Hallador Energy Advances Long-Term Capacity Pricing While Facing Margin Pressure in Q1 2026

Vertically integrated coal mining and power generation business secures $1 billion capacity agreement amid tightening cash flows and operational challenges.

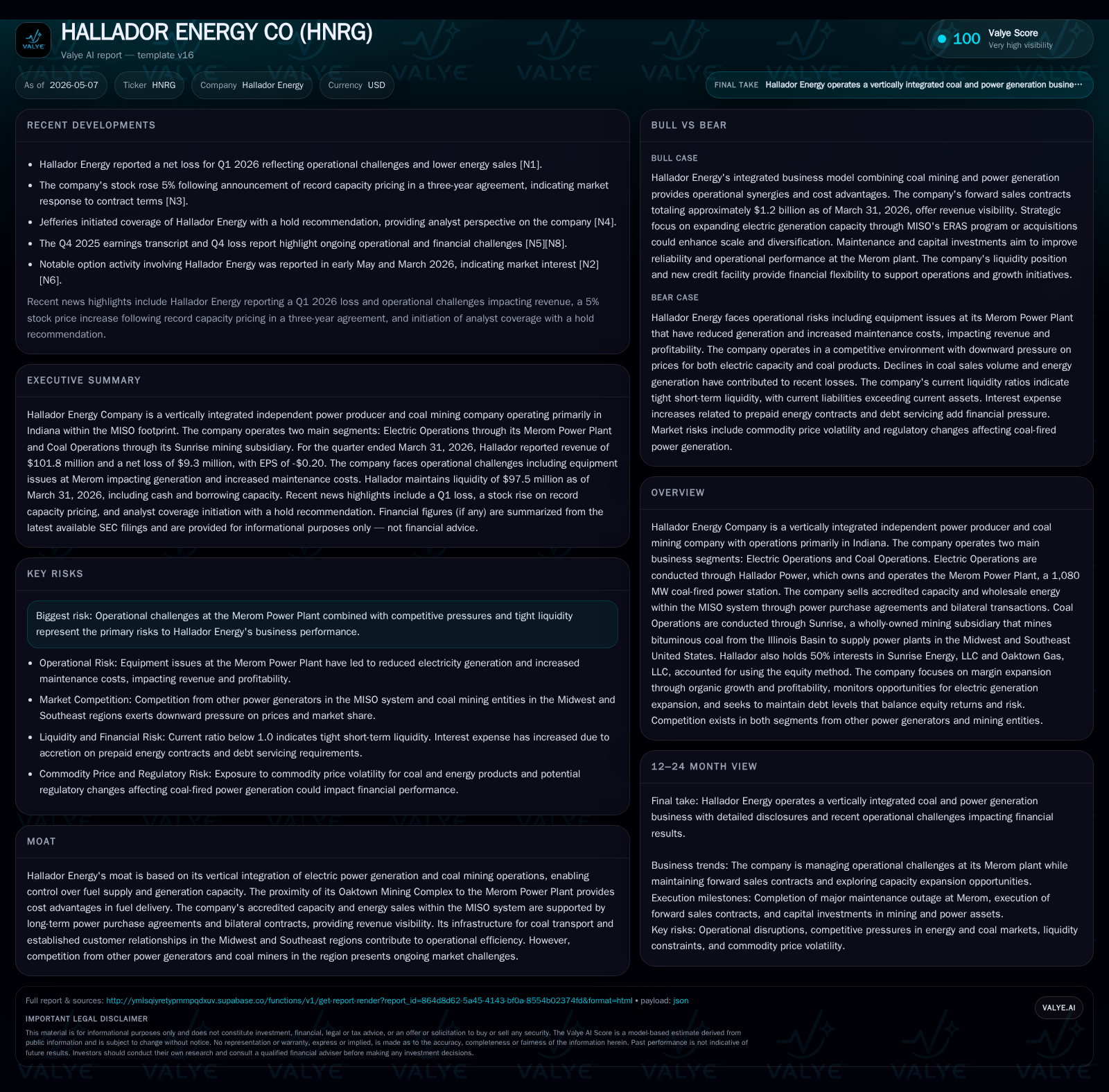

Hallador Energy Company, an integrated coal mining and independent power producer primarily operating within the MISO system, finalized a record 12-year capacity agreement valued over $1 billion in early 2026. Despite this milestone, its first-quarter 2026 results revealed lower adjusted EBITDA, increased inventory levels, and diminished net capacity utilization at Merom Power Plant, applying pressure to near-term margins. The firm’s vertical integration through coal mining at the Oaktown complex provides cost control advantages but faces structural headwinds from evolving energy markets and regulatory landscapes. Liquidity remains adequate with a new $75 million revolving credit facility, although the current ratio of 0.8 signals working capital tightness. Growth hinges on execution of long-term contracts, operational reliability at Merom, and successful capital deployment.

Recent Operating Update

Hallador Energy's latest quarterly filing for Q1 2026 confirms both strategic progress and operational headwinds shaping its near-term outlook. The company executed a pivotal 12-year power capacity contract exceeding $1 billion in value, solidifying its revenue base through long-term agreements within the Midwest ISO (MISO) footprint [S21]. This contract represents record pricing levels for accredited capacity sales from its wholly owned Merom Power Plant.

However, financial results indicate pressures beneath headline contract wins. Net cash provided by operating activities dropped to approximately $20.5 million in Q1 2026 from $38.4 million one year earlier, driven by reduced adjusted EBITDA coupled with increased coal inventory buildup and amortization effects on prepaid forward sales contracts [S5][S6]. Investing outflows slowed as capex fell to $7.7 million from prior periods — allocated mainly to sustaining mining infrastructure at Oaktown and maintaining coal-fired assets at Merom [S5].

Liquidity metrics remain supportive but reflect tighter short-term working capital constraints; Hallador reported about $36.8 million cash on hand as of March end alongside roughly $60.8 million borrowing availability under a newly established $75 million revolving credit facility (plus a delayed draw term loan) replacing an earlier $30 million PNC Bank facility [F1][S4][S8]. This facility emphasizes manageable leverage aligned with coverage covenants but leaves limited excess cushion beyond operational cash needs.

Business Model

Hallador operates as a vertically integrated independent power producer (IPP) paired tightly with coal mining operations anchored in Indiana's Illinois Basin region [S2][S23]. This structure allows seamless fuel supply through Sunrise Mining subsidiary directly to its electric subsidiary Hallador Power’s Merom coal-fired power plant.

Merom Power Plant commands a nameplate capacity of 1080 MW composed of two steam turbines dating from the early 1980s [S1]. The plant participates fully within the MISO market where it sells accredited capacity—contractual rights to deliver dependable power—and wholesale energy via PPAs and bilateral trades. Accredited capacity pricing dominates revenue visibility since market rules require equivalent capacity backing for energy consumption [S1][S22].

Sunrise Mining delivers bituminous coal primarily from the Oaktown Mining Complex near the Merom site, reducing logistics costs and enabling operational synergies absent among many smaller competitors lacking direct fuel supply control [S1][S22]. Coal is sold internally (to Merom) and externally to third-party utilities throughout Midwest/Southeast U.S., typically under firm contracts with price escalation clauses tied to coal quality metrics.

Hallador also holds equity stakes in Sunrise Energy LLC and Oaktown Gas LLC—entities that extend its operational reach though critical accounting means have consolidated only partial financial impact [S2].

Overall profitability derives from margin capture across accredited capacity sales (secured under forward contracts), wholesale energy dispatch margins affected by fuel costs/natural gas competition, and coal selling prices balanced against extraction costs.

Industry Structure & Competitive Position

As an integrated miner-generator, Hallador stands apart from simple coal miners or pure IPP peers by controlling upstream fuel extraction costs alongside downstream generation assets. Its proximity between Oaktown mines and Merom enhances flexibility not afforded to generators reliant on third-party fuel deliveries or spot market purchases.

The MISO market environment is moderately competitive with abundant natural gas-fired plants increasingly setting marginal prices due to lower emissions profiles and regulatory favorability. Coal assets historically serve baseload or peaking reliability functions but face pressures from renewable penetration and environmental compliance costs.

Given Merom’s vintage fleet dating back four decades, efficiency gains are limited relative to newer combined-cycle units; however Hallador mitigates these through long-term PPAs securing stable cash flows largely insulated from spot price volatility [S1][N3]. The recent record-setting capacity contract underscores market confidence in the plant’s dispatchability despite sector decarbonization trends.

On the supply side, Illinois Basin coal mining remains cost-competitive relative to Appalachian counterparts but contends with demand erosion driven by shifting generation mixes; nonetheless regional utilities’ reliance on cost-effective domestic bituminous coal supports Sunrise’s contracted volumes.

Growth Drivers

- Long-Term Capacity Contracts: The executed twelve-year PPA exceeding $1 billion anchors revenue visibility, ensuring stable cash flow from accredited capacity sales across investment horizon periods [S21]. Capacity pricing at record levels improves gross margin assumptions compared to historical norms.

- Contracted Coal Sales Base: Coal segment benefits from diversified contracted streams including intercompany sales to Merom (~7.55 million tons at ~$51/ton) plus third-party contracts aggregating over two million tons priced around mid-$50s per ton reflecting consistent demand underlying legacy thermal generation plants [S22].

- Operational Efficiency Initiatives: Investment maintains asset reliability across electric generation units as well as sustaining mine productivity at Oaktown; prioritizing capex programs towards core income-generating assets sustains production volume while managing cost trajectories [S5].

- Equity Stakes Complement: Holdings in Sunrise Energy LLC and Oaktown Gas LLC diversify earnings base through ancillary operations possibly contributing incremental earnings via equity method accounting gains [S2].

Risks and Watchpoints

- Aging Asset Risk: Merom Power Plant units are nearly four decades old; maintaining operational uptime without costly forced outages is critical yet challenging given equipment age and evolving emission regulations requiring potential retrofits or environmental control investments [S1][S23].

- Market Competition & Regulatory Pressure: Increasing penetration of renewables coupled with low-cost natural gas alternatives threatens long-run competitiveness of coal-fired generation within MISO markets; regulatory tightening around coal combustion residuals, water discharge permits, or air emissions could impose additional capital or operating expenses.

- Working Capital Tightness: Current ratio below unity (0.8) indicates liquidity strain requiring careful management of payables/receivables cycles especially if inventory accumulates or receivables delay collection posing unexpected stress points on cash conversion cycles [F1].

- Commodity Price Volatility: Coal pricing subject to quality adjustments and contract parameters introducing forward sales risks; shifts in natural gas prices indirectly impact wholesale electricity prices affecting energy segment margins.

- Leverage Covenants & Refinancing Needs: While new credit facilities extend maturity profiles, covenant thresholds tied to leverage ratios allow limited flexibility if Adjusted EBITDA declines further especially under adverse market conditions potentially restricting additional debt capacities [S4][S8].

What to Watch Next

Key upcoming indicators will focus around:

- Execution quality of contracted capacity delivery aligned with PPA terms measured through quarterly accredited capacity volumes reported versus contractual baselines.

- Monitoring Adjusted EBITDA trends particularly across electric operations for signs of margin recovery or further compression stemming from fuel costs or dispatch patterns.

- Capex spend adherence in sustaining reliable operations without major incremental increases signaling unplanned maintenance or regulatory obligations.

- Inventory levels trajectory given increasing raw material stock counts currently pressuring operating cash flows suggesting either demand softness or supply chain timing mismatches.

- Regulatory developments impacting operating permits at Merom or reclamation liabilities potentially affecting cost structures.

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $37mm | |

| 2026-03-31 | ||

| Total debt | $30mm | |

| 2025-12-31 | ||

| Net debt | $-7mm | |

| 2025-12-31 | ||

| Current assets | $151mm | |

| 2026-03-31 | ||

| Current liabilities | $190mm | |

| 2026-03-31 | ||

| Current ratio | 0.8x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

A snapshot as of March 31, 2026 reveals moderate liquidity: cash & equivalents totaled approximately $36.8 million supported by current assets of $151.1 million against current liabilities of $190 million resulting in a sub-one current ratio (0.8), indicating working capital tightness [F1]. Total debt stood near $30 million year-end though subsequent refinancing provided enhanced revolving borrowing availability approaching $75 million plus an optional delayed draw term loan facility expiring March 2029 collateralized by substantially all assets enhancing balance sheet flexibility beyond prior arrangements [F1][S4][S8].

Revenue for calendar 2025 remained modestly below half-a-billion dollars ($469 million), with operating income near $61 million reflecting legacy asset economics amid transitional sector dynamics [F1]. Net income was reported near $42 million for the same period.

Cash flow from operations weakened in Q1 ’26 versus prior year quarter but financing inflows associated with new credit facilities bolstered overall liquidity position providing runway to address ongoing capital programs focused on maintaining asset integrity rather than expansionary growth given industry context [S5][F1].

This analysis is based solely on publicly available SEC filings, company disclosures, and direct reporting without investment recommendations. All financial figures cited reflect latest available data as per SEC filings dated May 6, 2026 ([F1], [S2], [S3], etc.). Market conditions remain dynamic due to industry transition pressures affecting thermal coal usage.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments