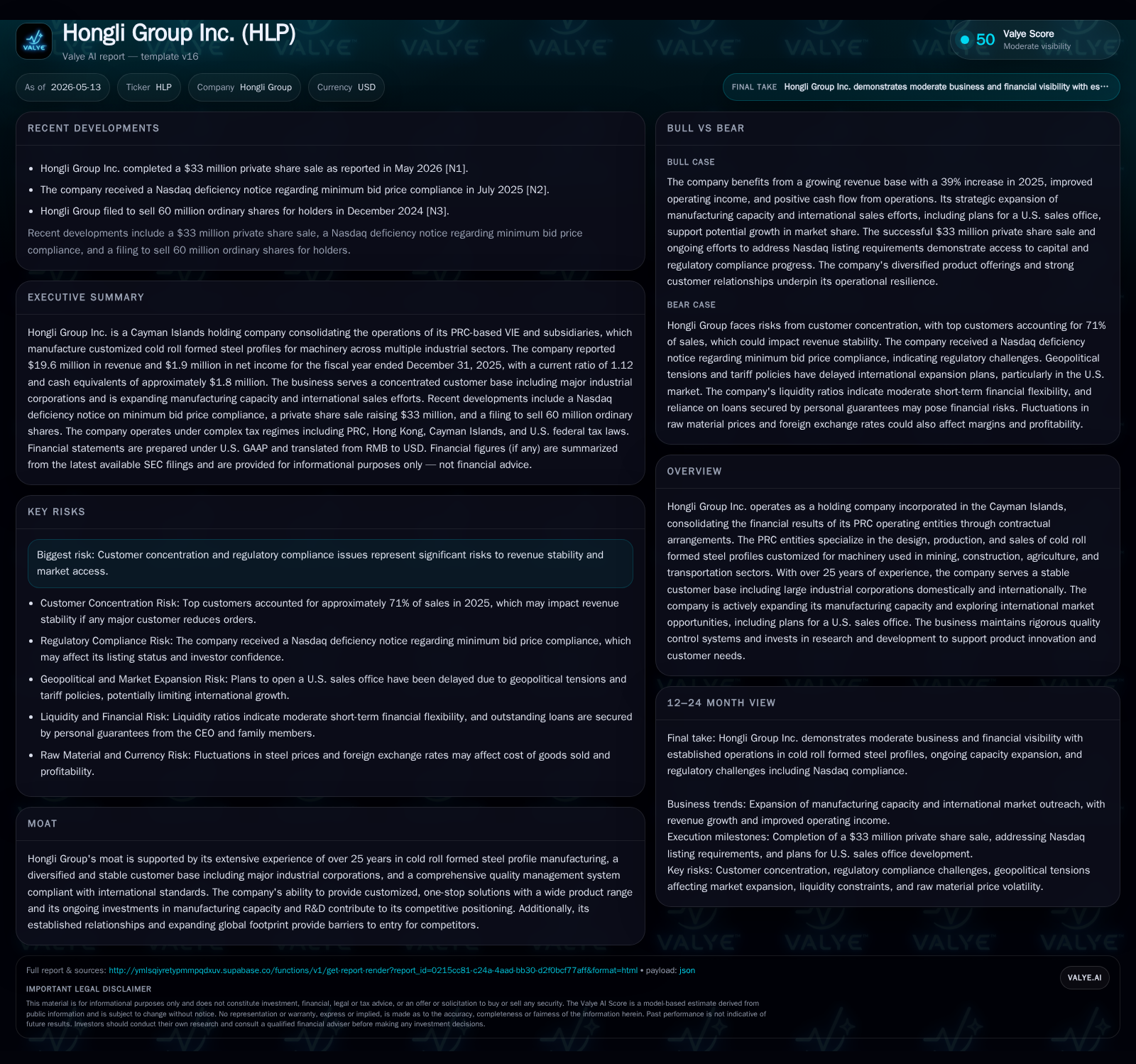

Hongli Group Expands Capacity and Global Reach with Latest Equity Raise

Recent capital infusion and manufacturing capacity expansion signal Hongli Group’s strategic shift toward scaling amid evolving market demand.

Hongli Group recently closed a private placement raising $325,000 through issuance of 1.3 million shares, reinforcing its balance sheet to pursue critical manufacturing capacity expansions. The company reported 39% revenue growth in 2025 driven by increased orders mainly from the PRC domestic market and international customers, despite steel price volatility. Hongli’s business model centers on producing custom cold roll formed steel profiles primarily serving mining, construction, agriculture, and transportation sectors, with over 25 years of customer relationships underpinning its competitive moat. Capacity saturation in existing facilities necessitates new investments to support top-line growth and R&D-led product innovation, while regulatory risks linked to its contractual VIE structure and customer concentration remain watchpoints.

Recent Capital Raise and Operational Update

Hongli Group Inc. completed a pivotal private placement in April 2026, issuing 1.3 million ordinary shares at $0.25 per share and raising gross proceeds of $325,000 [S3]. This injection arrives concurrently with the Company's fiscal year-end financial results announcement in May 2026 [S2], signaling clear intent to support manufacturing scale expansion initiatives.

The latest quarter confirmed that Hongli's existing manufacturing facilities have reached full capacity saturation [S1], constraining the company's ability to fulfill the increasing demand from core industrial sectors such as mining and construction machinery. The equity raise directly addresses these capacity bottlenecks by providing incremental capital essential for purchasing additional facilities, expanding factory footprints, and hiring more employees—critical steps before revenue volume growth can accelerate further [S1].

Business Model and Product Customization Strength

Hongli Group operates through an offshore holding company domiciled in the Cayman Islands that consolidates the financials of its mainland China VIE entities via contractual agreements rather than direct equity ownership [S1]. The PRC operating subsidiaries specialize exclusively in designing, producing, deep-processing, and selling cold roll formed steel profiles customized for machinery targeting mining excavation, construction equipment, agricultural implements, and transportation industries.

Leveraging over a quarter-century of industry expertise, Hongli offers a comprehensive range of products tailored precisely to customer machinery designs. This high degree of customization builds significant switching costs among an established clientele that includes Weichai LOVOL Heavy Industry Co., SUNGJIN TECH CO., XCMG Group, and clients associated with Katsushiro Machinery in Japan [S1]. Such embedded customer trust fosters durable pricing power even amidst input cost fluctuations.

Revenue mechanics rely heavily on volume increases secured through repeat business from loyal clients with an average relationship span exceeding ten years [S20]. Pricing flexibility hinges notably on steel raw material costs—over half of production expenses—but mitigating practices like volume buying and forward inventory purchasing smooth margin volatility [S18].

Competitive Positioning and Industry Dynamics

The competitive landscape is shaped by Hongli’s proven track record balancing advanced quality controls compliant with international standards against commodity-driven cost pressures inherent in steel manufacturing [S1]. Its moat stems from:

- Extensive operational history establishing trusted long-term contracts,

- A broad yet specialized product portfolio that addresses multifaceted industrial applications,

- Ongoing R&D investments fostering technological improvements critical for performance differentiation,

- Strategic geographic presence spanning China’s heavy industry hubs plus initial footprint extensions into South Korea, Japan, and the U.S. [S1][S9].

Nonetheless, industry structural risks persist around raw material price unpredictability affecting gross margins directly [S1]. Furthermore, Hongli’s corporate structure introduces legal uncertainty due to reliance on PRC Contractual Arrangements governing the VIE—the enforceability of which remains subject to evolving Chinese regulatory scrutiny [S1][S13]. Such factors impose potential barriers or cost impacts relative to competitors better aligned with local ownership models.

Capacity Expansion as a Growth Catalyst

According to management commentary within the latest filings, the current production lines are fully booked, necessitating urgent capital deployment into facility acquisitions and workforce augmentation to unlock incremental output capacity [S1]. This scale increase is vital not only for meeting order backlogs but also for enabling further R&D undertakings aimed at developing new or improved steel profile products demanded by evolving machinery specifications.

Geographic diversification efforts include plans for a dedicated sales office staffed by local personnel in Wisconsin intended to better penetrate the U.S. industrial market—a move delayed but still seen as strategic for capturing international demand beyond Asia [S9,S14]. Expanding physical presence coupled with production capability scaling enhances Hongli’s value proposition as a reliable global supplier across multiple sectors.

Operating leverage is expected to improve as fixed costs are amortized over larger production volumes while R&D enhancements should confer longer-term competitive advantages allowing premium pricing amidst commoditized inputs [S22].

Risks Around Customer Concentration and Regulatory Environment

Hongli derives approximately 70% of revenues from a tight group of major clients including LOVOL (35%) and XCMG (23%) among others; although these relationships are longstanding averaging over ten years each [S19,S20], such concentration creates vulnerability if any key customer reduces order volumes due to macroeconomic or strategic shifts.

On the legal front, the VIE structure under which Hongli operates lacks direct equity control over its main Chinese business entities—it consolidates them via Contractual Arrangements recognized under PRC law but subject to interpretation risks that could undermine enforceability or prompt governmental intervention impacting operational continuity or shareholder value negatively [S1][S13].

Additionally, fluctuation in steel prices can erode gross margins if increases are not effectively passed onto customers in time or if procurement hedges fail amid sudden market swings [S18]. Inflationary pressures on labor and overhead further contribute to cost risk without guaranteed offsetting revenue increases.

Key Near-Term Milestones to Monitor

Investors should closely monitor multiple execution points:

- Progress updates regarding acquisition or expansion of manufacturing facilities responding to current saturation,

- Implementation timeline and effectiveness of the planned U.S. sales office launch and subsequent order flow,

- Order book developments particularly from key long-term customers reflecting sector demand dynamics,

- Regulatory clarifications or government policies concerning VIE structures affecting Hongli’s consolidations,

- R&D outcomes leading to product innovation translating into new market wins or margin improvement.

These indicators will be crucial markers validating whether Hongli can successfully leverage newly raised capital into tangible growth beyond its current production ceilings.

Latest Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1811149 | |

| 2025-12-31 | ||

| Current assets | $16mm | |

| 2025-12-31 | ||

| Current liabilities | $14mm | |

| 2025-12-31 | ||

| Current ratio | 1.12x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) |

|---|---|

| Revenue | 19,600,691 |

| Operating Income | 2,433,285 |

| Net Income | 1,942,840 |

| Cash & Equivalents | 1,811,149 |

| Total Debt | 3,548,284 |

| Current Ratio | 1.12 |

As of fiscal year-end December 31, 2025, Hongli's revenue totaled approximately $19.6 million representing robust growth (+39%) compared with prior year levels [F1][S5]. Gross margin modestly expanded from prior periods reaching ~32.5%, supported by procurement efficiencies mitigating volatility in steel prices [S18]. Operating income stood at about $2.4 million with net income near $1.9 million illustrating improving operational leverage despite elevated sales-related expenses aligned with expansion strategies [F1][S22]. The company held cash reserves just above $1.8 million against total debt estimated near $3.5 million based on prior data points indicating manageable leverage supported by positive net working capital reflected through a current ratio above one (1.12) [F1][S11]. These financial fundamentals provide balance-sheet stability for approaching scale investments.

This analysis is based exclusively on publicly filed SEC reports as of May 13, 2026 ([S1], [S2], [S3]) combined with companyfacts financial data ([F1]) and relevant news disclosures ([N1]). It does not represent investment advice or recommendations but aims at a thorough understanding of Hongli Group Inc.'s recent operational evolution within its competitive setting.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments