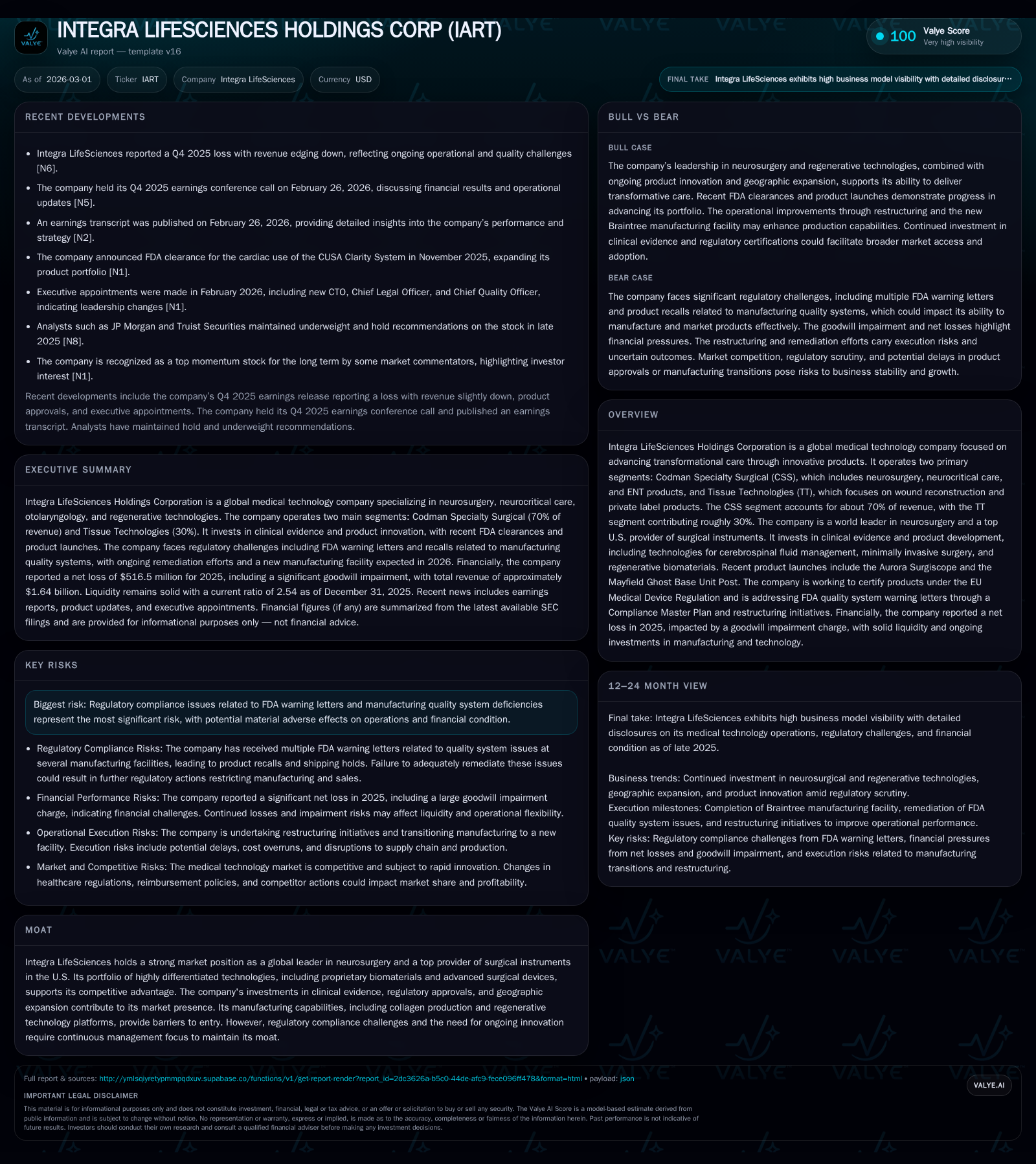

Integra LifeSciences' Transformation: Innovations and Fiscal Setbacks Reveal Growth Challenges

A detailed examination of Integra LifeSciences’ recent financial setbacks alongside its ongoing neurosurgical innovations and regulatory navigation.

Integra LifeSciences, a dominant force in neurosurgery with a leading Codman Specialty Surgical segment, showcased modest revenue growth yet faced substantial operating losses in fiscal 2025. Despite launching advanced products such as the Aurora Surgiscope and advancing clinical evidence through registries, the company grappled with FDA warning letters and manufacturing compliance hurdles which challenged its operational performance. Liquidity remains adequate with covenant relief in place, but increasing leverage and curtailed share repurchases highlight cautious capital allocation. Monitoring regulatory progress, registry outcomes, and geographic expansions will be key to understanding Integra’s near-term trajectory.

Revenue Evolution and Segment Drivers: What Shifted?

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -516 | 50 | -493 | 81 | -7337.7% |

| 2024 | -7 | 129 | 28 | 104 | -110.3% |

| 2023 | 68 | 140 | 112 | 67 | -62.5% |

| 2022 | 181 | 264 | 239 | 42 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -31 | -49.5 |

| 2024 | 52 | 25 | -0.4 |

| 2023 | 275 | 73 | 4.3 |

| 2022 | 125 | 222 | 10.0 |

Source: SEC companyfacts cache [F1].

Integra LifeSciences' revenue exhibited moderate growth, reaching approximately $1.635 billion in fiscal year 2025, marking a year-over-year increase from roughly $1.61 billion in 2024 [F1]. The company’s revenue mix is dominated by its Codman Specialty Surgical (CSS) segment, which contributed around 70% of total revenues — approximately $1.2 billion — encompassing neurosurgery, neurocritical care, and ENT products [S1][S4]. This unit benefits notably from geographic expansion efforts into markets such as China, Japan, and Europe. The Tissue Technologies (TT) segment accounted for about 30% ($435 million), focused on wound reconstruction products [S1][S4].

Geographically, the United States remains the principal market at $1.2 billion revenue in 2025, up slightly from the prior year. Europe and Asia Pacific reported gains to $163 million and $189 million respectively; Rest of World revenues softened marginally to about $79 million [S4]. This pattern reflects both localized economic conditions and the ongoing complexity of cross-border regulatory approvals impacting product launches.

Product Innovation and Regulatory Hurdles Impacting Growth

Integra has pressed forward on innovative fronts within neurosurgical solutions with product introductions aimed at minimally invasive surgery (MIS) advancements and cerebrospinal fluid management technologies. The Aurora Surgiscope System obtained FDA 510(k) clearance in 2025 — notable as the only tubular retractor system integrating camera and lighting designed for cranial surgery [S1][N1]. Similarly, the Mayfield Ghost Base Unit Post launched to support cranial fixation needs [S1].

A distinctive feature is the advancement of CerebroFlo® external ventricular drainage catheters incorporating Endexo® anti-occlusive polymer technology aimed at reducing thrombus formation clinically [S1]. Ongoing R&D also targets combining Bactiseal antimicrobial coatings with Endexo polymer for enhanced infection control.

However, these product advances have coincided with regulatory challenges. The company has faced FDA warning letters citing manufacturing quality system deficiencies at its Boston facility — representing material operational risk [S13][N7]. These issues inevitably slow new product rollouts and necessitate elevated compliance spending that weighs heavily on margins.

Geographic Expansion and Market Penetration Trends

Growth strategies emphasize expanding product registrations and market access outside North America. Europe’s regulated environment requires concerted efforts towards EU MDR certification—a process Integra actively pursues for key devices [S1]. Similarly, China and Japan represent attractive but complex markets requiring thorough clinical evidence gathering and local product registration compliance.

Such expansions hinge critically on effective clinical data collection through prospective registries like the AERA Pediatric Registry initiated in mid-2025 to validate safety and efficacy of balloon dilation treatments for pediatric Eustachian tube dysfunction [S1]. These real-world data collections enhance payer acceptance and broaden reimbursement horizons amidst stringent market entry barriers common to surgical medtech.

Fiscal Performance Breakdown: From Profitability to Losses

Integra’s fiscal results reveal stark contrasts between recent profitable runways versus current losses. Despite incremental top-line advances (+1.5% from $1.61B in 2024), operating income swung dramatically from positive $28 million for FY2024 to a sizable operating loss of $493 million in FY2025 [F1]. Net income followed suit plunging from approximately -$7 million loss prior year to a substantial -$516 million loss — reflecting special charges tied largely to remediation efforts against compliance setbacks [F1].

This translated into an adverse approximate return on equity near -49.5% given equity contraction during the period [F1]. The breakdown evidences intensifying pressure on margins where gross margin fell below prior-year levels (54.8% to roughly 50.9%, per SEC disclosures). Cost of goods sold rose sharply along with rising SG&A expenses focused on legal, quality improvements, and innovation investments [S16]. Such swings underscore challenges balancing innovation investments against tightening operational controls required by regulators.

Cash Flow Constraints and Capital Allocation Strategy

Operating cash flow deteriorated substantially by more than sixty percent to around $50 million compared to over $129 million generated in the previous year [F1]. Capital expenditures remained elevated at approximately $81 million down modestly from prior year levels but still reflective of ongoing capacity investments including manufacturing upgrades necessitated by regulatory directives [F1][S16].

Free cash flow consequently turned negative by about $31 million when contrasting CFO minus Capex figures [F1]. This is further exacerbated by reduced flexibility in capital allocation — share buybacks halted following expiration of a prior program with trivial repurchase activity ($221k) during FY2025 versus significant prior repurchases [$52M+$275M earlier] [F1].

Dividends have not been issued since inception due to restrictions under the Senior Credit Facility which caps dividend capacity amid high leverage ratios [S10][S5]. This facility currently imposes covenants adjusted through mid-2026 under a covenant relief period allowing up to five times consolidated leverage tapering thereafter progressively lower through late 2027 [S5][S20]. Total debt remains substantial around $1.86 billion including term loan facilities at prevailing interest rates varying circa mid-5% range continuing into maturity windows across next three years [S21].

The liquidity cushioning is solidified by working capital above $700 million at year-end largely driven by lower current liabilities alongside strong current asset bases +2.54x current ratio supportive of near-term operating demands [F1][S5]. However, preservation of cash remains critical given negative earnings trajectory.

Risk Factors: FDA Compliance and Manufacturing Challenges

The most conspicuous risk centers on regulatory compliance nuances following FDA enforcement actions targeting quality system inadequacies at discrete manufacturing nodes notably Boston operations [S13]. These deficiencies not only incur direct remediation costs but trigger heightened scrutiny delaying filings and constraining sales channels particularly within high-stakes neurosurgical device categories.

Management has responded via strengthening leadership appointments specifically elevating roles within quality assurance, legal affairs, and technology development domains—moves aimed at restoring regulatory confidence per recent announcements [N7]. Nevertheless, pending arbitration over acquisition-related contingencies plus active class action securities litigation indicate broader governance risks entwined with these manufacturing issues[S13].

Navigating this multi-dimensional compliance landscape while sustaining innovation momentum is pivotal for maintaining market trust among professional users who rely deeply on surgical precision instruments coupled with regenerative biomaterials—both hallmarks of Integra’s moat.

Key Milestones Ahead and Strategic Watchpoints

Looking forward, central milestones include completion of patient enrollment targets within registries like AERA Pediatric scheduled through mid-2026 providing tangible real-world evidence supporting reimbursement negotiations internationally [S1][N1]. Completeness of EU Medical Device Directive (MDD) recertification efforts remains critical as lack thereof could restrict sale continuity within European markets affecting CSS revenue pipelines.

Given absence of explicit formal guidance from management recently disclosed calls but emphasis pivoted towards execution on clinical data readouts combined with stepwise resolution of compliance matters signifies caution toward immediate forecasts while retaining medium-term confidence rooted in neurosurgical leadership status[N1]. Careful attention should be paid to quarterly cadence shifts in costs associated also with quality system upgrades plus how they impact earnings beyond FY25.

Capital markets should watch any signals around covenant adjustments post relief period expiration yet maintaining stable leverage trajectory remains essential for flexibility allowing continued investment into differentiated product lifecycles including next-gen MIS tools leveraging proprietary polymers like Endexo.

This analysis synthesizes publicly available SEC filings, earnings transcripts, industry context relevant for medical technology companies navigating regulatory complexity while investing heavily in innovation-driven growth segments such as neurosurgery. It refrains from investment recommendations focusing purely on factual reporting anchored by reported financial metrics as of full-year FY2025 disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments