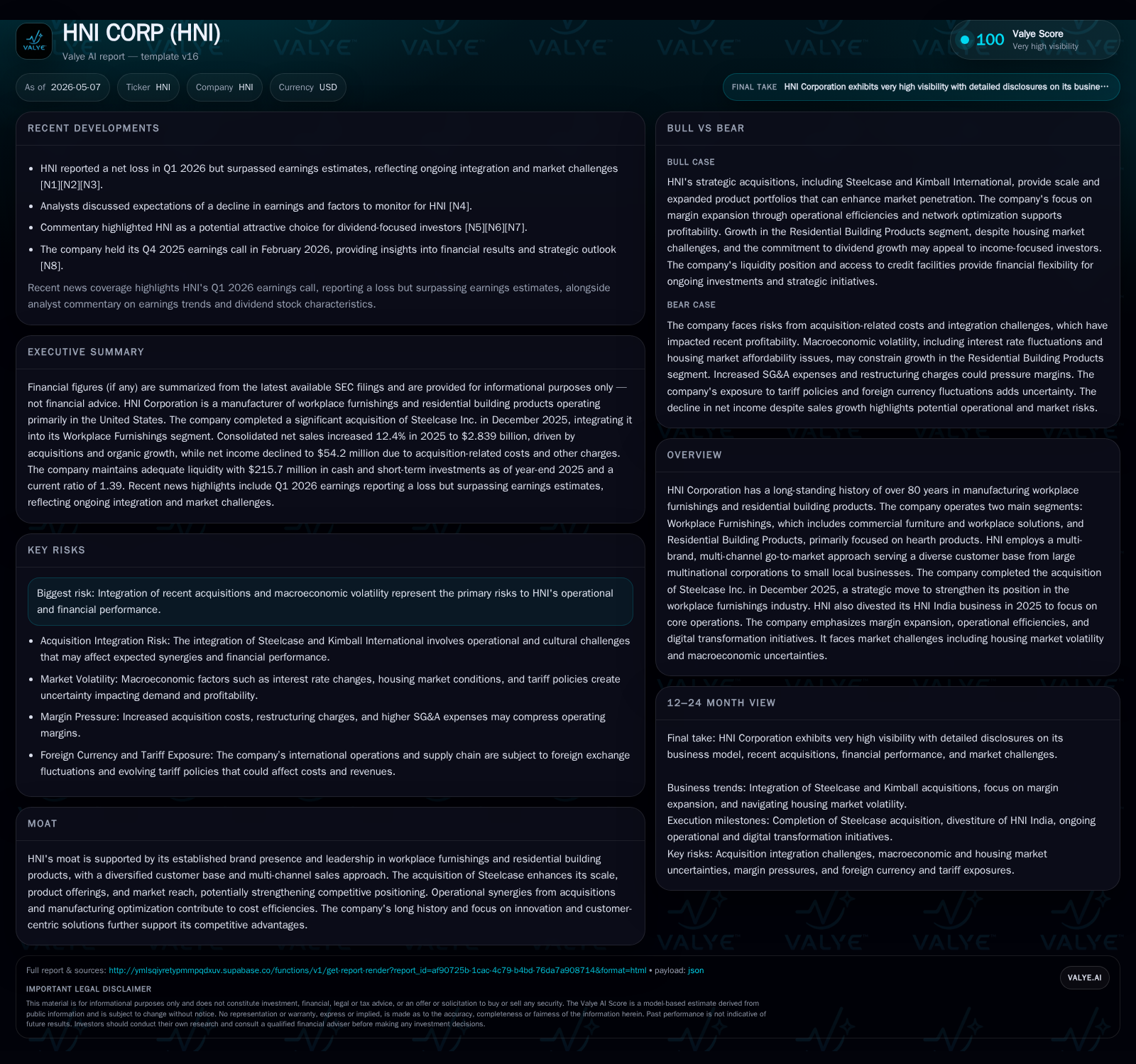

HNI Corp Advances Scale and Margin Initiatives Following Steelcase Acquisition

Q1 2026 marks HNI’s first full quarter post-Steelcase acquisition with a focus on integration, margin expansion, and operational efficiencies.

In its latest quarterly update, HNI Corporation is progressing through the integration of Steelcase, aiming to leverage scale benefits in workplace furnishings. The company continues to prioritize margin expansion via manufacturing optimization and digital initiatives while navigating challenges including housing market volatility impacting its residential building products segment. The business model centers on multi-brand commercial furniture and hearth products, with growth driven by strategic acquisitions, operational synergies, and diversified customer channels. Key risks include integration complexity and macroeconomic uncertainties. Monitoring execution on synergy realization and demand trends remains critical.

Recent Operating Update: Q1 2026 Filing Highlights

HNI Corporation’s Q1 2026 filing dated May 6 underscores the continued integration of the Steelcase acquisition completed late in 2025 [S2]. This transaction significantly reshapes HNI’s Workplace Furnishings segment by adding leading-edge design capabilities and expanded product lines. Financial results incorporate this acquisition alongside ongoing margin expansion initiatives designed to unlock synergies and operational efficiencies [S3],[S16].

Operationally, HNI is leveraging manufacturing capacity in Mexico and optimizing its network footprint which are integral to its profit transformation plan [S8],[S28]. In parallel, the divestiture of its India business in mid-2025 reflects a strategic focus on core North American operations [S17].

The Residential Building Products unit, centered on hearth-related offerings, continues navigating headwinds tied to U.S. housing market volatility stemming from interest rates and affordability challenges. Nevertheless, remodel/retrofit projects provide stable demand contributions [S7],[S28].

Business Model

HNI operates principally through two reportable segments: Workplace Furnishings and Residential Building Products [S1],[S17]. The former caters largely to commercial office environments offering panel-based systems, seating, tables, storage solutions, architectural products, and collaborative furnishings under multiple respected brands. It serves a broad customer base ranging from global corporations to smaller local entities employing a multifaceted go-to-market model including direct sales and independent dealers.

The Residential Building Products segment manufactures an array of hearth appliances such as gas, wood, pellet-fueled fireplaces, inserts, outdoor fire pits, and associated accessories primarily for the U.S. market. This business leverages channel diversity across remodeling contractors, specialty dealers, and retailers.

Revenue generation is driven by volume increases linked to new construction or renovation activity plus price realization programs addressing inflationary cost pressures. Margins are influenced by manufacturing productivity gains and scale economies especially following recent acquisitions [S14],[S28].

Industry Structure and Competitive Position

HNI occupies a leadership role in the workplace furnishings industry bolstered by its acquisition of Steelcase—a global design leader—strengthening competitive positioning through enhanced product offerings and global brand recognition [S1],[S16]. Both companies shared complementary expertise in innovative workplace solutions at the time of merger.

The commercial furnishings industry is marked by brand-driven competition emphasizing design differentiation alongside cost efficiency given commoditized components like steel framing or laminate surfaces. Distribution networks combining direct engagement with dealer partners create customer switching barriers.

In residential hearth products—which are more sensitive to housing cycle fluctuations—HNI maintains a dominant market share thanks to broad product selection adapted for various fuel types and price points [S28]. This diversification dampens exposure compared with firms focused solely on new-home construction markets.

Growth Drivers

- Acquisition Integration: Realizing cost synergies from Steelcase—estimated to drive earnings improvements over five years with modest accretion starting in 2026—is a pivotal lever for growth [S1],[S16].

- Operational Efficiencies: Ongoing manufacturing expansion in Mexico combined with supply chain optimizations amplifies margin potential amid inflationary pressures [S8],[S28].

- New Product Innovation: Investment in digital platforms alongside refreshed product portfolios supports evolving workplace needs such as flexible workspaces [N1],[S1].

- Residential Segment Stability: Continued demand for remodel/retrofit hearth products provides steady revenue streams despite broader housing headwinds [S7],[S28].

- Multi-Channel Sales: Leveraging diversified sales channels across geographies enhances market penetration across customer segments from large enterprises to smaller operators.

Risks / Watchpoints / Growth Constraints

Integration risks persist as HNI assimilates Steelcase’s operations—including cultural alignment, IT systems consolidation, and retention of key talent—which can pressure margins if not managed carefully [S1],[N4]. Moreover, prolonged inflationary trends may challenge cost control despite productivity efforts.

Macroeconomic uncertainty impacting office space utilization could suppress corporate investment in workplace furnishings varieties. Likewise, sluggishness or downturns in residential construction markets can curtail Hearth segment sales due to reduced new-build volumes or tightening consumer budgets given interest rate volatility [S28].

Additional risks encompass potential supply chain disruptions influenced by trade policy shifts (including uncertain tariff regimes after recent U.S. Supreme Court rulings), labor availability constraints affecting production levels, cyber threats imperiling operational continuity, and raw material price swings eroding margins [S18],[S20].

Financial leverage has increased post-acquisition with net debt approximating $1.37 billion supported by revolving credit facilities sufficient for near-term liquidity needs; covenants require careful compliance amid fluctuating earnings performance [F1],[S4–6].

What to Watch Next

Key upcoming milestones involve progress on facility rationalizations such as the announced exit from the Wayland NY plant slated for 2027 which ties into network optimization strategies [S26]. Monitoring achievement of synergy targets from Steelcase integration will be paramount for restoring operating income growth following Q4 2025 softness induced partly by acquisition costs [N2],[S14].

Demand indicators include same-store sales growth within core brands, backlog developments especially for commercial contracts given recent hybrid work trends resurgence indications, as well as residential housing starts or renovation spending data sustaining hearth product revenues.

Capital expenditure pacing toward digital transformation initiatives will also signal management commitment toward long-term competitiveness beyond immediate cost cutting [S20]. Furthermore, cash flow generation versus incremental debt servicing demands underpins financial flexibility.

Financial Profile (Latest Period Context)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $71mm | |

| 2026-04-04 | ||

| Total debt | $1445mm | |

| 2026-04-04 | ||

| Net debt | $1374mm | |

| 2026-04-04 | ||

| Current assets | $1297mm | |

| 2026-04-04 | ||

| Current liabilities | $936mm | |

| 2026-04-04 | ||

| Current ratio | 1.39x | |

| 2026-04-04 |

Source: SEC companyfacts cache [F1].

As of April 4, 2026 (end of Q1), HNI held $71.4 million in cash and equivalents paired against total debt near $1.45 billion resulting in net leverage around $1.37 billion on a current ratio basis of approximately 1.39 indicating adequate near-term liquidity from current assets relative to liabilities [F1].

Operating income recorded at $126 million for fiscal 2025 reflects a decline partially attributable to acquisition costs but includes baseline contributions from both segments following Steelcase consolidation [F1],[S14]. Net income stood at $54.2 million for the same period highlighting margin compression challenges post-transaction yet underpinned by sustained top-line growth.

Management anticipates capital expenditures between $140 million-$150 million for 2026 aimed at supporting ongoing modernization endeavors that align with digital transformation goals enhancing customer experiences [S20]. Dividend policy remains committed to maintenance or modest growth reinforcing stable shareholder returns despite integration expenses.

This analysis synthesizes the latest publicly available SEC filings alongside disclosed company developments without offering investment advice or recommendations. The assessment focuses on operational progress post-major acquisition while highlighting structural attributes influencing HNI's strategic positioning within industrial furnishings and residential building product markets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments