Indivior's Buprenorphine Franchise Drives Profitability Amid Legal and Cash Flow Challenges

Long-acting OUD therapies underpin Indivior's profitability while capital expenditures and ongoing litigation shape liquidity dynamics.

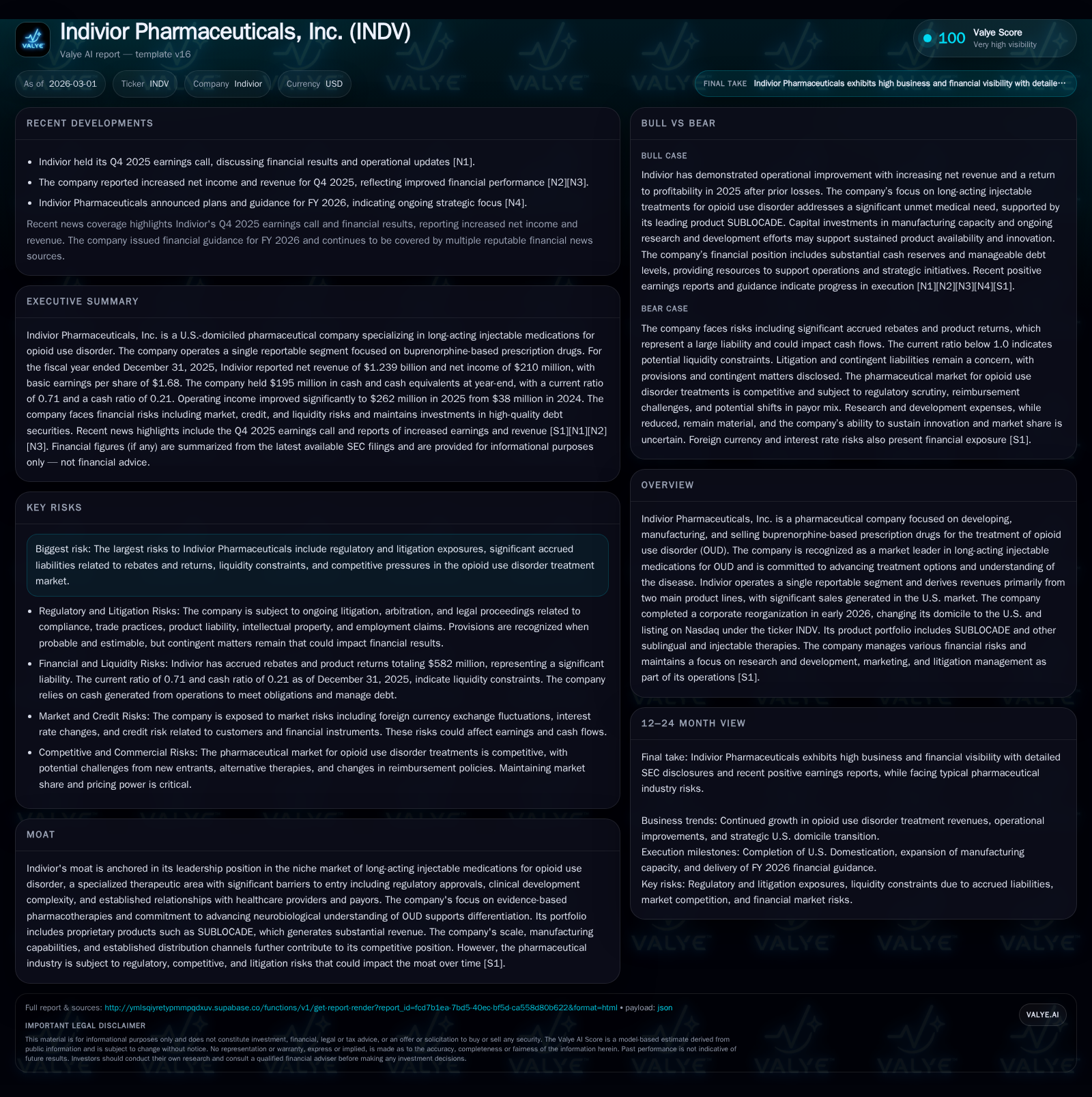

Indivior Pharmaceuticals, Inc. has established a strong position in opioid use disorder treatments, primarily supported by its buprenorphine-based products such as SUBLOCADE. Fiscal 2025 financials reveal significant growth in operating and net income, though operational cash flow turned negative due to elevated capital investments and litigation-related outflows. The company faces substantial legal and regulatory challenges but continues to manage settlements and maintain disciplined capital allocation amid debt covenant constraints. Future performance depends on sustaining core product sales and navigating ongoing legal exposures.

Company Overview and Market Position

Indivior Pharmaceuticals specializes in buprenorphine-based treatments for opioid use disorder (OUD). Following its relocation to the U.S. and Nasdaq listing under the ticker INDV early in 2026, Indivior is positioned closely with its largest market. Its flagship product SUBLOCADE, a long-acting injectable therapy, anchors its leadership within a niche marked by significant regulatory oversight and clinical complexity [S1].

Historical Financial Performance

In fiscal year 2025, Indivior reported a substantial improvement in profitability metrics. Operating income increased sharply to $262 million from $32 million in 2024—a growth rate of approximately 719%—reflecting stronger product sales alongside operational efficiencies or discrete factors reported in filings [F1]. Net income rose dramatically to $210 million compared to $2 million the prior year, demonstrating effective cost management amidst ongoing legal challenges.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 210 | -27 | 262 | 66 | +10400.0% |

| 2024 | 2 | 36 | 32 | 29 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 11 | -93 | -214.3 |

| 2024 | 173 | 7 | -0.6 |

Source: SEC companyfacts cache [F1].

Operating cash flow turned negative ($27M) compared with positive inflows ($36M) in the prior year. This decline is mainly attributable to elevated capital expenditures centered on expanding the Raleigh Manufacturing Facility — signaling investment for future growth despite near-term liquidity pressures [F1][S4]. Share repurchases were markedly reduced from $173 million to $11 million as management prioritized liquidity preservation during restrictive debt covenants tied to approximately $459 million of secured debt [F1][S6][S8].

Capital Structure and Liquidity

Indivior’s capital structure includes a note purchase agreement originally valued at $350 million with approximately $333 million outstanding at December 31, 2025. Additionally, an undrawn revolving credit facility of $50 million matures in November 2030. Debt agreements impose leverage limits at or below three times total debt relative to Adjusted EBITDA and require interest coverage ratios no less than 2.5x—benchmarks that Indivior was compliant with at fiscal year-end [S6][S8][S10]. Interest rates are indexed to SOFR plus a spread of 5.5%, increasing after September 2026.

Contractual obligations include scheduled debt repayments (approximately $59 million due within one year), litigation settlement liabilities ($8 million short term), commercial commitments ($68 million over four years), anticipated capital expenditures ($18 million next year), lease liabilities ($37 million total), and employee-related liabilities ($39 million). Total contractual commitments approximate $629 million highlighting significant fixed cash outflows that pressure working capital [S4].

Cash and cash equivalents stood at roughly $195 million at fiscal year-end December 2025. Current liabilities exceeded current assets resulting in a current ratio near 0.71 — indicative of constrained near-term liquidity necessitating careful cash management [F1][S8].

Litigation and Regulatory Environment

Indivior remains engaged in extensive opioid-related litigation stemming from the broader opioid epidemic. A key milestone was reached with the April 2025 State/Subdivision Master Settlement Agreement resolving multiple claims including many within the federal Opioid MDL. This agreement contemplates multimillion-dollar payments over several years; accrued liabilities related to these settlements total approximately $80 million inclusive of amounts held in escrow [S18][S21][S26].

Despite this progress settling government entity claims representing two-thirds of litigation volumes, over 130 private plaintiff cases remain active—many alleging neonatal abstinence syndrome—which require ongoing defense efforts and carry uncertain timing or financial outcomes [S14][S19][S22].

Additionally noteworthy is the large dental product liability multidistrict litigation consolidated in Ohio federal court involving tens of thousands of plaintiffs alleging defective design and inadequate warnings related to SUBOXONE Film’s contribution to dental injuries. Bellwether trials are not expected before late calendar year 2027. Insurance reimbursement discussions add further complexity to this matter [S11][S23].

Revenue recognition is subject to complex estimates around rebates, incentives, chargebacks linked to government programs such as Medicaid/Medicare. These estimates rely on judgment regarding customer payment behaviors affecting net revenue reporting accuracy and create regulatory risk exposure [S1][S15].

Growth Prospects and Commercial Drivers

Indivior’s entrenched position in OUD pharmacotherapy centers on proprietary long-acting injectables like SUBLOCADE which benefit from premium pricing supported by lengthy exclusivity granted through FDA approval complexity for novel delivery systems.

While explicit revenue guidance was not disclosed publicly in recent filings or earnings transcripts reviewed ([N1],[N2]), key indicators include maintaining or growing SUBLOCADE market share amid competitive dynamics including potential generic entrants or alternative therapeutics.

Pipeline developments or label expansions beyond core buprenorphine offerings have not been prominently highlighted.

Returns and Capital Allocation Insights

Financial returns present contrasts: despite substantially higher net income relative to a negative equity base (approximately negative $98 million), resulting in an approximate negative return on equity exceeding -214%, profitability improvements suggest strengthening operational cash generation potential ([F1]).

Free cash flow remains pressured given significant capital spending on facility expansion (approximately -$93 million calculated as CFO less capex). Share buybacks contracted markedly consistent with conservative balance sheet management under covenant constraints prioritizing deleveraging or liquidity preservation ([F1],[S6],[S8]). Dividend payments were not reported indicating retained earnings are likely directed toward reinvestment or legal contingencies.

Industry Context Analysis

The addiction treatment space faces regulatory scrutiny heightened by stigma associated with opioid dependency medications which can slow prescriber adoption rates. Long-acting formulations address adherence issues inherent with daily dosing while supporting integrated care models involving behavioral therapy.

High costs for Phase III trials combined with formulary restrictions create barriers protecting incumbents like Indivior; however payer reimbursement landscapes remain competitive and subject to policy shifts aimed at mitigating the opioid crisis.

Conclusion & Outlook

Indivior’s leadership in buprenorphine-based OUD treatments drove marked profitability improvements after years challenged by operational complexities intertwined with heavy legal provisions. The company balances expansive capital investments enhancing manufacturing capacity against constrained operating cash flows amid sizeable ongoing litigation expenses.

Maintaining compliance with credit covenants will be critical given upcoming debt maturities over the next five years. Legal developments around perinatal injury cases alongside dental MDL outcomes will materially influence future contingency expenses. The pace of innovation coupled with evolving payer policies may shape strategic adjustments or growth trajectories.

Key items for monitoring include:

- Quarterly sales trends for SUBLOCADE relative to competitors,

- Updates on settlement progress for remaining opioid-related civil suits including neonatal abstinence syndrome claims,

- Scheduling developments relating to dental MDL bellwether trials,

- Execution effectiveness of capital expenditure projects expanding production capacity,

- Debt covenant adherence measured via adjusted EBITDA,

- Changes in gross-to-net rebate estimates impacting future revenue recognition.

Disclaimer: This report compiles publicly available information without providing investment recommendations or price targets. All financial figures are sourced directly from verified SEC filings ([F1],[S#]) and factual news releases ([N#]). Forward-looking statements are inherently uncertain beyond the scope of this analysis.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments