12.8 |

| 2024 | 10.7 |

| 2023 | 10.0 |

| 2022 | 3.4 |

Source: SEC companyfacts cache [F1].

Table: Fiscal Year Performance Summary (2017–2025) based on company SEC filings [F1]

This financial trajectory signals that Gorman-Rupp has established an end-to-end operational platform capable of extracting incremental value beyond topline stagnation through lean manufacturing principles, supply chain optimization, and stringent overhead controls typical within capital equipment industries.

Acquisition Strategy Fuels Expansion but Adds Integration Risks

A pivotal component of Gorman-Rupp’s growth paradigm resides in its strategic acquisitions aimed at broadening product capabilities and expanding geographic reach [S1][S14]. The company explicitly acknowledges that its historical expansions have materially depended on acquiring complementary businesses domestically and internationally.

As of the latest disclosures, Gorman-Rupp maintains substantial leverage comprising a senior secured first-lien credit facility of $370 million as a term loan coupled with a revolving credit line totaling $100 million plus $30 million in senior secured notes carrying a fixed interest rate of approximately 6.40% [S4]. Such indebtedness underscores covenant risk exposure which can curtail flexibility amidst fluctuating economic conditions or unexpected operational setbacks.

Acquisition integration inherently carries risks including management distraction from core operations, potential attrition of key personnel or customers within acquired entities, valuation missteps impacting earnings accretion prospects, assumption of unforeseen liabilities, and the challenge of building cross-functional synergies across disparate organizational cultures.

While the acquisition approach is expected to augment market presence and sustain innovation pipelines in a competitive pump manufacturing sector characterized by commoditization pressures, these benefits must be balanced against the elevated financial commitments inherent in such transactions.

Growth Drivers and Industry Headwinds in Pump Manufacturing

Gorman-Rupp operates within markets tightly coupled to durable goods demand cycles as well as capital investment rhythms across sectors such as municipal water infrastructure, oil & gas exploration supporting commodity extraction activities, agriculture irrigation systems, and construction equipment OEMs [S5][S7].

Volatility in commodity prices profoundly affects end-user capex decisions; for example sustained downturns in oil prices can delay large-scale pump orders tied to energy infrastructure projects resulting in revenue lulls.

Moreover, ongoing tariffs imposed by the U.S. administration on various raw materials coupled with reciprocal foreign trade barriers can inflate input costs or disrupt supply chains necessitating proactive pricing strategies that risk dampening customer demand if passed through excessively.

Currency exchange rate fluctuations present another layer of complexity — with notable exposures across the Eurozone currencies (Euro), Canadian Dollar (CAD), British Pound (GBP), and South African Rand (ZAR) [S5], necessitating prudent hedging frameworks or flexible sourcing models.

Competitive dynamics remain fierce as peers innovate rapidly leveraging digital controls or alternative materials threatening traditional pump designs; thus continuous R&D investment is critical for maintaining technological parity or leadership .

Capital Allocation Highlights: Dividends, Debt, and Cash Flow Management

Gorman-Rupp demonstrates conservative capital allocation priorities emphasizing liquidity preservation along with consistent dividend payouts as part of shareholder returns without engaging recently in share repurchase programs [S19][F1]. The cash position stood at approximately $35 million against current liabilities near $98.6 million giving comfort via a healthy current ratio around 2.37x which signals effective working capital management for an industrial manufacturer with inventory-intense operations [F1].

Robust operational cash flows recorded at $106 million far outpace ongoing capex expenditures (~$13 million estimated based on historical trends), producing strong free cash flow nearing $93 million supporting debt servicing needs while maintaining discretionary flexibility for acquisition funding or dividend continuity [F1][S19].

The absence of recent buybacks suggests cautiousness potentially related to leverage considerations or prioritization of organic growth investments amid cyclical uncertainty.

Intellectual Property as a Competitive Moat in a Volatile Market

One differentiating aspect central to Gorman-Rupp’s competitive stance is its extensive intellectual property (IP) portfolio encompassing patents, trademarks, copyrights alongside internally-developed proprietary knowledge governing pump design and manufacturing processes [S1].

In an industry where product homogeneity is common and pricing pressure severe, IP protection serves not only as a barrier against direct replication but also underpins premium feature differentiation demanded by institutional customers.

However, challenges persist including enforcement variability across jurisdictions causing potential exposure to IP infringement disputes either as plaintiff or defendant; costly litigation risks and mandated redesigns could impact profit margins substantially if not promptly managed [S14].

Maintaining sufficient R&D investment levels is essential not only for product evolution but also for reinforcing IP strength against competitor technologies adapting quickly within digitally-enabled pump controls or energy-efficient designs.

Risk Factors: Indebtedness, Raw Material Volatility, and Regulatory Compliance

The company faces material risks concomitant with its sizable debt load which may restrict strategic agility should operating performance deteriorate or financial covenant thresholds tighten unexpectedly during recessions or supply chain disruptions [S4].

Raw material price swings—steel alloys along with other metals—are notably volatile influenced by global demand-supply imbalances exacerbated recently by geopolitical tensions heightening tariff regimes thereby pressuring cost structures further [S5][S7][S13]. Passing increased costs onto customers is constrained due to highly competitive markets intensifying margin squeeze risk.

Environmental regulations impose ongoing compliance costs encompassing emissions control mandates at production sites plus waste disposal requirements which may escalate operational expenses periodically requiring both capital upgrades and higher recurring outlays potentially reducing cash available for discretionary uses [S8].

Cybersecurity vulnerabilities loom large given increasing sophistication of hacking attempts targeting corporate networks that manage proprietary engineering data or customer information; breaches could cause reputational harm alongside direct financial damage stemming from intellectual property theft or production downtime exposures [S15].

Outlook: Metrics to Watch Amid Economic Cyclicality

Despite no explicit forward guidance disclosed recently [N1], monitoring several key indicators will illuminate how Gorman-Rupp navigates cyclical headwinds:

- Stability or uptick in revenue reflecting sustainable demand amid shifting capex patterns of end consumers.

- Leverage ratio trajectories post-acquisition activity which will reflect balance sheet flexibility

- Margins growth retention amidst input cost volatility signaling operational execution quality

- Effective ramp-up of R&D initiatives validating long-term IP competitiveness

- Integration success markers from newly acquired businesses manifesting through incremental earnings contributions.

In sum, Gorman-Rupp’s sturdy earnings progression combined with careful capital deployment provides grounds for cautious optimism if cyclical swings do not intensify abruptly while mitigating identified risk factors remains paramount.

This analysis is intended solely for informational purposes regarding The Gorman-Rupp Company’s financial condition and industry context based on publicly available filings as of early March 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments