Kinetik Holdings’ 2025 Growth Stalled by Capital Intensity and Permian Concentration Risks

Kinetik Holdings leverages integrated midstream infrastructure in the Permian Basin but faces headwinds from geographic concentration and elevated capex.

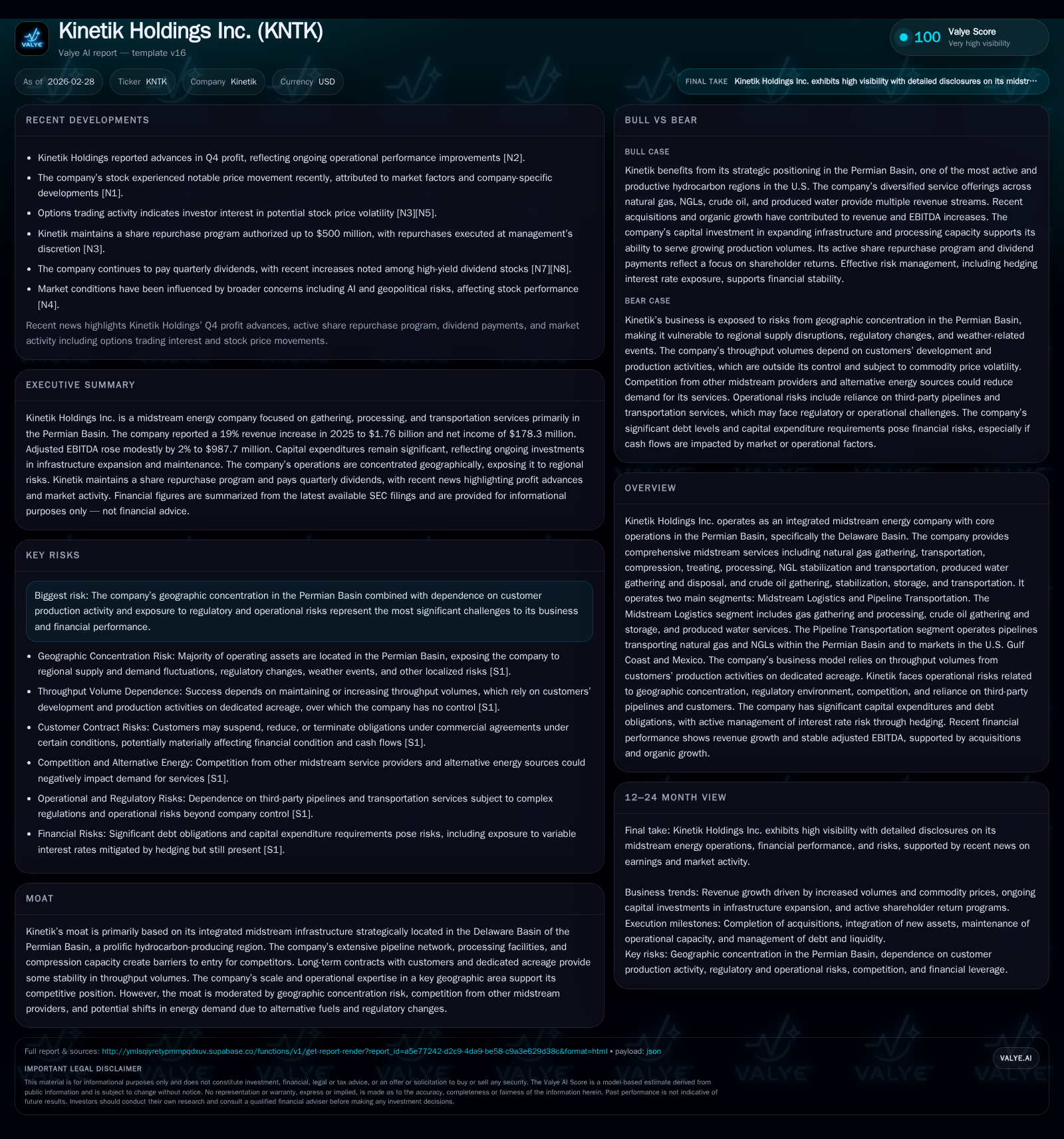

Kinetik Holdings Inc. operates midstream energy assets primarily in the Delaware Basin of the Permian Basin, offering a full suite of gathering, processing, and transportation services. The company reported 19% revenue growth in 2025, driven by higher volumes and commodity prices, yet operating income declined by 8% due to increased operating expenses and depreciation. Capital expenditures nearly doubled as Kinetik invested heavily in pipeline expansions and processing capacity, notably the Kings Landing Processing Complex. The company’s future hinges on sustaining throughput amid natural production declines and managing risks tied to heavy Permian concentration and regulatory factors. Liquidity remains solid with ample borrowing capacity and active share repurchases, but returns show strain given elevated net liabilities.

Company Overview

Kinetik Holdings Inc. stands as an integrated midstream energy company deeply rooted in the Delaware Basin portion of the prolific Permian Basin. Its business model centers on comprehensive midstream services encompassing natural gas gathering, transportation, compression, treating, processing, along with NGL stabilization and transport; plus crude oil gathering, storage, stabilization and transport; produced water gathering and disposal also feature prominently [S1].

Operations are bifurcated into two key segments: Midstream Logistics — covering gas gathering & processing, crude oil services, water management — and Pipeline Transportation — managing pipeline systems for natural gas and NGL movements within the Permian reach extending to U.S. Gulf Coast markets and Mexico [S1]. This integrated footprint provides significant presence enabling scale advantages and potential customer lock-in but il-lustrates a pronounced geographic concentration risk [S1][S26].

Historical Performance

Kinetik’s financial trajectory demonstrates steady top-line expansion against variable profitability [F1]. Revenues grew from approximately $135.8 million at fiscal year-end (FY) 2019 to about $160.6 million by FY2021 (latest multi-year data available), reflecting incremental asset additions and higher commodity-linked product sales volumes.

More recent annual figures for FY2025 spotlight revenue reaching $1.76 billion, up roughly 8.2% year-over-year compared to FY2024 [F1]. This uplift chiefly stems from increased commodity-related product revenues (+23%) driven by heightened NGLs, condensate volumes sold, and stronger realized natural gas residue prices alongside service revenue gains (+9%) fueled by expanded gas gathering fees linked to volumetric growth [S22].

Historical performance (annual)

| FY | CFO ($mm) | OpInc ($mm) | Capex ($mm) |

|---|---|---|---|

| 2025 | 604 | 165 | 492 |

| 2024 | 637 | 179 | 264 |

| 2023 | 584 | 159 | 313 |

| 2022 | 613 | 150 | 206 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 194 | 176 | 112 |

| 2024 | 175 | 0 | 374 |

| 2023 | 81 | 6 | 272 |

| 2022 | 39 | 407 |

Source: SEC companyfacts cache [F1].

Operating income declined modestly (approx -8%) despite revenue growth due mainly to rising operating expenses (+38%) including facilities maintenance, labor costs, as well as increased depreciation reflecting asset additions [F1][S22]. Net income showed a disproportionate jump largely attributable to non-recurring gains from divestitures—principally a $415 million gain from the sale of equity interests in EPIC pipelines [S22][F1]. The huge YOY net income variation reflects this one-time gain rather than underlying operational improvement.

Operating cash flow shrank slightly (-5%) while capital expenditures nearly doubled year-on-year as Kinetik invested heavily into expansions such as its Kings Landing Processing Complex that added over 200 MMcf/d of processing capacity along with associated Acid Gas Injection (AGI) projects targeted for completion by end-2026 [S24][S25]. These investments highlight an aggressive capex stance designed to sustain long-term volumes within their concentrated regional footprint.

Future Growth Prospects

Growth outlook rests fundamentally on Kinetik’s ability to maintain or boost throughput volumes amid natural production declines common with hydrocarbon wells [S26]. Expansion via acquisition has played a recent role—e.g., Barilla Draw Acquisition ($175.5 million cash consideration securing multi-stream gathering opportunities) underscores inorganic growth strategies alongside organic capacity build-out at Kings Landing processing site completed late September 2025 [S24][S26].

The Delaware Basin remains one of the U.S.’s richest unconventional basins but concentration risk is material: regulatory hurdles like water restrictions or prorationing; weather impacts like drought; or upstream producer decisions around drilling activity influence throughput volume directly [S26][S13]. Moreover, competitive pressures emerge from alternate midstream providers or developing proprietary pipelines by producers themselves affecting customer retention and pricing power [S23].

Commodity price volatility indirectly pressures demand for midstream services—lower oil/gas prices can dampen drilling activity negatively impacting throughput volumes—while regulatory developments around emissions controls create both cost implications and operational adjustments [S13][S21].

Capital expenditure plans anticipate moderation around $450–510 million range for 2026 yet remain focused heavily on New Mexico expansions capitalizing on early-mover advantages in ECCC Pipeline completion plus Phase I AGI project at Kings Landing to handle increasing sour gas levels safely [S19][S24].

Forecasts / Milestones / Expectations

While explicit forward guidance is limited in public filings outside forecasted capex ranges for the coming year ($450–510 million), key milestones include:

- Full commercial operation of Phase I Acid Gas Injection system at Kings Landing anticipated by year-end 2026 [S24]

- Continuation of expansion into New Mexico low/high-pressure gathering networks capitalizing on emerging growth corridors [S24]

- Monitoring declaration updates or amendments regarding dividend policy contingent upon earnings and capital needs [S8]

Investors will keenly watch throughput metrics tied to producers’ drilling/completion activities on dedicated acreage amid fluctuating commodity prices that drive corporate capex decisions upstream—a principal volume driver for Kinetik.

Returns / Capital Allocation

The capital allocation strategy balances continued infrastructure investment against cash returned to shareholders via dividends and repurchases.

- Dividends paid totaled about $193.7 million in FY2025 up modestly from prior years consistent with policy of quarterly distributions declared based on earnings availability and financial health [F1][S10].

- Stock buybacks accelerated substantially with $176 million spent during FY2025 under an expanded Board-approved repurchase program allowing up to $500 million aggregate purchases; this reduces share count while signaling confidence though constrained somewhat by applicable excise taxes on buybacks per IRS rules [F1][S11][S20].

- Operating cash flow was approximately $604 million yet capital spending consumed nearly $492 million leaving positive but narrow free cash flow (~$112 million), which requires careful management given elevated leverage levels from sizeable outstanding debts totaling multiple billions across fixed notes & variable credit facilities [F1][S4][S6].

Equity position remains negative nearing -$565 million partly reflecting leveraged financing strategies typical in midstream sectors deploying large-scale assets financed through senior notes & credit agreements maturing between 2028–2030; interest expense rose moderately due to rising borrowing costs though partially mitigated through swaps [F1][S9]. ROE is currently negative (~-31%) when calculated crudely due to negative equity base but operational profitability is evident albeit pressured.

Risks Summary

The core risks revolve around:

- Heavy geographic concentration makes Kinetik susceptible to region-specific disruptions including regulatory constraints on production volumes or infrastructure siting delays related to permits or environmental contingencies [S13][S26]

- Dependency on third-party producers’ drilling pace creates volume unpredictability impacting throughput-linked revenue streams; commodity price swings drive such upstream activity levels unfavorably occasionally [S13][S21]

- Increasing competition both within traditional midstream players expanding footprint as well as alternative fuel trends indirectly affecting long-term energy demand profiles introducing market risks [S23]

- Elevated capital intensity necessitates financing dependence while interest rate volatility could increase debt service cost influencing free cash flow availability for dividends/buybacks [S9]

- Environmental and legal compliances impose ongoing operating cost pressures plus contingent liabilities though current reserves seem manageable relative to operations [S13][S17][S24]

Conclusion

Kinetik Holdings’ integrated midstream platform anchored in the Delaware Basin positions it well operationally within one of North America’s premier hydrocarbon basins. However, its concentrated footprint coupled with ramped-up capital spending pressure margins despite strong revenue growth sustained primarily through volume expansions supported by upstream producer activity.

Near-term growth hinges critically on successful deployment of expansion projects like Kings Landing complex enhancements alongside maintaining throughput via customer development programs within dedicated acreage zones—all while navigating evolving regulatory landscapes and market competition.

Capital structure shows resilience via ample liquidity ($1.22 billion borrowing headroom as of end-2025), paired with a balanced approach toward shareholder returns via dividends plus aggressive stock buybacks under controlled tax considerations.

Returns face headwinds reflecting heavy reinvestment phase balanced against earnings generated—operational cash flows are sound but stretched by capital intensity.[F1]

For stakeholders monitoring Kinetik going forward, key indicators include upstream production trends affecting throughput volumes; completion timelines for AGI project phases; management’s ability to optimize capital allocation amid macroeconomic volatility; and any shifts in regional regulatory environment potentially influencing operations.

This report synthesizes information derived from Kinetik Holdings Inc.’s publicly filed SEC disclosures including its latest Form 10-K for fiscal year ended December 31, 2025,[F1],[S#] alongside relevant market news articles.[N#] It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments