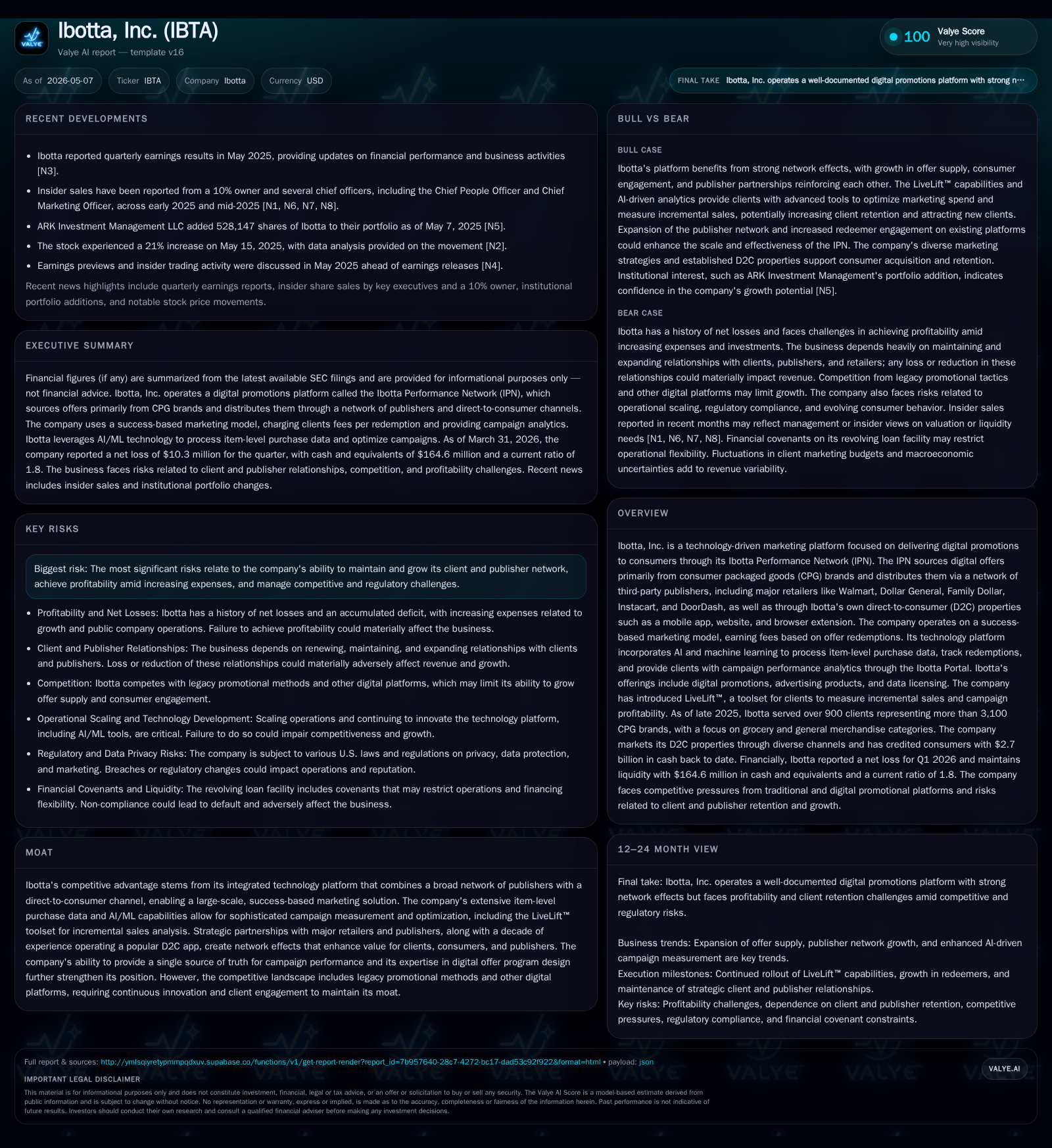

Ibotta Strengthens Success-Based Marketing with Expanding Publisher Network

Ibotta's Q1 2026 update highlights AI-driven platform enhancements and growing partnerships that deepen its integrated digital promotions network.

In its latest quarterly filing, Ibotta reinforced its position as a leading success-based marketing platform by expanding both client engagements and its publisher network. The company continues to invest heavily in AI and machine learning capabilities that enhance offer targeting and performance analytics, particularly through tools like LiveLift™. While revenue growth prospects appear structurally supported by a diversified portfolio of publishers and direct-to-consumer channels, rising expenses and legal risks present ongoing challenges for profitability. Monitoring client retention and technological rollout will be critical in assessing Ibotta's trajectory.

Recent Quarterly Operating Developments and Their Implications

In its Q1 2026 10-Q filing dated May 6, Ibotta disclosed sustained momentum in expanding its ecosystem of clients and third-party publishers [S2][S3]. The company highlighted intensified investments in artificial intelligence (AI) and machine learning (ML) initiatives aimed at refining campaign measurement, notably through the LiveLift™ toolset introduced in 2025. This system enables granular assessments of incremental sales impact and cost efficiency metrics like cost-per-incremental-dollar (CPID), which are pivotal for clients seeking optimized promotional ROI.

Importantly, the reporting affirms ongoing onboarding of new publishers across strategic verticals such as pharmacy and specialty retail, complementing established relationships with notable entities like Walmart, Dollar General, Family Dollar, Instacart, and DoorDash. These moves signal validation of Ibotta’s growth strategy centered on deepening integration within both retailer ecosystems and multi-channel offer distribution platforms.

Operationally, the company maintains strong focus on client engagement metrics — currently serving over 900 clients covering more than 3,100 consumer packaged goods (CPG) brands — alongside steps to augment redemption rates per consumer on publisher platforms [S2][S3]. However, this growth coincides with elevated expenses from technology deployment efforts.

How Ibotta's Business Model Captures Value Through Success-Based Promotions

Ibotta operates the Ibotta Performance Network (IPN), a technology-driven marketing platform earning fees solely based on successful consumer purchase redemptions of digital offers [S1][S27]. Clients—primarily CPG brands—create campaigns by defining product eligibility, budgets, offer values, expiration dates, and tailoring based on consumer purchase history.

These offers are distributed both through Ibotta’s direct-to-consumer channels (mobile app, website, browser extension) and an expanding network of third-party publishers who host offers on a white-label basis. Consumers redeem offers without needing an Ibotta account when using third-party platforms.

Revenue generation hinges on successful conversion of these digital promotions into transactions tracked at the item level via proprietary AI/ML algorithms analyzing purchase data streams. The IPN infrastructure encompasses data ingest from partner retailers/publishers feeding into analytical tools such as the Ibotta Portal—a centralized dashboard delivering real-time campaign performance insights to clients.

This model benefits from scalable platform integration capable of handling high redemption volumes across multiple verticals while enabling advanced incremental sales measurement capabilities through proprietary inventions like LiveLift™, which helps link media spend directly to incremental revenue outcomes.

Competitive Dynamics: Industry Structure and Ibotta’s Differentiated Position

The digital promotions industry is fragmented with competition from legacy couponing methods (print & in-store promotions) as well as numerous digital marketing platforms attempting to capture sponsor budgets. Ibotta distinguishes itself through a comprehensive ecosystem combining a broad set of large-scale strategic partners (notably Walmart’s extensive footprint) and deep technical integration providing unique item-level attribution [S1][S27].

Its white-label publisher relationships allow seamless embedding of offers across diverse consumer touchpoints without friction caused by separate account requirements—a form of distribution leverage difficult for newer entrants to replicate quickly.

Another moat element is the company's ability to serve as a “single source of truth” for campaign analytics. LiveLift™ provides standardized incremental sales measurements validated by third parties such as Circana—heightening trust for CPG clients budgeting at scale. Switching costs accrue as brands leverage accumulated data insights over time coupled with multi-retailer reach.

Nonetheless, competitive pressures remain from digital ad tech giants optimizing their own shopper marketing solutions plus evolving retail media networks emphasizing first-party data ownership. Legacy promotional budgets also pose inertia challenges requiring continuous innovation to migrate spend toward success-based digital alternatives.

Growth Catalysts: Technology, Client Expansion, and Network Effects

Ibotta’s growth prospects center on several intertwined drivers:

- Client Base Expansion: With over 900 active clients representing more than 3,100 brands mostly in non-discretionary categories like grocery but increasingly including general merchandise such as toys or beauty products [S1], continued penetration into new verticals—especially pharmacy chains—promises incremental volume.

- Publisher Network Expansion: Dedicated teams focus on broadening IPN’s third-party publishers horizontally across grocery/mass/pharmacy retailers plus vertically into delivery services and specialty stores. Growing this distribution footprint increases audience scale driving redemption frequency per user [S1][S26].

- AI-Driven Optimization: Substantial R&D investments back enhanced targeting algorithms improving offer relevancy; this personalization drives higher redemption rates which feed up improved revenue effectiveness metrics accessible via client reporting tools.[S2]

- Direct-to-Consumer Upside: Growth in the D2C app ecosystem remains important to engage consumers directly while feeding cross-platform data flows enhancing overall marketing intelligence.

Collectively these reinforce network effects where client acquisition attracts publishers wanting programmatic offer content while publishers’ audiences draw more client demand forming virtuous cycles.

Risks and Bottlenecks Impacting Scalability and Profitability

Key risks outlined remain consistent with prior reporting but bear reiteration given their magnitude:

- Profitability Uncertainty: Ibotta reports ongoing net losses accompanied by forecasted rising operating expenses required for technology investments and scaling publisher/client acquisition efforts [S1][S2]. Realizing sustainable profitability depends on balancing growth spending with margin accretion.

- Client & Publisher Retention: Success hinges on renewing existing client contracts while onboarding new ones at rates that offset churn. Similarly sustaining publisher relationships requires those entities to maintain technical integrations and promote maximal offer redemptions—a dependency outside direct control [S1].

- Regulatory Environment: The company operates within complex US federal/state laws around data privacy (including behavioral advertising), mobile platform regulation, consumer protection statutes all subject to evolving enforcement standards increasing compliance costs [S1].

- Competitive Threats: Established digital promotion rivals plus emerging retail media platforms constantly challenge market share gains.

- Legal Proceedings: Ongoing securities class action lawsuits filed against Ibotta could impose financial burdens or distract management despite intent to vigorously defend [S1][S22].

Collectively these dimensions impose execution discipline constraints amid market uncertainties.

Key Milestones to Monitor in the Coming Quarters

To gauge progression toward strategic targets investors may focus on:

- Client Renewal Rates: Stability or improvement signals successful value delivery amid competitive pressures.

- Publisher Network Growth Pace: Particularly new contracts in target verticals like pharmacies where incremental revenue can accrue.

- LiveLift™ Adoption & Functionality Enhancements: Tracking upgrades indicating improved granularity or efficiency can hint at upgraded pricing power or margin expansion potential.

- Campaign Metrics via Ibotta Portal Usage: Increases in active campaigns or redemption volumes reinforce demand momentum.

- Expense Management Initiatives: Monitoring operating cost trends relative to revenue growth will be pivotal for assessing profitability inflection timing.

Regular disclosures addressing these elements will provide clarity on execution effectiveness.

Latest Financial Snapshot: Liquidity and Profitability Trends

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $165mm | |

| 2026-03-31 | ||

| Current assets | $361mm | |

| 2026-03-31 | ||

| Current liabilities | $201mm | |

| 2026-03-31 | ||

| Current ratio | 1.8x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026, Ibotta holds $164.6 million in cash and equivalents with no reported debt outstanding [F1], yielding a current ratio near 1.8 reflective of ample short-term liquidity capacity. This balance sheet position supports ongoing investments into AI technologies and network expansion without immediate refinancing pressure or leverage constraints [F1].

However, the company posted an operating loss of $841 thousand for full year ended December 31, 2025 while reporting a net income of $3.58 million—suggesting non-operating factors contributed positively during that period [F1]. Overall profitability remains fragile with elevated spending on R&D and sales/marketing reported alongside growth-stage business model characteristics [F1][S2].

Management’s recent increased authorization for share repurchase programs signals confidence in capital allocation flexibility should cash flow improve [S23]. Nevertheless maintaining disciplined expense growth aligned with revenue gains will be necessary for durable earnings improvements.

This analysis is based exclusively on publicly available SEC filings dated through May 7, 2026 ([S1]-[S29], [F1]), with no investment recommendations intended or implied.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments