Quantum Leap Acquisition Faces Liquidity and Execution Challenges Post-IPO

The latest quarterly filing exposes tight liquidity and operating losses as Quantum Leap Acquisition navigates the pre-merger runway typical for SPACs.

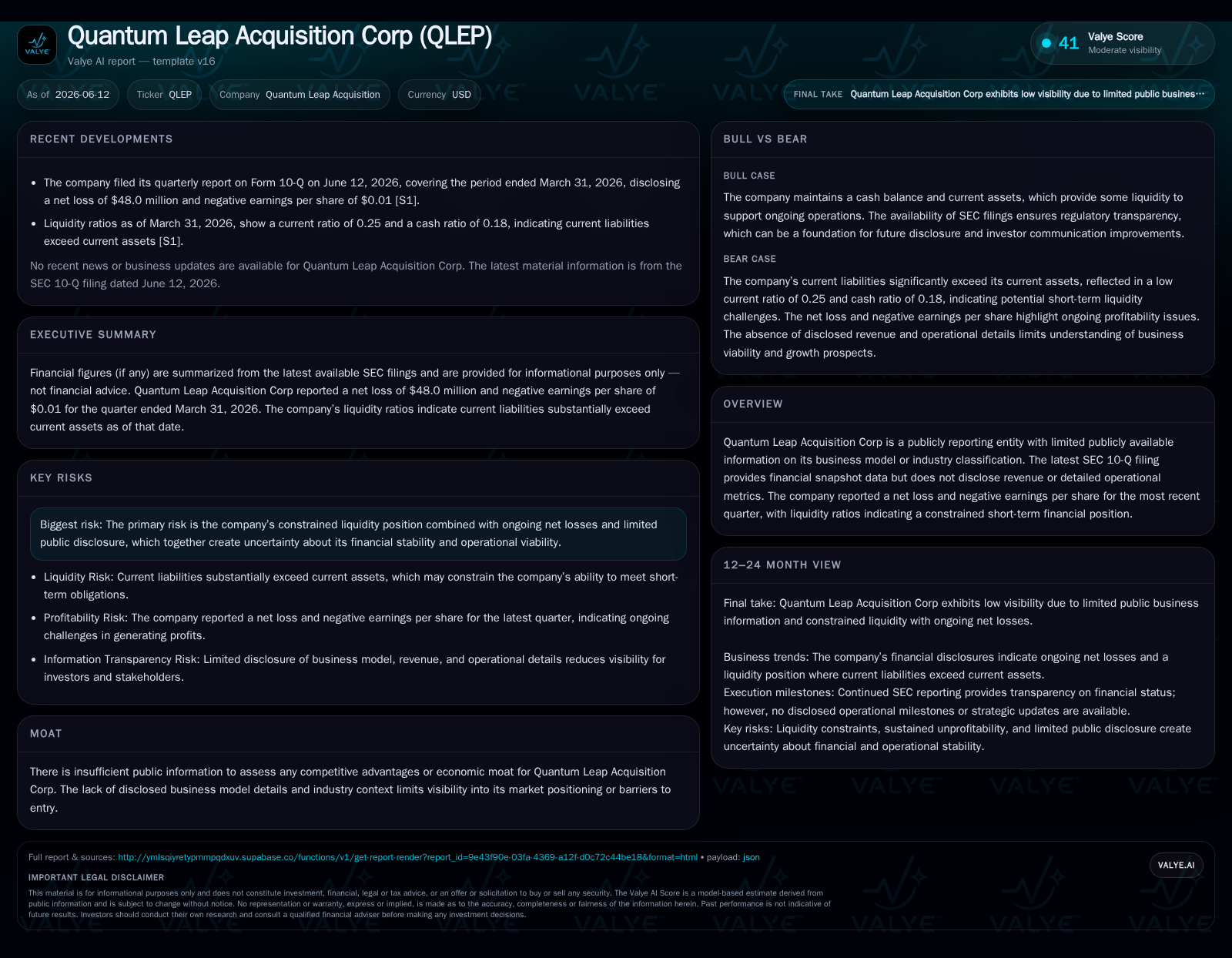

Quantum Leap Acquisition Corp’s (QLEP) June 2026 10-Q reveals a constrained liquidity position with a current ratio of 0.25 and a net loss typical for a recently IPOed Special Purpose Acquisition Company (SPAC). The company raised approximately $211 million through its IPO, private placement, and partial over-allotment, held in a trust account while seeking an acquisition target. The firm faces standard SPAC challenges including managing operating expenses pre-merger, sponsor promote dilution risks, shareholder redemption rights, and the ticking clock of the mandated business combination deadline within about two years of IPO. These factors frame the near-term viability and execution risks for QLEP as it pursues a de-SPAC transaction amid broad industry pressures.

Latest Quarterly Update: Liquidity and Operational Status Post-IPO

Quantum Leap Acquisition Corp reported its latest SEC quarterly filing on June 12, 2026 [S2]. The disclosure reflects typical early-stage SPAC financial dynamics: no revenues or operating income but consistent net losses incurred to cover offering and corporate administrative expenses. For the quarter ended March 31, 2026, QLEP posted a net loss of $48,012 with current assets totaling approximately $126,910 against current liabilities near $499,831 [F1], resulting in an acute current ratio around 0.25. This signifies very limited short-term liquidity relative to obligations.

The May 18 event filing [S3] confirms that QLEP successfully closed its initial public offering on May 4, 2026, issuing 20 million units priced at $10 each and raising gross proceeds of about $200 million. The underwriters partially exercised their over-allotment option shortly thereafter for an additional nearly one million units generating another $9.17 million. Alongside a private placement raising about $5.95 million from the sponsor entity Paddington Partners 88 LLC [S13], total gross funds raised exceeded $211 million. These proceeds are held in a U.S.-based trust account managed by Continental Stock Transfer & Trust Company acting as trustee [S14]. Withdrawal from this trust is restricted until successful completion of a qualifying business combination or liquidation/redemption events.

This trust funding structure is fundamental to SPAC models — safeguarding investor capital while seeking an acquisition target but also establishing operational runway constraints given ongoing overhead costs borne outside the trust account.

Understanding Quantum Leap Acquisition’s SPAC Business Model and Mechanics

Quantum Leap Acquisition functions solely as an acquisition vehicle without intrinsic operating activities or revenue streams pre-merger. It raises capital by selling Units consisting of one Class A ordinary share plus one redeemable warrant exercisable into an additional share [S3]. The IPO price was set at $10 per unit, consistent with industry norms.

Funds raised are deposited into the trust account which secures investor capital until the firm completes a merger (business combination) or liquidates if no deal is consummated within approximately 18 months post-IPO (the mandated timeframe).

Sponsor incentives are crafted through the "sponsor promote" mechanism whereby the sponsoring shareholders receive founder shares typically convertible into approximately 20% equity post-merger contingent on deal success [S3]. Sponsors also have working capital loans made convertible into equity if elected. This arrangement facilitates alignment but sets up potential dilution risks for public shareholders if warrants are exercised or loans convert.

Redemption rights enable public shareholders to redeem their ordinary shares at pro rata trust account value prior to merger approval or deal completion. High redemption rates can materially reduce available cash to fund acquisitions and complicate deal execution.

In essence, Quantum Leap must identify and close an attractive target transaction within its limited timeline while managing operational burn outside the trust account and navigating shareholder redemption dynamics.

Industry Backdrop: Positioning Within the SPAC Market Structure and Peer Norms

Compared to peers that have also completed IPOs recently in similar size brackets (~$200 million), Quantum Leap aligns with standard capital structuring — including partial over-allotment exercise reflecting moderate underwriter demand [S14]. However, its early liquidity metrics reveal notable strain vis-à-vis typical sector benchmarks where stronger short-term liquidity cushions support both operational flexibility and negotiation power during acquisition discussions.

SPACs across markets routinely face pressure from delays or inability to consummate business combinations within regulatory timeframes leading to forced liquidations or value-destroying redemptions [S5]. Sponsor promote dilution ratios often range up to about 20%, placing emphasis on sponsors’ ability to deliver accretive deals that justify equity dilution.

Warrant exercise behavior also critically influences capitalization structures post-business combination; presently QLEP holds standard redeemable warrants exercisable for Class A shares with terms established at IPO close [S3]. Absent explicit redemption rate data this cycle for QLEP substantiates caution given broader market trends showing elevated redemption activity diminishing merger fund pools.

Key Growth Drivers Supporting Successful Business Combination Execution

Growth prospects for Quantum Leap predominantly hinge on its ability to leverage structural tailwinds favoring SPACs as alternative routes for private companies’ public listings.

Regulatory support for de-SPAC transactions has stabilized compared to prior years’ uncertainty enhancing transaction feasibility combined with tweaks in sponsor incentive frameworks aligning interests more explicitly around deal success.

Expertise brought by Quantum Leap’s sponsors evidenced by their willingness to commit working capital loans convertible into equity suggests readiness to underwrite transaction costs thereby reducing liquidity drain on public funds pre-merger.

Market appetite among institutional and retail investors continues skewing toward speculative growth vehicles in volatile macroeconomic conditions providing tuning opportunities for PIPE financing instruments once QLEP announces definitive merger targets.

Milestones that may indicate forward momentum include secured merger agreements subject to shareholder votes, timing extensions requested prudently within regulatory thresholds, PIPE financing commitments signaling valuation endorsement by strategic investors; all potentially strengthening QLEP’s path toward closing viable business combinations.

Risks and Caveats: Liquidity Constraints, Dilution, Redemption Risk, and Timelines

Material risks disclosed directly spotlight QLEP’s constrained capacity reflected by subpar liquidity—current ratio of roughly 0.25 as of March quarter-end—highlighting vulnerability should costs escalate or merger progress stall [F1][S2]. Operating expenses although moderate require vigilant control given absence of revenue generation pre-acquisition.

Failure to consummate an initial business combination within roughly an eighteen-month window could trigger mandatory liquidation processes returning limited proceeds after administrative cost deductions thereby eroding shareholder value [S5]. Closely tied is the redemption risk where large-scale shareholder exits reduce merger funding making transactions challenging or unattractive.

Dilution considerations emerge through sponsor promote framework granting sponsors sizable equity stakes post-transaction completion plus warrant conversions incurring further share count inflation adversely impacting post-merger earnings per share potential [S3].

Market volatility especially noticeable across recent periods impacts trading prices for units and thus investor sentiment influencing exercise rates on warrants or decisions on redemptions creating cyclic uncertainty around capital structure stability.

Lastly potential conflicts between sponsors aiming for deal closures that preserve their promote economics versus public shareholders demanding accretive outcomes adds governance complexity requiring transparent communication from management teams overseeing these arrangements.

What to Watch Next: Milestones Measuring De-SPAC Progress And Investor Signals

Investors following Quantum Leap Acquisition should monitor several key event-driven developments indicating progression toward de-SPAC execution:

- Public announcement of definitive merger agreements specifying target companies alongside transaction valuations.

- Filing updates regarding PIPE investment rounds which supplement trust account funds in conjunction with completed deals.

- Scheduling notices for shareholder votes that legitimize mergers provide clarity on timing horizons.

- Trends in warrant exercises versus redemption submissions revealed in proxy materials revealing investor confidence levels.

- Updated balance sheet disclosures tracking cash balances net operating spend shedding light on available runway.

- Notifications regarding requests for extension approvals beyond initial SPAC lifespan marking either negotiation complexities or strategizing phases.

- Any shifts in regulatory landscape affecting compliance costs or procedural hurdles impacting QUANTUM LEAP’s opportunity set.

Together these indicators will define whether QLEP can overcome structural challenges typical for newly minted SPACs maneuvering complex market conditions toward successful public listing facilitation for private companies.

This analysis synthesizes latest publicly available SEC filings and industry context relevant as of June 12, 2026. It refrains from speculative forecasts or unsupported conclusions regarding specific merger targets or timings.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments