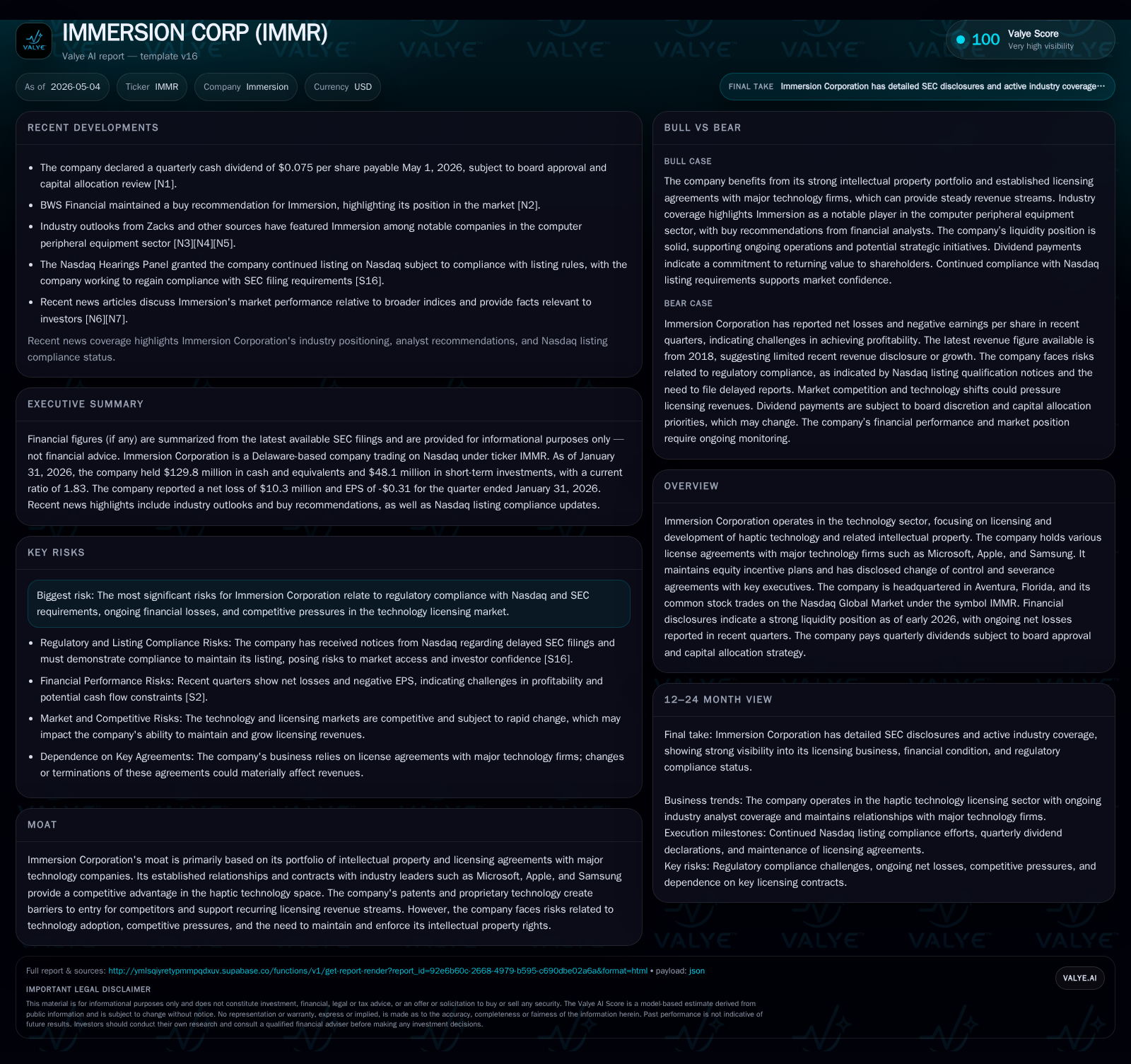

Immersion Corporation Eyes Stability and Growth Through Patent Licensing Amid Recent Nasdaq Listing Compliance

Immersion’s May 2026 quarterly report reveals progress on Nasdaq compliance alongside steady patent licensing performance, shaping a cautious yet constructive near-term outlook.

Immersion Corporation’s latest 10-Q filing highlights the company’s ongoing efforts to satisfy Nasdaq Listing Rule requirements following previous filing delays while maintaining its core business of licensing haptic technology IP to major tech players. The firm’s robust patent portfolio and established alliances underpin recurring royalty revenue streams, though recent quarters continue to reflect net losses amid operational and regulatory headwinds. Growth catalysts include expansion into emerging application areas of haptic technology, with risks centered on regulatory compliance, enforcement challenges, and the pace of customer adoption. Key upcoming milestones include the Nasdaq compliance deadline in May 2026 and continued license renewal developments, with a financial snapshot showing solid liquidity and manageable debt.

Latest Quarterly Update: Nasdaq Compliance and Operating Traction

Immersion Corporation's May 4, 2026 10-Q filing marked a pivotal moment in its regulatory journey by disclosing the company's successful request for an extension to comply with Nasdaq Listing Rule 5250(c)(1), which requires timely SEC filings [S2][S3]. Following prior delinquency notices for late submission of quarterly reports covering fiscal quarters ending July 31, 2025 through January 31, 2026, Immersion has shown operational resolve to bring filings current without immediate suspension or delisting threat. The Nasdaq Hearings Panel granted additional time through May 22, 2026, contingent on Immersion demonstrating full compliance [S24].

While regulatory compliance dominates near-term headlines, the operating context remains anchored in the company’s fundamental business of patent licensing. Despite ongoing net losses reported over recent quarters, Immersion continues to steward its relationships with leading technology firms and fortify its intellectual property assets [S2]. This dual-pronged effort underscores a critical inflection where governance stability must align with revenue resilience.

Business Model Overview: Licensing Core IP in Global Haptics Tech

Immersion derives nearly all of its revenue from licensing a comprehensive suite of haptic technology patents to marquee customers including Microsoft, Apple, Samsung, among others [S1]. These license agreements typically involve upfront fees combined with recurring royalties tied to product sales embedding Immersion’s patented tactile-feedback components. This licensing approach generates high-margin revenue streams largely insulated from direct manufacturing or distribution costs.

The firm’s revenue mechanics rest on usage-based royalties—customers pay based on units sold or integrated haptic-enabled devices—creating stable income as these underlying markets expand. Long-term contracts offer some predictability; however, renewal cycles require maintaining technological relevance and negotiating favorable terms. The inherent switching costs arise both from technical integration complexity and legal deterrents enforced by Immersion’s patent portfolio.

Licensing also fosters implicit incentives for large OEMs to retain agreements rather than risk litigation or expensive redesigns due to Immersion's rights enforcement history [S1][F1]. This model scales organically with the adoption of immersive interfaces broadly across consumer electronics.

Competitive Position: Moat Built on Patents and Tier-1 Partnerships

Immersion's competitive moat is entrenched chiefly in its intellectual property dominance within the nascent but fast-evolving haptics space [S1]. Its portfolio encompasses foundational patents essential for tactile feedback mechanisms integral to a wide array of touch-enabled devices. This establishes high barriers to entry for new competitors given substantial legal and R&D hurdles.

Beyond pure IP control, existing license agreements with industry leaders serve as strategic partnerships anchoring recurring revenue and creating significant client stickiness. These alliances provide privileged access to market trends and allow Immersion to tailor its patents’ applicability toward emerging technologies like virtual reality controllers or automotive interfaces.

The strength of this position is reflected by sustained royalty inflows despite macroeconomic uncertainties in consumer hardware markets. Nevertheless, innovation by rivals or patent expirations remain latent threats necessitating continual IP refreshment and enforcement agility.

Growth Catalysts: Expanding Application Areas and Licensing Renewal Momentum

Structural growth opportunities stem from growing demand for haptics beyond traditional smartphone applications into gaming consoles, wearable devices, augmented reality (AR), virtual reality (VR), automotive human-machine interfaces (HMI), and industrial controls [S1]. As user interaction moves towards seamless multisensory environments, haptic feedback plays an increasingly vital role enhancing immersion.

Renewal momentum for key licenses offers another lever if Immersion can successfully negotiate extensions or upsell newer patent families aligned with next-generation devices. Market penetration into emerging regions or verticals may also unlock incremental streams given increasing device pervasiveness worldwide.

Industry innovation cycles favor licensors preserving broad patent coverage compatible with evolving hardware design trends—this positions Immersion well if it invests efficiently into patent development while shielding its core royalties base.

Risks and Watchpoints: Regulatory Requirements, Adoption Pace, and Financial Losses

A critical risk cluster lies in regulatory compliance pressures tied to multiple recent delayed filings prompting Nasdaq scrutiny [S2][S3]. Continued failure could lead to trading suspension or forced delisting impairing capital access and investor confidence.

Additionally, product adoption uncertainty affects royalty volume sustainability; slower-than-expected uptake of new haptic technologies or loss of major licensees would impact revenue durability. Enforcement expenses required for defending IP rights also weigh on margins.

Persistent net losses reported in recent quarters imply operational leverage challenges; without clear profitability inflection signs or cost containment breakthroughs disclosed yet [S2], the financial path remains a watchpoint combining governance risks with capital efficiency concerns.

What to Monitor Next: Compliance Milestones, Revenue Trends, and Portfolio Developments

Investors should closely track progress toward meeting Nasdaq's May 22 compliance demonstration deadline as reaffirmed by the latest hearings decision [S24]. Filing subsequent delayed quarterly reports promptly will be critical for regulatory standing.

Operationally, quarterly revenue updates indicating stable or improving royalty income will signal whether underlying licensing deals maintain strength amid evolving customer dynamics. Announcements regarding new license agreements or renewals with major tech firms will serve as key demand indicators.

Management commentary around patent pipeline expansion or cost management initiatives may provide clues on margin improvement prospects ahead of future reporting periods.

Financial Snapshot: Liquidity, Debt Profile, and Near-Term Profitability Indicators

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $130mm | |

| 2026-01-31 | ||

| Current assets | $1013mm | |

| 2026-01-31 | ||

| Current liabilities | $554mm | |

| 2026-01-31 | ||

| Current ratio | 1.83x | |

| 2026-01-31 |

Source: SEC companyfacts cache [F1].

| Metric | Latest Value |

|---|---|

| Cash & Equivalents | $129.8 million |

| Total Debt | $103.1 million |

| Current Ratio | 1.83 |

| Net Income (Recent) | Ongoing net losses |

As of the quarter ended January 31, 2026, Immersion holds approximately $130 million cash reserves against $103 million total debt yielding a net-debt negative position of roughly -$27 million [F1]. The current ratio stands at a healthy 1.83 indicating solid short-term liquidity coverage relative to liabilities [F1].

However, recent earnings remain affected by continuous net losses suggesting operating expenses—and possibly enforcement costs—outpace revenues at present [S2]. The balance sheet strength provides breathing room but execution on revenue growth and cost discipline will be vital for reaching sustainable profitability thresholds.

This analysis is based solely on disclosed company filings through May 4, 2026 ([S1], [S2], [S3], [F1]) along with Valye News proprietary sector knowledge. It does not constitute investment advice or recommendations but aims to provide an informed operational perspective on Immersion Corporation's business status amid evolving regulatory conditions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments