Lion Group Holding Ltd Charts Path After Latest Exclusivity Deal

The April 2026 exclusivity agreement marks a strategic pivot for Lion Group Holding Ltd to stabilize operations amid financial challenges.

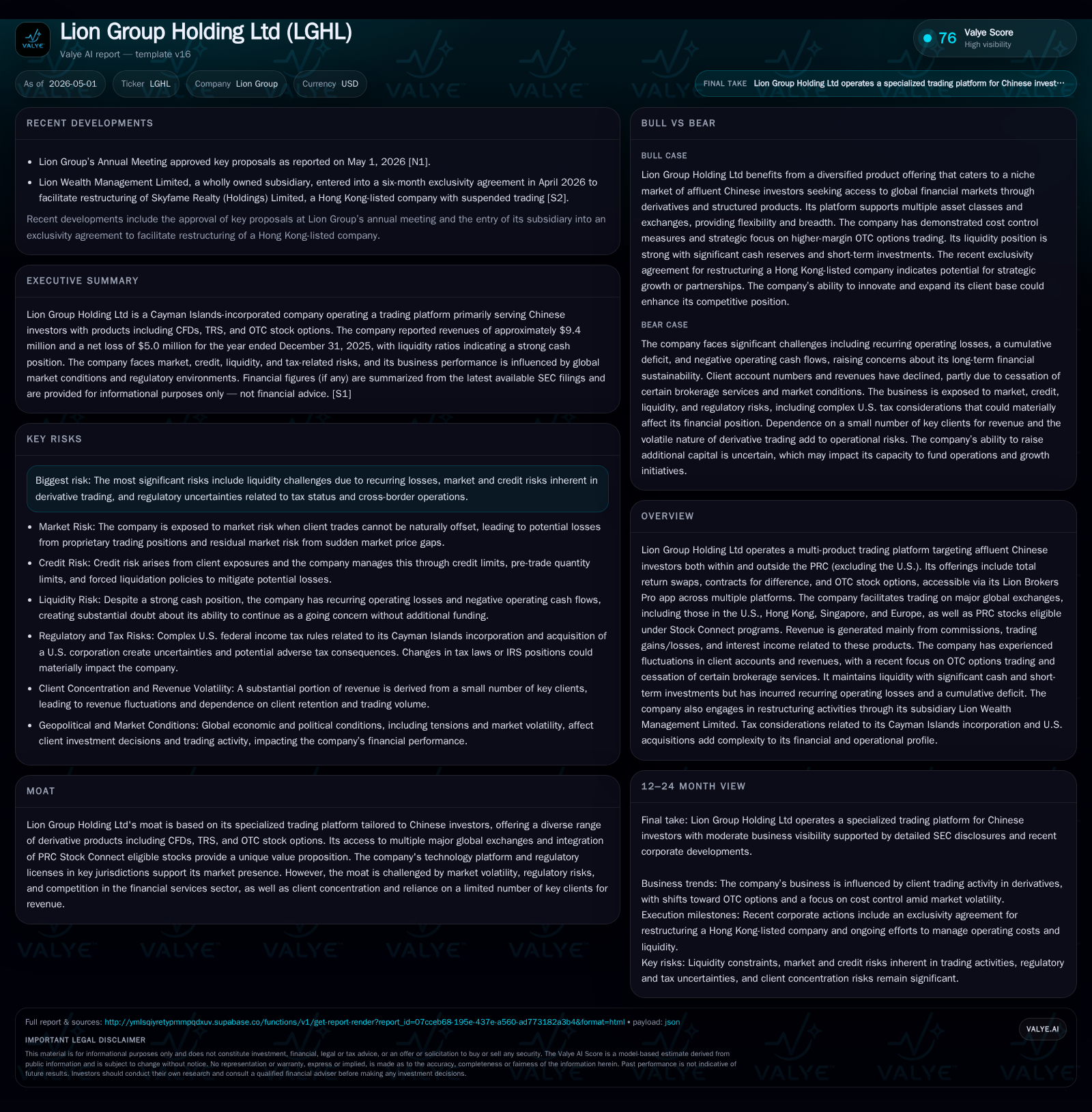

Lion Group Holding Ltd recently entered into a six-month exclusivity agreement to facilitate restructuring of Skyfame Realty, signaling a diversification effort beyond its core derivative trading platform focused on affluent Chinese investors. The company’s multi-product offering—including TRS, CFDs, and OTC stock options—targets clients operating across global exchanges and Stock Connect eligible PRC stocks. Despite meaningful liquidity supported by over $20 million in cash and a strong current ratio, recurring operating losses and client concentration pressure remain key near-term risks. Technology investments and the growing OTC options business serve as potential growth drivers, while regulatory uncertainties and high operating leverage temper outlook clarity.

April 2026 Exclusivity Agreement: Implications and Context

In April 2026, Lion Wealth Management Limited (a wholly owned subsidiary of Lion Group Holding Ltd) signed an exclusivity agreement with Skyfame Realty (Holdings) Limited (currently in liquidation) that grants a six-month window to lead restructuring efforts aimed at resuming Skyfame's public trading on the Hong Kong Stock Exchange [S2]. This move signals LGHL's proactive approach to diversify beyond its core derivatives platform amid ongoing operating losses and liquidity concerns. The agreement includes provision of an unsecured credit facility up to approximately $3 million USD to cover professional fees related to Skyfame’s restructuring [S1], illustrating LGHL's willingness to deploy capital strategically outside traditional financial product offerings.

This structural pivot could either stabilize or complicate LGHL’s financial profile depending on the outcomes of these restructuring negotiations. With Skyfame’s shares suspended due to liquidation proceedings, LGHL is exposed to operational risk outside its primary brokerage business but sees potential synergies or asset acquisition opportunities that could complement its broader wealth management ecosystem.

Business Model and Product Suite Adapted to Affluent Chinese Traders

LGHL’s revenue mechanics hinge predominantly on commission income, bid-offer spreads, trading profits/losses, and interest income generated via derivatives offerings including total return swaps (TRS), contracts for difference (CFD), and over-the-counter (OTC) stock options tailored specifically for well-educated affluent Chinese investors both inside and outside mainland China—excluding U.S. clients [S1]. These products are delivered across multiple digital platforms through the Lion Brokers Pro app on iOS, Android, Mac, and PC.

A key strategic strength is LGHL’s pan-global access enabling client trades on major futures exchanges such as CME, SGX, HKFE, Eurex; stock exchanges including NYSE, Nasdaq, HKSE; plus PRC shares via Shanghai-Hong Kong and Shenzhen-Hong Kong Stock Connect programs. This broad exchange connectivity supplements diversified product mix offerings spanning equities, futures, forex, ETFs, warrants alongside callable bull/bear contracts [S1].

Revenue trends track closely with client transaction volumes and account counts. However, total revenue-generating accounts have declined steadily from 2,443 at end-2023 to 2,172 at end-2025 due to exits from less profitable futures brokerage services and insurance products [S1][S12]. CFD trading remains prominent though volatile given concentrated reliance on few key clients historically responsible for outsized revenue portions.

Competitive Positioning Within Retail Derivatives Trading

Within the highly competitive retail derivatives space catering primarily to the Chinese investor segment overseas, LGHL carves out a niche through its specialized derivative instruments combined with comprehensive jurisdictional licenses in Cayman Islands and Hong Kong markets [S1]. Its integrated product suite coupled with robust trading app delivery enhances switching costs with customers favoring seamless multi-platform accessibility.

However, competitive pressures manifest acutely through market volatility impacts—geopolitical tensions such as Ukraine-Russia conflicts or Israel-Iran war have repeatedly triggered global market circuit breakers affecting client risk appetite—and regulatory uncertainty around cross-border tax treatments poses ongoing risk [S1]. Client concentration amplifies revenue earnings volatility as historic dependency on a narrow investor cohort restricts scalability absent broad user base expansion.

Futures brokerage exit reflects strategic realignment towards higher-margin derivative products like OTC stock options where LGHL experienced a swing from losses to positive trading income in 2025 [$33 million improvement] [S18]. However, sustaining differentiation depends heavily on maintaining technological leadership and compliance rigor within shifting regulatory regimes.

Technology Investments as a Differentiator in User Experience

Technology expenditures constitute a core pillar of LGHL’s competitive strategy. Communication and technology expenses rose modestly ($3.4M in 2024 vs $3.1M prior year), driven by AI integration within OTC option algorithms along with launch of multi-currency trading accounts [S1]. These investments aim at intelligent order routing capabilities and enhanced user experience across devices.

Continuous product innovation is critical given the inherently fast-evolving retail derivatives ecosystem where users seek algorithmic execution efficiency paired with broad asset accessibility. This may help mitigate declines encountered in segments like futures brokerage by repositioning the platform as an AI-enabled wealth management hub serving geographically distributed clients.

Growth Catalysts: OTC Options Focus and Restructuring Opportunities

The ramp-up of OTC stock options represents a key growth vector with LGHL shifting resources away from legacy businesses towards this high-potential vertical [S18]. Improved performance here materially influenced revenue increase in 2025 despite overall account count softness.

Simultaneously, the exclusive restructuring mandate for Skyfame offers potential ancillary benefits if successful integration unlocks new asset channels or capital flows that feed back into LGHL’s core operations [S2][S11].

Success metrics relevant to monitoring growth include client acquisition rates post-restructuring effort implementation alongside transaction volume trends on OTC products. A recovery in total active accounts beyond recent declines would be pivotal for scaling revenues sustainably.

Risks and Constraints: Liquidity, Client Concentration, and Regulatory Exposure

Despite holding $20.1 million cash & equivalents as of Dec-31-2025 backed by a healthy current ratio of 4.11 [F1], recurring operating losses (~$5 million net loss in 2025) generate substantial doubt around going concern viability per management disclosures [S3]. Negative cash flow from operating activities (-$3.5 million) exacerbates liquidity pressure despite recent financing uplifts via convertible debentures totaling $25 million raised since mid-2023 [S6][S16].

Client concentration risk persists because a small number of users historically contribute disproportionate revenue share making earnings susceptible to their variable activity [S1]. Regulatory risks surround U.S. federal income tax complexities for non-U.S entities owning U.S.-listed securities alongside cross-border restrictions impacting business model fluidity [S1].

Furthermore, dependence on continuous ability to raise capital at acceptable terms introduces execution risk that could materially impair operating capacity if market conditions deteriorate or investor sentiment wanes.

Key Near-Term Milestones and Watchpoints

Primary focus will be on developments related to Skyfame restructuring outcomes ahead of October 2026 exclusivity expiration [S2], assessing whether this diversification strategy yields tangible operational or financial stability.

Quarterly reports thereafter should be scrutinized for user account trajectory changes as well as OTC options transaction volumes confirming the success of pivotal growth initiatives [S12]. Technology deployment progressions including AI algorithm effectiveness also warrant attention as indicators of sustained competitive edge.

Lastly, liquidity trend monitoring is essential given sizable cash burn juxtaposed against funding needs articulated in filings emphasizing potential capital raises or related party support necessity [S3][F1].

Latest Financial Snapshot: Liquidity and Operating Results

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $20mm | |

| 2025-12-31 | ||

| Current assets | $26mm | |

| 2025-12-31 | ||

| Current liabilities | $6mm | |

| 2025-12-31 | ||

| Current ratio | 4.11x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Period End |

|---|---|---|

| Revenue | 9,390,651 | |

| 2025-12-31 | ||

| Net Income | -4,956,735 | |

| 2025-12-31 | ||

| Cash & Equivalents | 20,124,296 | |

| 2025-12-31 | ||

| Current Ratio | 4.11 | |

| 2025-12-31 |

The fiscal year ended December 31, 2025 saw LGHL generate revenue of approximately $9.4 million with a net loss nearing $5 million due largely to operational expenses exceeding trading income despite gains in OTC options segments [F1][S17][S18]. Meanwhile, financial strength is evidenced by robust cash reserves exceeding $20 million alongside minimal debt exposure contributing to a strong short-term liquidity position embodied by a current ratio above four times liabilities [F1].

Still, management expressed concern regarding sufficiency of existing liquidity sources relative to planned working capital demands over the next twelve months pointing toward heightened refinancing or capital infusion risks ahead [S3]. This underscores the importance of executing growth strategies while controlling cost structures diligently.

Disclaimer: This analysis is provided solely for informational purposes based on publicly available SEC filings as of May 2026. It does not constitute investment advice or recommendations regarding securities of Lion Group Holding Ltd or any other entity. Readers should conduct their own independent due diligence before making any decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments