INNEOVA Holdings Faces Nasdaq Pricing Compliance Challenge While Leveraging Diversified Spare Parts and Engineering Services Platforms

The company's latest filings reveal operational resilience amid market headwinds and intensifying compliance scrutiny.

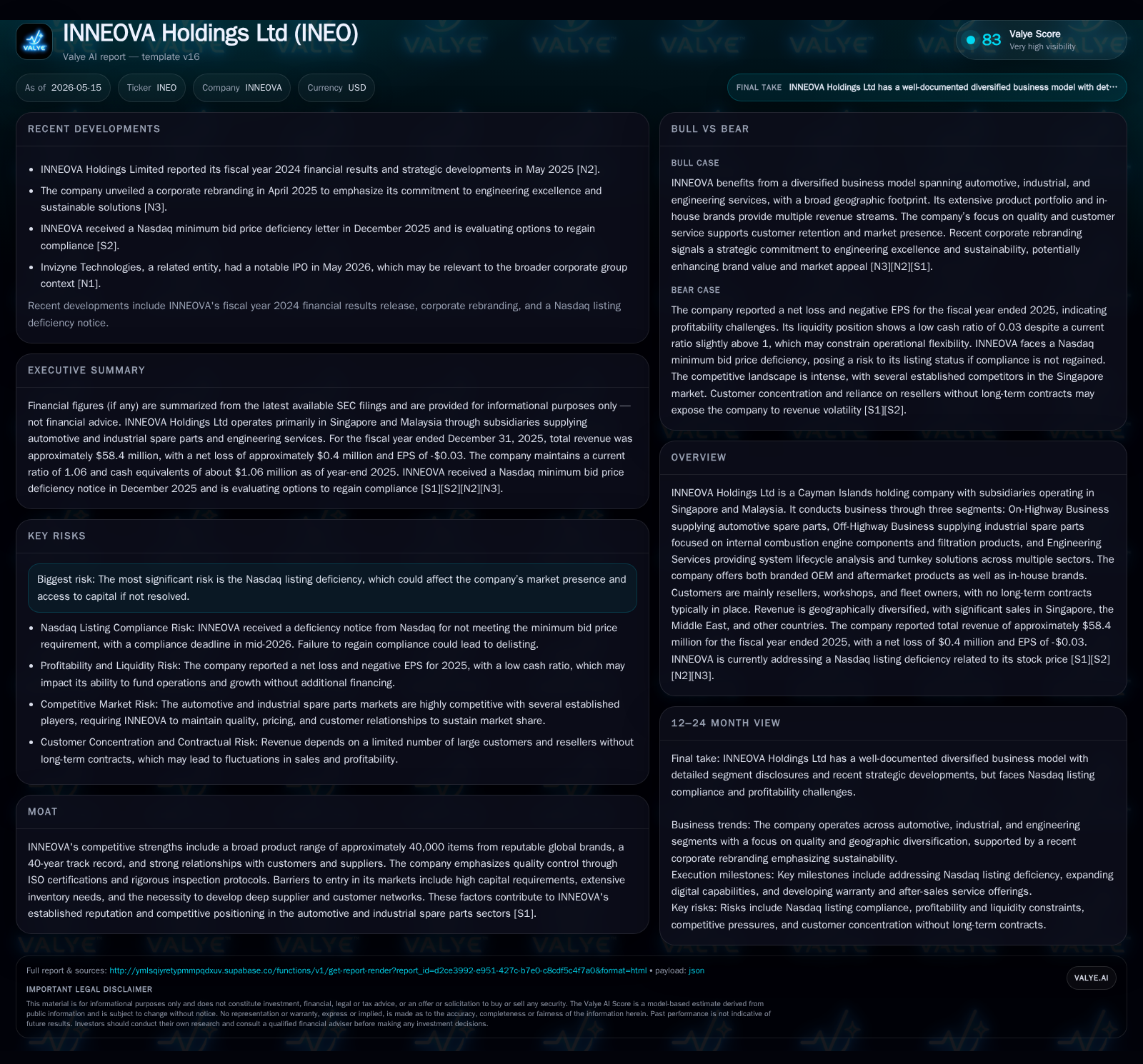

INNEOVA Holdings Ltd, a multi-segment automotive and industrial aftermarket supplier with a 40-year history, reported a modest decline in revenue and a shift to a small net loss in fiscal 2025. The company’s recent Nasdaq minimum bid price deficiency notice underscores increasing pressures on equity valuation despite steady operating cash flow. INNEOVA’s broad product portfolio, strategic expansion into engineering services, and geographic diversification underpin its competitive moat, although customer concentration and pricing pressures remain watchpoints. Going forward, the firm aims to regain Nasdaq compliance while developing digital commerce capabilities and after-sales service offerings to fuel growth.

Recent Operating Update

INNEOVA Holdings Ltd received a Nasdaq minimum bid price deficiency notice in December 2025 due to its share price falling below the $1 threshold over an extended period [S2]. The company has been given until June 8, 2026, to regain compliance or face delisting risks. This development represents a material near-term catalyst affecting investor sentiment and equity market presence.

Despite this compliance challenge, INNEOVA reported fiscal year 2025 revenues of approximately $58.4 million—a decline from $62.7 million in the prior year—and a net loss of $0.4 million compared with $8 thousand net income in fiscal 2024 [F1][S1]. Operating income swung negative by about $51 thousand, reflecting margin pressures across its segments. However, operating cash flow improved significantly to about $4.44 million as working capital management benefited from lower receivables and inventories coupled with active payables management [F1][S10]. Liquidity remains tight but manageable with a current ratio of 1.06; total debt stands near $1.24 million against cash of ~$1.06 million [F1].

The company is actively evaluating strategic responses to the Nasdaq deficiency including potential reverse stock splits but underscored the uncertainty inherent in regaining compliance within the available window [S2].

Business Model

INNEOVA functions as a Cayman Islands holding company overseeing three distinct yet complementary operating subsidiaries based primarily in Singapore and Malaysia [S1][S23]. It generates revenue through three core segments:

- On-Highway Business: Supplying OEM and aftermarket spare parts for passenger and commercial vehicles through retail outlets (Autozone (S)) and distribution networks primarily in Singapore and Malaysia.

- Off-Highway Business: Delivering industrial spare parts focused on internal combustion engine components such as filtration products to sectors including marine, energy, mining, agriculture, construction, and oil & gas.

- Engineering Services: A newer segment providing system lifecycle analysis and turnkey solutions spanning transport infrastructure, healthcare equipment maintenance, defense systems, utilities management, and facilities operations.

Revenue streams stem from product sales to resellers (distributors/dealers), workshops, fleet operators, shipyards, and end users without reliance on long-term contracts [S20][S22]. The broad catalog of approximately 40,000 SKUs includes branded OEM components sourced globally alongside proprietary in-house brands like REV-1 which undergo rigorous quality inspections backed by ISO certifications [S15]. Quality control comprises multiple inspection stages at receipt from manufacturers through final packing to ensure defect-free delivery.

Pricing is subject to competitive market conditions where the company faces vigorous price competition yet benefits from high barriers to entry including substantial upfront capital for inventory stocking demands and the necessity for cultivating deep supplier/customer networks over decades [S1][S20]. Customers value INNEOVA's ability to offer both wide choice and reliable availability with responsive service support sustaining loyalty absent firm contracts.

Industry Structure & Competitive Position

The On-Highway automotive parts market is highly fragmented yet dominated by companies capable of sustained OEM relationships combined with aftermarket offerings [S1]. INNEOVA's four-decade track record enhances credibility among distributors and fleet owners seeking dependable sourcing solutions focusing on quality assurance.

The Off-Highway sector serving energy-intensive industries such as mining or oil & gas is less crowded but requires specialized technical knowledge around combustion engine filtration technologies critical for industrial uptime [S1]. The company's extension into engineering services through the acquisition of INNEOVA Engineering Pte Ltd expands its footprint into higher-margin system integration projects supporting sustainable infrastructure maintenance [S11][S20].

Competitively, INNEOVA's geographic diversification—with heavy sales concentrations in Singapore (46%), the Middle East (5%), and other countries (~49%)—dampens localized economic shocks [S18][S28]. However, significant customer concentration risk persists with the top five clients generating over one-fifth of total revenues annually; the largest single customer contributed roughly 7% in FY25 highlighting dependency vulnerabilities [S9][S24].

Strategic partnerships with logistics firms like Lalamove enhance last-mile distribution efficiencies aiming to outpace rivals' service levels while ongoing digital investments aim to transition from traditional brick-and-mortar sales toward integrated e-commerce platforms facilitating real-time order processing [S20][S22].

Growth Drivers

Digital Transformation Initiatives

INNEOVA is actively digitizing operations with plans for a 24/7 online platform enabling customers to verify product availability instantly and place orders directly—an increasingly essential capability given evolving customer expectations for convenience and rapid turnaround [S20]. Integration with warehouse management systems coupled with last-mile delivery alliances promises gains in inventory velocity and fulfillment precision.

Service Line Expansion

Recognizing industry trends toward warranty-backed maintenance solutions over pure product sales, INNEOVA is developing after-sales service capabilities including repair and overhaul services that complement existing parts supply [S20]. While still nascent without formal contracts signed yet these moves could unlock sticky recurring revenues enhancing lifetime customer value.

Geographic & Product Diversification

While Asia Pacific remains core, partnerships aimed at expanding within Southeast Asia plus selective penetration into Middle Eastern markets provide avenues for volume growth mitigated by operational complexity [S20][S22]. Product breadth expansion via collaboration agreements enables offerings tailored across multiple industrial uses—from automotive replacement parts to heavy-duty machinery filters—allowing client cross-selling synergies.

Cash Flow Strength Supporting Investment Capacity

Improved operating cash flow generation (+66% YoY) despite slight top-line shrinkage provides solid internal capital for selective capex focused mainly on technology upgrades versus large-scale physical expansion which minimizes dilution risks [F1]. This positions INNEOVA well to steward funding needed both for navigating current market uncertainties as well as pursuing growth initiatives.

Risks & Watchpoints

Nasdaq Listing Compliance Risk

The imminent deadline to remedy share price deficiency introduces strategic pressure that may drive dilution or restructuring decisions impacting shareholder base perception and company valuation continuity [S2]. Failure poses existential risk regarding exchange delisting consequences.

Customer Concentration & Price Sensitivity

Heavy reliance on few major customers exposes revenue streams to demand swings or contract renegotiation especially amid inflationary cost pressures forcing price optimization battles along supply chains reducing margins potentially [S9][S17].

Supply Chain & Inventory Financing Constraints

Prepayment mandates imposed by suppliers limit working capital flexibility exacerbating liquidity stress under adverse market conditions particularly as inventory represents over 80% of cost of revenues impacting gross margin stability if raw material prices rise unexpectedly [S1].

Operational Dependence on Key Executives & Personnel Availability

Loss or departure of top executives (CEO Chin Heng Neo et al.) could disrupt strategic execution given their extensive industry experience pivotal since inception more than two decades ago combined with challenges recruiting comparably skilled talent in core regional markets Singapore/Malaysia adds execution risk [S12].

Product Liability Exposure & Regulatory Compliance Costs

Though product safety risks are mitigated through stringent quality controls restricted insurance coverage outside proprietary brands carries residual liability risks potentially incurring costly claims or harming brand reputation impacting customer retention long term [S12][S15].

Macro-Economic Cyclicality Affecting End Markets

Demand throughout marine energy mining agriculture sectors served by Off-Highway unit fluctuates alongside global commodity cycles sensitive to geopolitical tensions recession hazards while On-Highway passenger/commercial vehicle part replacement volumes depend on vehicle usage intensity impacted by consumer spending power trends particularly within Asia-Pacific recovering from varied financial instabilities recently reported [S17][N1].

What To Watch Next

Key milestones include:

- Progress updates regarding Nasdaq compliance efforts including announcements around potential stock consolidations or other remedial actions before June 8 deadline;

- Execution success on digital platform rollout evidenced by customer adoption rates or order volumes transitioning online;

- Development traction within new warranty/after-sales service segment capabilities whether formal contracts/contracts follow;

- Customer concentration trends such as retention or losses among top clients impacting backlog visibility;

- Changes in working capital dynamics especially inventory financing terms affecting liquidity cushions;

- Regulatory or litigation developments pertaining to product safety issues if any emerge;

- Sectoral economic indicators signaling recovery/slackening across targeted industrial verticals influencing order books.

Financial Profile Summary (FY ended December 31)

Historical performance (annual)

|

| FY | Net ($) | CFO ($mm) | OpInc ($) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -397000 | 4 | -51000 | 10000 | -5062.5% |

| 2024 | 8000 | 3 | 784000 | 774000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 4 | -8.0 |

| 2024 | 2 | 0.1 |

Source: SEC companyfacts cache [F1]. 2025 | | Operating Income | -51 | 2025 | | Net Income | -397 | 2025 | | Operating Cash Flow | 4,441 | 2025 | | Capital Expenditures | 10 | 2025 | | Equity | 4,973 | 2025 | | Total Debt | 1,241 | 2025 | | Cash & Equivalents | 1,059 | 2025 | | Current Ratio | 1.06 | 2025 |

Despite slipping into a small net loss in FY25 after consistent profitability prior years endured macro challenges most notably intense price competition plus supply chain disruptions impacting margins slightly. Robust operating cash flow facilitates debt servicing while conservative capex signals fiscal discipline supporting operational sustainability amidst market challenges [F1].

Disclaimer

This analysis is for informational purposes only based on publicly available data provided as of May 15th, 2026. It does not constitute investment advice or recommendations regarding buying or selling securities of INNEOVA Holdings Ltd or any other entity.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments