ONE Group’s Q1 Performance Tests Capital-Light Expansion Strategy

Q1 2026 results reveal modest net income amid liquidity constraints that challenge ONE Group Hospitality’s franchising-led growth approach.

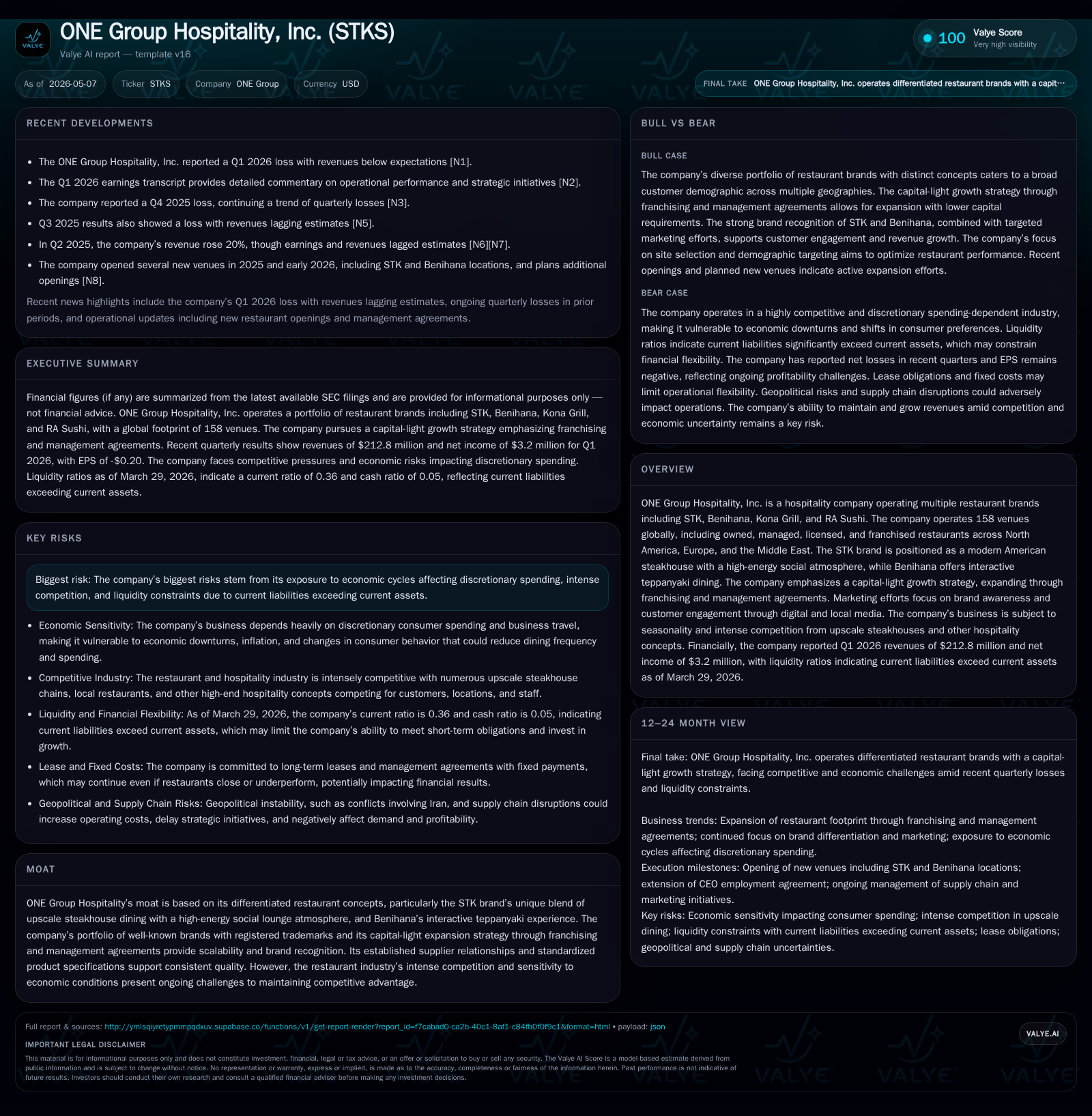

In the first quarter ended March 29, 2026, ONE Group Hospitality reported revenues of $212.8 million and a net income of $3.2 million, marking a rare quarterly profit amid an overall challenging operating environment. The company continues to pursue a capital-light expansion strategy through franchising and management agreements, leveraging its differentiated brand portfolio including STK and Benihana. However, liquidity pressures remain acute with a current ratio of just 0.36, underscoring potential risks to sustaining growth without operational improvements or financing relief. Demand dynamics reflect ongoing sensitivity to discretionary consumer spending and geopolitical uncertainties that could complicate supply chains and cost management going forward.

Q1 2026 Operating Update Highlights

ONE Group Hospitality reported first quarter revenues of $212.8 million alongside a net income of $3.2 million for the period ended March 29, 2026 [N1][S2]. This quarterly profit is notable given the company's broader annual net loss context but also underlines the unevenness in financial performance driven by operational challenges and industry headwinds. The filing dated May 6, 2026 (10-Q) confirmed no material changes in risk factors but highlighted ongoing concerns around geopolitical instability affecting costs and operations [S2]. The contemporaneous earnings call emphasized the company’s efforts to maintain growth momentum amid these headwinds by focusing on margin improvement initiatives and cautious site selection for new openings [N2].

The Q1 results reflect typical industry seasonality but also suggest that the capital-light expansion approach through franchising is providing some cushioning against fixed cost pressure inherent in fully owned venues.

Business Model and Brand Portfolio Overview

ONE Group Hospitality operates a multi-brand restaurant portfolio primarily comprising STK, Benihana, Kona Grill, and RA Sushi across North America, Europe, and the Middle East with approximately 158 venues globally [S1]. The company employs a ‘‘capital-light’’ strategy focusing on franchising, licensing, and management agreements rather than pure ownership which allows scalable expansion with lower upfront capital expenditure burdens [S17]. This model yields management fees tied to top-line sales at franchised locations alongside margins from owned restaurants.

STK stands out as an upscale steakhouse blended with an energized lounge atmosphere featuring DJs and social dining settings — a socio-dining ‘‘vibe’’ concept that targets customers seeking both quality food and entertainment in urban centers [S1][S17]. Average domestic STK owned/managed locations generate roughly $14 million in revenues annually with an average check size around $129 per person indicating strong pricing power within its niche [S17].

Benihana leverages interactive teppanyaki cooking performances as a key customer engagement differentiator, offering communal dining experiences that mix entertainment with cuisine. It operates both owned (75) and franchised (11) units primarily in the U.S., Latin America (excluding Mexico), and Caribbean markets with average unit volumes near $6.3 million domestically [S22]. The blend of experiential service plus established brand equity supports customer retention but requires skilled labor deployment to sustain quality.

The company's other concepts like Kona Grill and RA Sushi contribute diversified exposure across casual dining categories but have seen some locations consolidated or converted to STK or Benihana formats consistent with strategic focus on high-performing brands [S1]. Overall revenue generation is driven by volume at owned units plus royalties/fees from franchised/licensed sites.

Competitive Positioning and Industry Dynamics

ONE Group competes intensely within the upscale dining segment characterized by high consumer expectations on quality, service, ambiance, and innovative concepts. Competitors range from traditional steakhouses to emerging lifestyle restaurants blending food with nightlife elements [S25]. The industry remains vulnerable to shifting consumer preferences away from beef or high-end dining toward more casual or health-conscious alternatives impacting menu demand elasticity.

Supply chain dynamics add complexity as increased tariffs or geopolitical events can affect commodity costs notably for meat and seafood categories critical in menus across all concepts; cost inflation frequently triggers menu price adjustments that may dampen traffic if not carefully balanced [S1][S25]. Seasonality also plays a role given dependence on business travel patterns (notably for hotel casino based venues) which majorly contribute weekday revenues and discretionary consumer spend cycles sensitive to macroeconomic fluctuations [S20].

The company’s multi-region presence exposes it also to operational risks stemming from local market economic variations coupled with concentration risk given multiple venues sometimes clustered within single metropolitan areas; adverse developments such as labor strikes or regional declines disproportionately affect returns relative to more geographically dispersed competitors [S26]. Furthermore, emerging technological trends require adaptation in marketing (for example AI-based analytics for customer insights) where better-resourced competitors might hold advantages.

Growth Drivers and Strategic Initiatives

ONE Group’s targeted expansion hinges on identifying metropolitan markets demonstrating robust demographics favoring high-end social dining and securing seasoned franchise partners able to execute the brand experience while adhering to operational standards [S17][N2]. A recent landmark deal grants rights for ten new Benihana-based restaurants including express formats throughout the San Francisco Bay Area — scaling via operator partnerships aligns well with capital-light mandates while accelerating presence in lucrative coastal markets [N2][S17].

Digital marketing campaigns leveraging social media coupled with tailored local promotions aim to deepen customer engagement improving visit frequency among core clientele while building awareness ahead of new venue launches across all brands. Brand differentiation through event programming (e.g., DJs for STK), signature menu innovation, and curated beverage offerings further buttresses competitive positioning.

Organic growth is paced deliberately; new openings are typically focused on conversions or relocations requiring moderate investment (~$1.5 million), rather than aggressive footprint increases minimizing leverage pressures amid liquidity constraints highlighted below [N2][S17]. Backlog execution provides visible milestones offering potential topline lifts if consumer confidence remains stable.

Risk Factors and Operational Constraints

Liquidity poses a significant risk spotlighted by a current ratio of just 0.36 as current liabilities ($130.2M) substantially outstrip current assets ($46.5M) according to quarter-end March 29 data — reflecting short-term working capital tightness which could constrain operational flexibility or stunt ability to react swiftly to market shifts without external funding support or cash flow improvement measures[F1][S2].

The cyclical nature of discretionary consumer spending remains pivotal; any prolonged economic softness or dampened business travel post-pandemic could reduce average check sizes or visit frequency materially affecting top-line performance especially given elevated fixed lease commitments which persist even if outlets close temporarily [S18][S20]. Regulatory complexities including labor laws as well as geopolitical instability notably connected to Middle East exposures present ongoing volatility impacting supply inputs costs or access to certain markets due to sanctions/compliance burdens discussed explicitly for Iran conflict risks[S9][S16].

Competitive intensity meanwhile demands continued investment in brand relevance requiring balancing cost containment without eroding guest experience — failure here could undermine customer loyalty amid plentiful alternative options.[S25]

Key Milestones and What to Watch Next

Investors should track sequential same-store sales trends especially given heightened economic uncertainty as early indicators of demand sustainability per management’s remarks during recent earnings calls[N2][S3]. Progress in executing new franchise openings particularly those from landmark agreements like the San Francisco Bay Area Benihana deal will be telling for growth trajectory absent capital-heavy moves. Updates on margin improvement initiatives including cost control metrics will signal how effectively operating leverage can be leveraged against rising input prices.

Given liquidity concerns monitoring quarterly free cash flow generation versus debt servicing needs is prudent though no immediate refinancing developments have been announced[S3]. Insight into managerial commentary regarding lease obligation management strategies especially concerning closed or relocated venues would add clarity on risk mitigation plans.

Finally, watch for any changes in guidance from updated SEC filings or earnings releases that may recalibrate expectations about expansion pace or profitability outlook amid ongoing external pressures.

Latest Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $6mm | |

| 2026-03-29 | ||

| Current assets | $46mm | |

| 2026-03-29 | ||

| Current liabilities | $130mm | |

| 2026-03-29 | ||

| Current ratio | 0.36x | |

| 2026-03-29 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Date |

|---|---|---|

| Cash & Equivalents | 6,121,000 | |

| 2026-03-29 | ||

| Current Assets | 46,473,000 | |

| 2026-03-29 | ||

| Current Liabilities | 130,178,000 | |

| 2026-03-29 | ||

| Current Ratio | 0.36 | |

| 2026-03-29 |

This snapshot poignantly illustrates the liquidity challenge constraining ONE Group Hospitality’s capacity to maneuver without either operational windfalls or capital structure adjustments[F1]. Net debt approximates $41.9 million when cash is offset against total debt estimated earlier[F1], highlighting moderate leverage appropriate for an expansion-stage hospitality firm but underscoring tight working capital under current conditions.

DISCLAIMER: This analysis is provided solely for informational purposes based on public SEC filings and related news sources as of May 2026. It does not constitute investment advice or recommendations regarding ONE Group Hospitality shares or securities. Readers should conduct independent due diligence respecting evolving market conditions before applying any insights herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments