Intuit’s Expansion through AI and Ecosystem Integration Strengthens Market Position

Intuit leverages AI advancements and platform synergies to drive diversified growth across business segments while maintaining financial discipline.

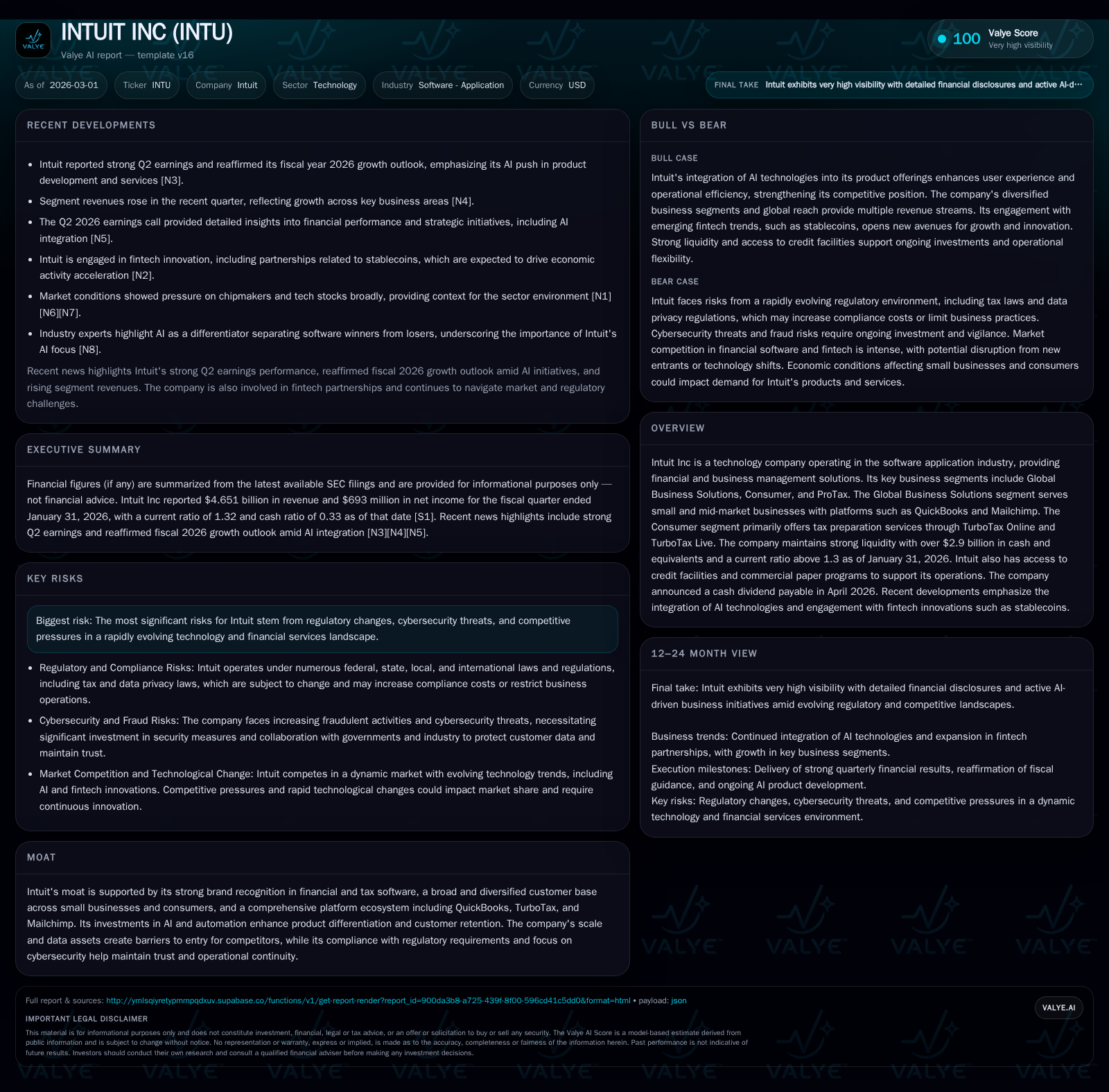

Intuit Inc has demonstrated robust growth over recent fiscal years, with a 15.6% revenue increase and strong operating income gains reflecting enhanced scale from its diversified software platforms such as QuickBooks, TurboTax, and Mailchimp. The company is accelerating AI integration and fintech partnerships, notably exploring stablecoin applications, key to sustaining differentiation in a competitive market. Recent Q2 earnings surpassed expectations, reaffirming full-year guidance amid continued investment in innovation and cybersecurity. Intuit upholds disciplined capital management, employing substantial share repurchases and dividends supported by strong cash flow generation and liquidity while navigating evolving regulatory landscapes that impose both operational risks and moat-building imperatives.

Robust Historical Growth Fueled by Diversified Segments and Platform Synergies

Over the past four fiscal years ending July 31, Intuit has achieved outstanding financial performance characterized by steady top-line expansion alongside disproportionate profitability gains. Revenue increased from $12.7 billion in FY2022 to $18.8 billion in FY2025 representing a compound annual growth rate (CAGR) of approximately 14%. The year-over-year revenue growth accelerated to 15.6% in FY2025 compared to prior periods, reflecting expanding penetration of the company's Global Business Solutions (QuickBooks and Mailchimp), Consumer (TurboTax Online/Live), and ProTax segments which serve a broad base of small businesses, mid-market enterprises, and individual taxpayers [F1].

Operating income advanced at an even more accelerated pace rising 35.6% YoY to $4.92 billion in FY2025 from $3.63 billion the prior year, indicative of scalable operating leverage amplified by automation technology investments that reduce incremental service costs across cloud infrastructure and live expert support services [[F1]]. Net income surged 30.6% reaching near $3.87 billion driven not only by operating efficiencies but effective tax planning within its complex multi-jurisdictional footprint [[F1]].

Importantly, Intuit's operating cash flow exhibited robust resilience growing 27.1% YoY to over $6.2 billion in FY2025 even as capital expenditures declined sharply by more than half due to optimization of previous investing cycles [[F1]]. This positive cash flow trajectory underscores the strength of recurring SaaS-like subscription revenue models underpinning QuickBooks' business management platforms plus sustained consumer demand for tax filing solutions.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 18.8 | 3.9 | 6.2 | 4.9 | +15.6% | +30.6% |

| 2024 | 16.3 | 3.0 | 4.9 | 3.6 | +13.3% | +24.3% |

| 2023 | 14.4 | 2.4 | 5.0 | 3.1 | +12.9% | +15.4% |

| 2022 | 12.7 | 2.1 | 3.9 | 2.6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($bn) | FCF ($bn) |

|---|---|---|---|

| 2025 | 1189 | 2.8 | 6.1 |

| 2024 | 1034 | 2.0 | 4.7 |

| 2023 | 889 | 2.0 | 4.8 |

| 2022 | 774 | 1.9 | 3.7 |

Source: SEC companyfacts cache [F1].

The lower capital expenditure aligns with maturing cloud infrastructure deployments allowing Intuit to focus on software feature enhancement rather than heavy infrastructure outlays.

AI Innovation and Fintech Partnerships Catalyze Next-Generation Growth

In recent quarters, Intuit has significantly escalated its technological advancement initiative centered around artificial intelligence integration and expanded fintech partnerships to create differentiated value propositions for customers across its segments [[N1]], [[N2]], [[N9]], [[S3]].

The company is embedding machine learning algorithms deeply into TurboTax workflows to automate data entry, error detection, personalized tax optimization recommendations, and real-time live support facilitated by AI-powered assistants—allowing tax professionals to serve more clients efficiently while enhancing customer experience [[N3]]. Simultaneously, QuickBooks is increasingly enhanced with AI-driven predictive financial insights, smart cash flow forecasting models, automated bookkeeping classification, fraud detection alerts using behavioral analytics, all delivered through a seamless cloud interface [[S3]].

Complementing these internal innovations are collaborations with payment technology providers including ventures exploring stablecoin-based transactions that promise lower friction cross-border payments and near-instant settlement capabilities for small businesses—pioneering fintech disruptions supporting economic acceleration as emphasized by Circle's CEO [[N9]]. These efforts reveal Intuit’s strategy not merely as a software provider but as an embedded financial operations partner within its customers’ ecosystems.

Such advancements underpin higher customer retention due to 'ecosystem lock-in' effects where integrated AI tools coupled with complementary fintech offerings raise switching costs significantly.

Q2 Earnings Beat and 2026 Growth Outlook: What to Watch Next

Intuit delivered an impressive Q2 FY26 earnings report beating consensus revenue and earnings per share estimates amid broad segment expansion [[N1]], [[N2]], [[N5]], [[N6]], [[N8]]. Year-to-date results show strong sequential improvement attributable to successful marketing campaigns during the tax season peak combined with platform enhancements driving incremental subscriptions.

Segment-wise revenue momentum was notable; Global Business Solutions benefited from accelerating Mailchimp adoption beyond email marketing into customer journey orchestration; Consumer segment sustained gains via TurboTax Online Live; ProTax also grew linked to season extension services catering to accounting firms [[N3]]. Margins remained healthy due to productivity gains despite ongoing investments in AI innovation.

Management reiterated full-year FY26 guidance endorsing mid-teens revenue growth pace consistent with prior years while emphasizing milestone delivery around new AI feature rollouts planned for the second half as well as deepening fintech ecosystem integrations [[N3]], [[N8]].

Going forward, key indicators include subscription net dollar retention rates across QuickBooks users post-AI launch phases, new loan product uptake velocity under fintech partnerships supporting SMB working capital needs, plus regulatory compliance cost trajectories tied to evolving AI legislation.

Valuation considerations must account for this durable growth blend underpinned by sustainable recurring revenues amplified by platform synergies enhancing lifetime customer value.

Capital Allocation Excellence: Dividends, Buybacks, and Balance Sheet Strength

Intuit demonstrates disciplined capital allocation consistent with large-cap technology sector norms coupled with prudent risk management frameworks ensuring capital efficiency aligned to shareholder interests [[F1]], [[S10]], [[S13]]. For FY2025 the company returned approximately $4 billion through dividends ($1.19 billion) and share repurchases ($2.77 billion), reflecting an emphasis on returning excess capital while maintaining flexibility for strategic investments [[F1]].

Operating cash flows totaled $6.21 billion supporting these payout levels comfortably alongside productive reinvestment into R&D projects primarily focused on AI innovations.

The reported return on equity stands near 19.6%, denoting efficient use of equity capital backed by steady net income growth against expanding shareholder equity base ($19.7 billion at FY25 end) [[F1]].

Liquidity remains robust with over $2.94 billion in cash & equivalents complemented by access to multiple unsecured revolving credit facilities aggregating several billions facilitating working capital maneuvers including seasonal refund financing programs distinctively associated with TurboTax offerings [[S4]], [[S5]], [[S7]], [[S8]]. The current ratio exceeding 1.3 further testifies financial stability.

On debt covenants front Intuit complies fully with stipulated EBITDA leverage ratios ensuring no material restrictions risk disruption enabling continuous opportunistic capital deployment amid varying economic cycles [[S19]].

Navigating Regulatory and Cybersecurity Challenges in Financial Software

Operating within highly regulated financial software sectors exposes Intuit to mounting compliance demands encompassing data privacy laws, licensing regulations for lending/payment products, anti-fraud mandates alongside nascent AI-specific legislative frameworks such as the EU Artificial Intelligence Act enforced starting August 2024 [[S12]].

These regulations necessitate elevated expenditures on internal governance protocols integrating transparency, fairness assessments for AI model outputs plus rigorous vulnerability remediation practices strengthening cybersecurity postures indispensable in safeguarding customer trust.

The company's proactive approach includes continuous collaboration with government agencies for industry-wide anti-fraud initiatives striving for preemptive mitigation of fraud schemes targeting tax preparation customers as well as enterprise clients leveraging QuickBooks ecosystem features addressing cybersecurity threats dynamically through advanced machine learning detection mechanisms [[S17]], [[S20]].

While these represent inherent operational risks potentially inflating costs or constraining product flexibility they concurrently enhance competitive barriers fostering loyal user bases reliant on compliant trustworthy platforms.

Intuit’s Competitive Moat: Brand, Scale, Data, and Ecosystem Effects

Intuit’s fortified market position stems from its internationally recognized trusted brand strongly associated with core products QuickBooks (business finance) TurboTax (consumer tax prep) Mailchimp (marketing automation), collectively constituting an interconnected SaaS ecosystem delivering end-to-end financial management solutions across business lifecycle stages [[F1]].

Scale affords unparalleled data network effects feeding proprietary AI models improving predictive accuracy of automated recommendations elevating user experiences uniquely accessible only via aggregated transaction histories proprietary accounting data sets or extensive consumer tax filings aggregated securely.

Integration across segments generates significant cross-selling opportunities augmenting average revenue per user coupled with high switching costs since migrating away entails considerable setup costs plus loss of integrated functionalities—classic ecosystem lock-in dynamics pursued commonly among leading platform-based software vendors.

These attributes create durable entry barriers deterring new entrants facing formidable challenges replicating both breadth/depth without substantial investments over sustained time horizons.

This analysis synthesizes SEC filings ([F1],[S#]) alongside recent market commentary ([N#]) without offering investment advice or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments