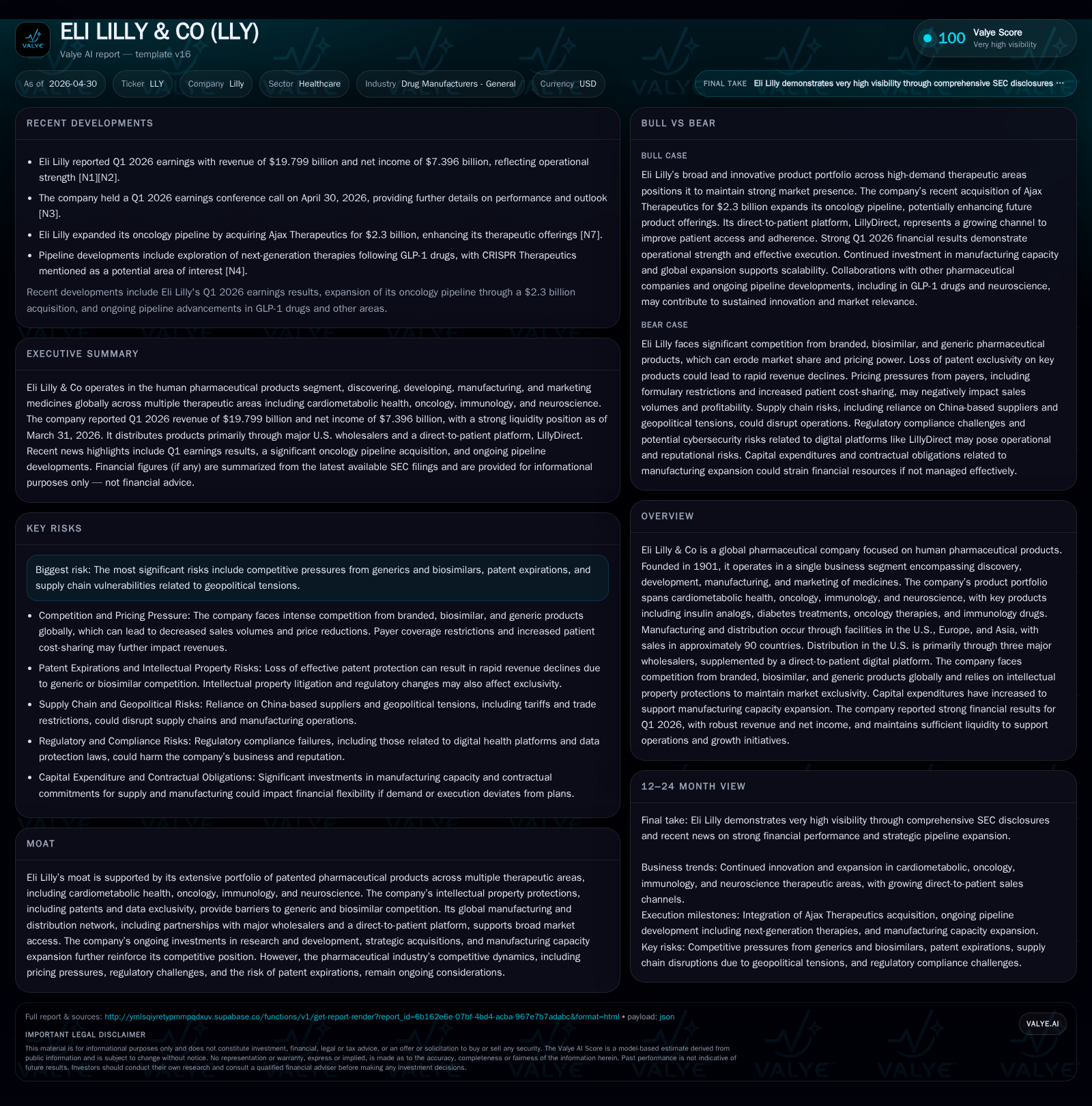

Eli Lilly’s Growth Strengthened by Pipeline Advances and Manufacturing Expansion Despite Pricing Pressures

Q1 2026 results reflect robust momentum in cardiometabolic and oncology franchises, underpinned by strategic R&D investments and capacity scaling.

Eli Lilly's latest quarterly filing highlights sustained top-line growth driven mainly by volume increases in flagship products like Mounjaro and Zepbound, complemented by ongoing expansion in its oncology and immunology portfolios. The company continues heavy capital expenditure on manufacturing infrastructure to meet growing demand, while navigating persistent pricing pressures and patent cliff risks. Pipeline progression includes multiple late-stage trials across cardiometabolic, oncology, and neuroscience areas, underpinning the firm's long-term growth strategy. Operational execution focuses on global distribution efficiency with a multichannel approach including major wholesalers and a direct-to-patient digital platform.

Recent Operating Update

Eli Lilly reported its first quarter results for 2026 in the Form 10-Q filed on April 30, marking steady operational momentum following a year of notable revenue acceleration. Management’s discussion emphasizes continued volume-driven growth from key products such as Mounjaro (tirzepatide) and Zepbound—both glucagon-like peptide-1 (GLP-1) receptor agonists with expanding indications for diabetes and obesity treatment [S2]. This volume growth has partially offset downward pressure from lower realized prices amid intensified payer negotiations and generic competition.

Capital expenditures intensified markedly in recent years, reaching $7.8 billion in 2025 compared to $5.1 billion the prior year, as Lilly invests heavily in global manufacturing capacity upgrades to support both current blockbuster drugs and an expansive clinical pipeline [S26]. The ongoing augmentation of production capabilities aligns with management’s strategic goal of ensuring reliable supply amidst growing demand for cardiometabolic therapies.

Additionally, Eli Lilly recently finalized its $2.3 billion acquisition of Ajax Therapeutics, bolstering its position in oncology with promising targeted therapies now entering pivotal late-stage trials [N11]. This acquisition complements Lilly’s established oncology franchise which continues to gain market share alongside key immunology assets.

Business Model Analysis

Eli Lilly operates through a single business segment centered on human pharmaceutical products encompassing research, development, manufacturing, marketing, and distribution worldwide [S1]. Its revenue generation derives from sales of patented medicines across multiple therapeutic clusters: cardiometabolic health (including diabetes), oncology, immunology, and neuroscience.

Who pays? The primary payers include healthcare providers reimbursed by insurance entities or government programs. Revenue hinges critically on a combination of prescription volumes driven by physician adoption, pricing negotiated with payers (both public and private), reimbursement policies, and usage intensity per patient treated.

Lilly commands durable pricing power on many branded drugs due to patent exclusivity safeguarded by intellectual property rights and data exclusivity frameworks. However, this pricing power is tempered by rising biosimilar competition post-patent expiration—and the company acknowledges ongoing downward price pressures for mature molecules [S1].

Volume growth is currently fueled by newly approved medicines like Mounjaro for type 2 diabetes and obesity indications as well as expanding label extensions leveraged via phase 3 advancements for products such as orforglipron and retatrutide [S1]. Product mix improvements support margin expansion alongside systemic cost controls despite increasing R&D spend.

Manufacturing is largely conducted internally through state-of-the-art facilities across the U.S., Europe, and Asia complemented by contract manufacturing agreements strategically designed to balance fixed costs while remaining flexible to scale production based on demand shifts [S26]. Distribution combines three major U.S.-based wholesalers with an emerging direct-to-patient digital platform that enhances market reach and patient engagement—a competitive differentiator especially relevant in chronic disease therapies.

Industry Structure and Competitive Position

Eli Lilly competes in a highly concentrated global pharmaceutical industry marked by fierce rivalry among large-cap innovators including Pfizer, Merck, AbbVie, Roche, Novartis, Amgen, and others. The industry dynamics are shaped by:

- High barriers to entry due to costly R&D cycles and complex regulatory approvals.

- Dependence on a pipeline capable of replacing revenues lost through patent expirations.

- Increasing scrutiny over drug pricing by governments leading to policy interventions affecting reimbursement.

- Growing presence of biosimilars eroding exclusivity windows post-patent expiry.

Lilly’s competitive moat rests on four pillars:

- An extensive portfolio of patented specialty biopharmaceuticals spanning several fast-growing therapeutic sectors.

- Intellectual property protections that confine generic/biosimilar entrants notably in cardiometabolic treatments like insulin analogs.

- Broad geographic footprint covering ~90 countries enabling diversified revenue streams.

- Ongoing investments into next-generation molecules augmented by acquisitive strategies (e.g., Ajax Therapeutics acquisition).

Nevertheless, sector risks are notable including price erosion trends observed industry-wide plus legal/regulatory uncertainties around pricing practices currently investigated or litigated [S11][S12]. While the innovation pipeline remains strong structurally supporting the firm’s future market position, execution risks persist particularly around approvals timelines and payer acceptance.

Growth Drivers

Pipeline Expansion & Label Extensions

Lilly’s pipeline exemplifies an aggressive diversification strategy aiming at structurally expanding addressable markets:

- Numerous phase 3 trials underway targeting expanded cardiometabolic conditions beyond type 2 diabetes: obesity comorbidities like obstructive sleep apnea (OSA), hepatic steatosis (MAFLD), peripheral artery disease; rare conditions also targeted via biologics like muvalaplin [S1].

- Immunology candidates such as mirikizumab (approved) and lebrikizumab (phase 3) offer further potential revenue diversification into inflammatory bowel diseases and allergic disorders.

- Neuroscience focus includes Alzheimer’s therapies like donanemab now approved across multiple regions with further early-stage programs targeting alcohol use disorder etc. Oncology pipeline is enhanced through breakthrough therapy designations accelerating novel agents for KRAS-mutant lung cancers [S1][N11].

Manufacturing Capacity & Supply Chain Investment

Active investment in manufacturing infrastructure supports sustainability amid rising demand volumes:

- Commitment to multi-billion dollar capex drives capacity expansion globally.

- Contract manufacturing flexibility aims at mitigating supply chain disruptions while controlling fixed-cost leverage.

- Investment ensures faster scale-up potential post-launch enhancing time-to-market responsiveness [S26].

Strategic Acquisitions & Collaborations

Acquisition of Ajax Therapeutics enriches oncology offerings placing Lilly among leaders developing targeted KRAS inhibitors—critical given substantial unmet need in certain advanced cancers [N11]. Ongoing collaborations support innovation without sole reliance on organic discovery mitigating pipeline risk exposure.

Risks / Watchpoints / Growth Constraints

Pricing Pressure & Reimbursement Environment

Despite strong product demand growth volumes sustain downward pressure on realized prices due to payers’ negotiating leverage plus intensified scrutiny from policy makers on drug pricing fairness [S1][S27]. Public programs represent substantial revenue share imposing compulsory rebates restricting effective prices especially within U.S.

Patent Expirations & Biosimilar Incursion

Lilly faces medium-term threats as patents expire or transition out some legacy products rendering them vulnerable to generic/biosimilar substitution diluting revenue base over time if replacements do not keep pace [S1].

Regulatory & Litigation Exposure

Ongoing investigations related to pricing practices (notably insulin pricing) plus patent litigations add uncertainty to expense outlook potentially impacting reputation or financial results [S11][S12]. Regulatory hurdles inherent to pharma development could delay approvals or limit market label breadth influencing commercial return assumptions.

Supply Chain & Geopolitical Risks

Manufacturing spread across multiple continents balances risk but remains exposed to geopolitical tensions or tariffs that could disrupt supply flows or increase raw material costs unpredictably [S1].

What to Watch Next

Key upcoming milestones informing near-term trajectory include:

- Progress reports from several phase 3 cardiovascular outcome trials assessing tirzepatide derivatives’ broader indications like heart failure or renal outcomes [S1].

- Regulatory submission decisions pending for insulin efsitora alfa across regions impacting next-gen diabetes portfolio expansion [S1].

- Execution developments on manufacturing capacity expansion with updates on new facility commissioning or contract manufacturing scalability [S26].

- Legal developments especially regarding ongoing 340B program litigation involving government investigations into pricing practices [S8][S12].

- Market uptake metrics for recently launched products such as pirtobrutinib in hematologic cancers serving as bellwethers of commercial execution strength [N2].

- Monitor updated guidance or management commentary integrating recent Q1 earnings beat reinforced by volume gains despite price headwinds [N5][N14].

Financial Profile (Selected Latest Snapshot)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $5.3bn | |

| 2026-03-31 | ||

| Current assets | $54.8bn | |

| 2026-03-31 | ||

| Current liabilities | $36.6bn | |

| 2026-03-31 | ||

| Current ratio | 1.5x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD Billions) | Period Ended |

|---|---|---|

| Cash & Equivalents | $5.28 | |

| 2026-03-31 | ||

| Total Debt | $29.47 | |

| 2024-12-31 | ||

| Current Assets | $54.83 | |

| 2026-03-31 | ||

| Current Liabilities | $36.63 | |

| 2026-03-31 | ||

| Current Ratio | 1.5 | Calculated |

| Net Debt* | ~$24.19 | Approximate |

| *Net Debt = Total Debt minus Cash & Equivalents [F1] |

Liquidity remains solid with cash reserves sufficient relative to short-term liabilities providing operational flexibility amidst capital-intensive projects including R&D scaling and manufacturing buildout [S2][F1]. Long-term debt maturity profile coupled with proactive refinancing has positioned Eli Lilly with manageable leverage supporting balanced capital allocation emphasizing share buybacks ($10.9 billion remaining authorization post-$4.1B repurchased in 2025) alongside dividends raised recently to $6.92 per annum subject to quarterly payments commenced in early 2026 [S1].

This analysis is based solely on publicly available disclosures without any stock recommendations or price targets implied.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments