Vertical Integration and Market Expansion Define AiXin Life’s Emerging Franchise

AiXin Life International advances its health and wellness business in China through vertical integration, omni-channel distribution, and targeted acquisitions but faces serious liquidity and operational risks.

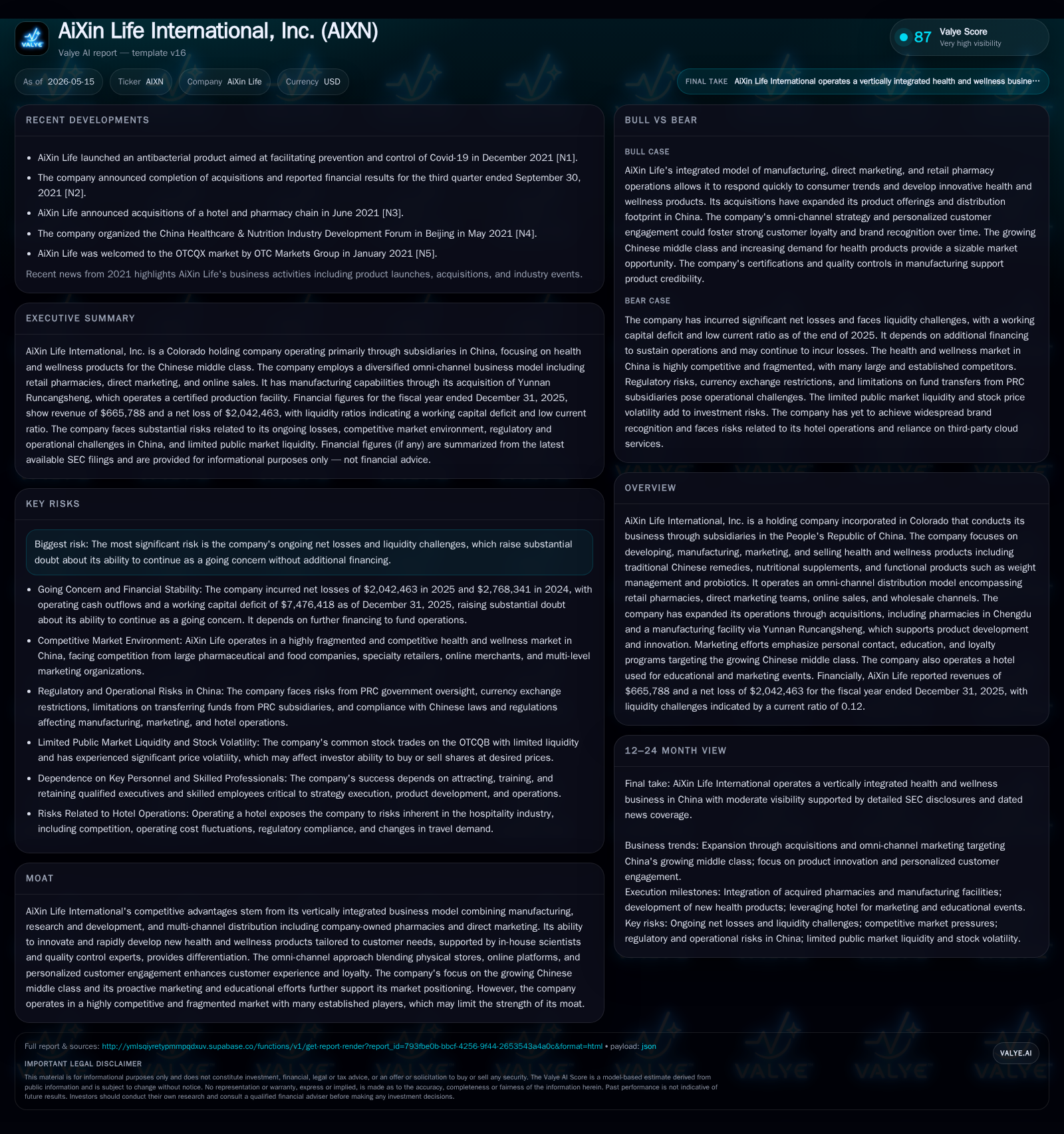

AiXin Life International recently disclosed ongoing operational challenges characterized by continued net losses and a severe working capital deficit raising doubts about its viability without additional financing. The company operates a vertically integrated health and wellness platform in China, combining proprietary manufacturing, R&D, company-owned pharmacies, direct marketing events, and online sales to target the growing middle class. While recent acquisitions bolster its production capacity and retail footprint, intense market competition and regulatory complexities constrain growth. Watchpoints include successful integration of acquisitions, execution on omni-channel expansion, and securing sustainable funding to support operations.

Latest Operational Disclosures: The November 2025 Quarterly Filing Highlights

In the latest 10-Q filing dated November 19, 2025 [S2], AiXin Life International reiterated existing risk factors reflecting ongoing financial strain. The company reported operating losses surpassing $2 million annually for the preceding years ending December 31, 2025 [F1], underscoring persistent difficulties in achieving cash flow breakeven. Cash levels dwindled to approximately $20,751 at year-end 2025 from over $62,000 a year prior while operating cash outflows exceeded $2 million during the same period [F1]. Most troubling is the current ratio measured at a critical 0.12 indicating that short-term liabilities dwarf liquid assets by an order of magnitude [F1]. These metrics collectively raise substantial doubt about the company’s ability to continue as a going concern absent immediate access to additional financing.

Director certifications appearing in the same quarterly filing indicate standard corporate governance compliance though no detailed operational improvements or explicit liquidity plans were delineated here. Subsequent event disclosures in an April 2026 8-K filing [S3] provide incremental background including leadership profile updates but do not materially alter the financial outlook delivered in late 2025.

As context, AiXin’s annual report filed May 15, 2026 [S1] offers a broader narrative on its strategy blending manufacturing acquisition integration with expanded retail pharmacy presence and digital sales channels aiming for scalability.

Comprehensive Business Model: Product Quality and Distribution Channels

AiXin Life International operates principally through its PRC subsidiaries focusing on health and wellness products marketed mainly to China’s rising middle class [S1][S21]. The business model integrates several related functions. On the supply side, acquisition of Yunnan Runcangsheng provides a nearly 3,000 square meter manufacturing complex fully equipped for traditional Chinese medicine (TCM) processing compliant with national GMP standards including ISO quality certification [S1]. This facility supports rapid product innovation with dedicated R&D teams of scientists, formulators, nutritionists, and quality control specialists enabling development of functional nutraceuticals such as weight management formulas and probiotics tailored to urban lifestyle diseases like hypertension or obesity.

Sales are executed via an omni-channel distribution approach encompassing wholesale shipments, company-owned pharmacies (eight locations concentrated in Chengdu following acquisition of nine outlets in September 2021), direct multi-level marketing events featuring entertainment-style consumer education programs led by field representatives, as well as e-commerce platforms [S1]. The pharmacies double as learning centers where staff educate customers on product benefits via personal contact supporting customer loyalty.

This vertical integration from ingredient planting to end consumer affords control over product quality consistency and supply chain agility enhancing differentiation compared to distributors reliant purely on third-party products. The varied sales touchpoints also spread customer acquisition risks while enabling cross-channel promotions such as order pickup at physical stores following online purchases.

China’s Health and Wellness Industry: Competitive Dynamics and Regulatory Considerations

The Chinese health supplement market is large but fragmented with entrenched competition from multiple fronts including multinational pharmaceutical giants heavily advertising legacy brands alongside fast-moving local players leveraging digital marketing muscle [S1][S4]. Increasing smartphone penetration enables real-time price comparison which compresses margins particularly for commoditized categories. To maintain relevance requires consistent innovation backed by credible scientific evidence combined with brand-building investment—a challenge for AiXin given limited operating history since launching its health division in late 2017 via acquisition [S1][S24].

From a regulatory perspective, AiXin faces complex PRC requirements covering product safety certifications, advertising claims controls prohibiting unsubstantiated health benefits assertions, environmental compliance impacting raw material sourcing/manufacturing emissions, employee social insurance mandates varying across regions, plus evolving cybersecurity laws governing consumer data collected online or through loyalty programs [S4][S5][S7][S16]. Compliance missteps could incur fines or disrupt operations. While litigation risk has recently diminished following closure of a legacy case involving one pharmacy purchased pre-acquisition with indemnification arrangements secured from former ownership [S4][S6], broader legal uncertainties persist due to limited precedents within China's still-maturing judicial frameworks.

Growth Catalysts: Innovation, Acquisition Strategy, and Omni-Channel Expansion

Strategic growth hinges on continuing product pipeline development backed by proprietary R&D housed at Yunnan Runcangsheng enabling rapid formulation cycles for emerging consumer trends in functional health products aimed at lifestyle ailments typical among urban middle-class Chinese consumers [S1]. The facility also supports scale production of tablets, capsules, granules ensuring supply continuity.

Acquisitions form a central pillar of expansion extending retail distribution reach through controlling pharmacies directly involved in omnichannel retail/education activities; these provide not only revenue streams but also marketing hubs where frontline staff can enhance customer engagement through personalized coaching programs tailored to wellness outcomes [S3]. Online channels have gained traction complementing physical presence through subscription models allowing recurring revenues supported by cross-promotions incentivizing store pick-up or home delivery illustrating effective channel synergies.

Moreover regulatory compliance costs are likely set to increase amid tightening PRC laws around social insurance payments for employees (with regional enforcement variability) plus stringent environmental/safety regulations impacting manufacturing cost base potentially squeezing profitability further if scale effects lag expectations [S5][S7][S16].

Governance concerns stem from heavy reliance on CEO Quanzhong Lin who splits attention among multiple enterprises including entities sometimes adjudged competitive; additionally his ongoing need to clear legal uncertainties linked to allegations of illegal fundraising—recently reported as orally cleared though without official documentation—introduces leadership continuity risk which could disrupt execution if unresolved forcing possible resignation scenarios [S25][S26].

Upcoming Milestones and Watchpoints for Execution Progress

Critical near-term monitoring points include any formal disclosures regarding updated revenue or profitability guidance post fiscal year-end filings that might signal stabilization or acceleration of growth efforts [S2][S3]. Additionally key will be clarity around financing plans addressing liquidity shortages either through debt restructuring or equity capital raises designed to extend runway enabling organic growth pursuits.

Operationally success integrating acquired pharmacies into seamless omni-channel retail operations will be evident through data such as unit openings/closures count changes plus metrics capturing customer retention rates derived from learning-center initiatives. Progress expanding online subscription memberships vis-à-vis established sales benchmarks would also confirm strengthening digital adoption supporting recurring revenue stability.

Product innovation momentum can be gauged via launch announcements backed by patent filings associated with proprietary formulations developed at Yunnan Runcangsheng or pipeline indicators communicated during investor updates highlighting new remedy categories targeting chronic conditions prevalent among target customers.

Governance developments concerning CEO Lin’s legal status documentation remain closely watched given their significance for investor confidence toward stable executive leadership crucial for sustained turnaround efforts.[S3][S25]

Financial Snapshot: Understanding the Current Balance Sheet and Profitability

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $20,751 | |

| 2025-12-31 | ||

| Total debt | $85,799 | |

| 2025-12-31 | ||

| Net debt | $65,048 | |

| 2025-12-31 | ||

| Current assets | 1,016,123 | |

| 2025-12-31 | ||

| Current liabilities | 8,492,541 | |

| 2025-12-31 | ||

| Current ratio | 0.12x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Period End |

|---|---|---|

| Revenue | 665,788 | |

| 2025-12-31 | ||

| Operating Income | -2,520,550 | |

| 2025-12-31 | ||

| Net Income | -2,042,463 | |

| 2025-12-31 | ||

| Cash & Equivalents | 20,751 | |

| 2025-12-31 | ||

| Total Debt | 85,799 | |

| 2025-12-31 | ||

| Current Ratio | 0.12 | |

| 2025-12-31 |

The snapshot underscores AiXin Life's difficult financial footing at fiscal year-end December 2025 evidenced by modest revenue generation under $700k overshadowed by considerable operating losses exceeding $2.5 million yielding negative net income over $2 million despite inventory assets suggesting some scale. Extremely low cash levels limit agility while high total debt magnifies refinancing risk compounded by an alarming current ratio signaling severe working capital deficits that jeopardize solvency without corrective measures.[F1]

Disclaimer: This analysis is based solely on publicly filed SEC documents up to May 15, 2026. No investment recommendations are offered or implied.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments