Hi-Great Group Holding Advances Nutritional Supplements and Family Weekend Farm Amid Liquidity Pressures

Latest quarterly filing confirms continued development of supplement sales and agritourism resort as company navigates funding and market challenges.

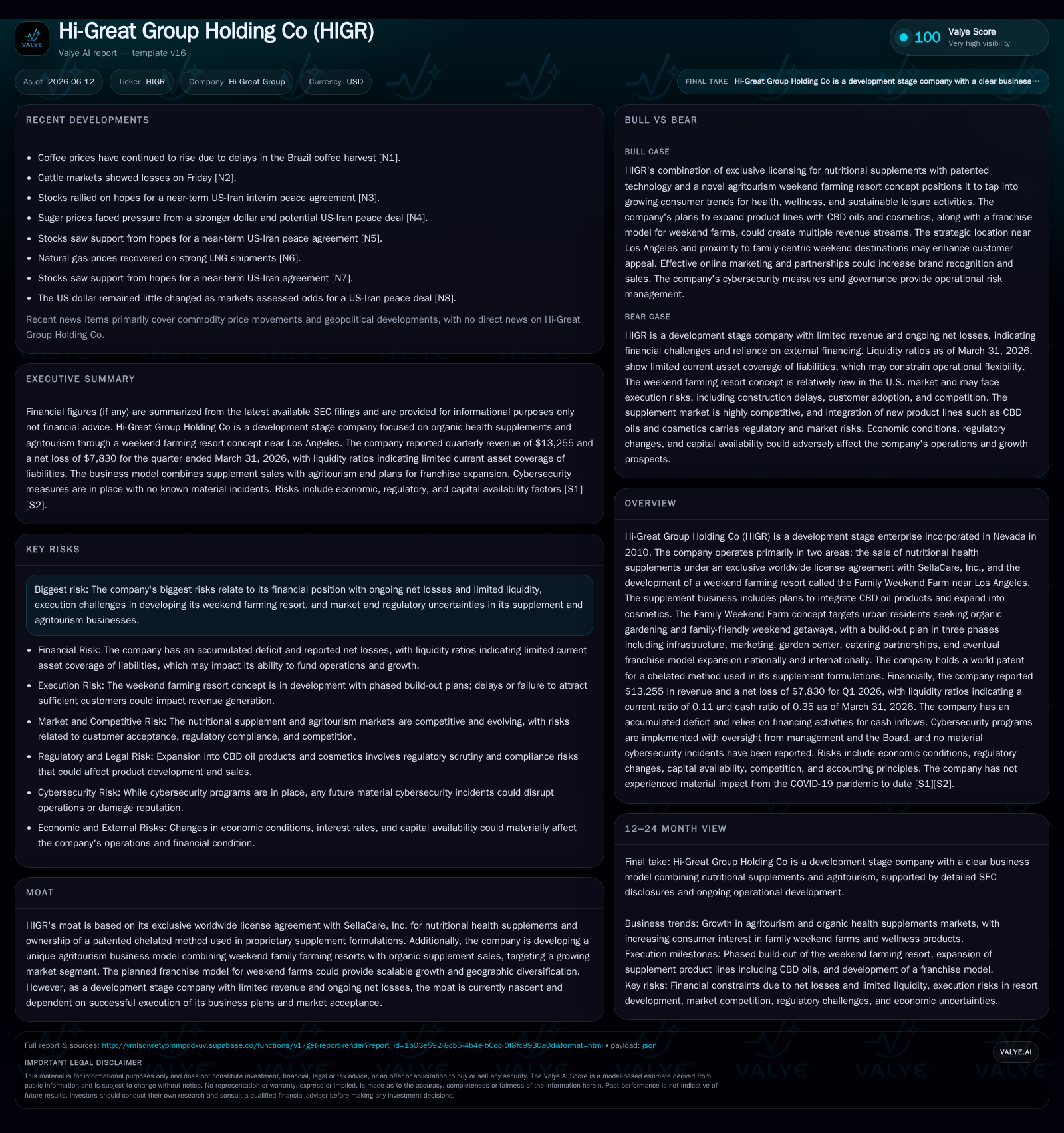

Hi-Great Group Holding Co (HIGR) remains a development stage company focusing on direct-to-consumer nutritional supplements under an exclusive license and building out a novel weekend farming resort targeting urban families. Its latest 10-Q filing shows ongoing operational losses and liquidity constraints, underscoring the importance of successful execution of its supplement branding refresh and phased resort build-out. The company leverages a world-patented chelated mineral method for product differentiation while developing a scalable franchise model in agritourism. However, limited revenue traction, competitive pressure in supplements, and capital intensity in resort development present substantial growth risks.

Recent Operating Update

Hi-Great Group Holding Co filed its latest quarterly report on June 12, 2026 [S2], confirming it continues to operate as a development stage enterprise without material COVID-19 impacts reported so far. Despite this stability, the company's liquidity position remains strained: it reported current assets of approximately $22,105 against current liabilities of $194,621 as of March 31, 2026 [F1], resulting in a critically low current ratio near 0.11. This highlights ongoing funding challenges during efforts to develop its dual business segments.

Business Model Overview

HIGR's business rests primarily on two coordinated pillars:

Nutritional Health Supplements: Through an exclusive worldwide licensing agreement with SellaCare, Inc., HIGR markets nutritional supplements built around a patented method involving chelated minerals (patent #5128139). These supplements focus on alkalization, amino acids, advanced minerals, and whole rice concentrates aimed at health-conscious consumers seeking longevity benefits. The products are sold predominantly via direct-to-consumer online platforms.

Family Weekend Farm Agritourism: HIGR is simultaneously developing an innovative “weekend farming resort” near Los Angeles targeting urban families seeking organic gardening experiences coupled with safe, family-oriented recreational getaways. This concept includes leasing gardening parcels equipped with portable cottages constructed from reclaimed materials with optional solar panels to reduce carbon footprint. The resort is planned as a three-phase build-out including infrastructure setup (clubhouse/restrooms/marketing), expansion with garden centers and catering partnerships, culminating in scalable franchising across the U.S. and internationally.

This dual approach enables HIGR to foster potential cross-selling opportunities—leveraging organic herbs grown on its farms for supplement production reduces sourcing costs while promoting brand synergy between wellness products and experiential agritourism.

Industry Structure and Competitive Position

HIGR operates at the intersection of two vibrant but distinct sectors: nutritional supplements (including planned CBD oil integration) and agritourism-focused experiential travel.

In nutritional supplements—a crowded market where strong brands like Herbalife Nutrition establish direct sales dominance—HIGR's exclusive rights to proprietary chelated mineral formulations offer valuable differentiation but require significant marketing investment to break through consumer awareness barriers [S1]. The renewed focus on revamping its retail website aims to improve internet traffic and customer retention metrics essential for sustainable growth

The agritourism sector is rapidly growing internationally yet remains early-stage in U.S. weekend family farming concepts where operators are few. HIGR’s proximity to major urban centers like Los Angeles positions it well geographically; however, scaling a resort-based model involves high fixed costs related to land acquisition/improvement, operational staffing, entertainment partnerships, accommodation facilities, and marketing to capture a niche audience seeking organic lifestyles.

Furthermore, franchise modeling introduces complexity around maintaining consistent service quality while enabling rapid geographic expansion.

Growth Drivers

Several structural drivers underpin potential long-term growth:

- An increasing global consumer preference for plant-based health products alongside rising demand for CBD-infused supplements could enlarge HIGR’s addressable market if product expansions succeed.

- Expansion of e-commerce digital marketing effectiveness may significantly drive online supplement sales volume if website enhancements and brand updates gain traction.

- Urban families’ growing interest in organic farming experiences fuels demand for weekend farms offering safe recreational environments conveniently located near cities.

- Developing franchise units nationally would provide geographical diversification while generating recurring fees.

- Patent-protected formulations enable better positioning against commoditized products.

- Cross-channel customer engagement strategies leveraging both agritourism guests and supplement consumers can boost retention.

KPIs such as online traffic growth rates to the new retail site, conversion rates into paying customers for supplements, membership sales for farm parcels, resort occupancy rates beginning after phase one completion, along with franchisee onboarding velocity will be critical markers of momentum.

Risks and Growth Constraints

The company’s nascent stage nature coupled with financial fragility pose significant risks:

spending cycles and evolving consumer preferences toward experiential organic lifestyles.

- Intellectual property enforcement challenges could dilute competitive advantage if key patents are contested or circumvented.

- Scaling via franchising adds operational complexity; failure to maintain consistent brand experience may impair reputation before geographic diversification benefits accrue.

What To Watch Next

Key milestones reflecting future progress include:

- Launch completion timing for the redesigned supplement retail website incorporating updated branding elements—crucial for improving online customer acquisition efficiency [S1].

- Early membership subscription volumes for Family Weekend Farm parcels following phase one infrastructure readiness expected; tracking booking rates will indicate market acceptance [S12][S16].

- Development announcements around forming entertainment partnerships or catering agreements that enhance guest experience at the farm resort [S16].

- Updates on pilot sales or roll-out timelines for new CBD-infused products or cosmetic lines leveraging the existing herbal ingredient supply chain.

- Capital raising activities supporting operations beyond current liquidity status will serve as a leading indicator of sustainability given ongoing net loss trends [S1].

- Disclosure of initial franchise agreements secured or markets targeted beyond California suggesting geographical expansion plans occur.

Financial Profile Summary

As of the end of fiscal year 2025: revenues were approximately $36,958 following contraction from prior year figures while cost of sales fell correspondingly [F1][S1]. Operating expenses showed mixed trends with reduced professional fees offset by higher general administrative spend attributed to increased operational activities. Net losses nearly doubled to $87,208 highlighting operating leverage challenges at very low scale.

Liquidity remains critically strained; current assets stood at $22,105 versus liabilities at nearly $194,621 as of March 31, 2026, creating a current ratio near 0.11 [F1]. Its latest disclosures affirm continued developmental investments amidst sharp financial constraints characteristic of early-stage ventures attempting complex go-to-market expansions across two distinct verticals concurrently.

Successful execution hinges on revitalizing their online direct-to-consumer health product channel while advancing multi-year phased physical resort build-outs positioned strategically near large urban population centers craving organic lifestyle experiences. Concurrently navigating significant liquidity pressures increases execution risk but underscores potential scalability through franchise models if initial phases gain traction.

Investors should monitor evolving brand adoption trends in both business lines alongside upcoming capital raises that alleviate immediate funding gaps critical for sustaining growth initiatives amidst high competitive intensity within nutritional supplements and experiential agritourism sectors.

Disclaimer: This analysis is informational only based on publicly filed documents as referenced; it does not constitute investment advice or research views.

Financial position in context

Current assets of $22,105 and current liabilities of $194,621 imply a current ratio near 0.11x for 2026-03-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments