INNO Holdings’ Strategic Shift to Recycled Electronics Tests Operational Resilience

INNO Holdings faces operational and financial challenges amid its pivot to recycled electronics and blockchain-enabled B2B marketplace ambitions.

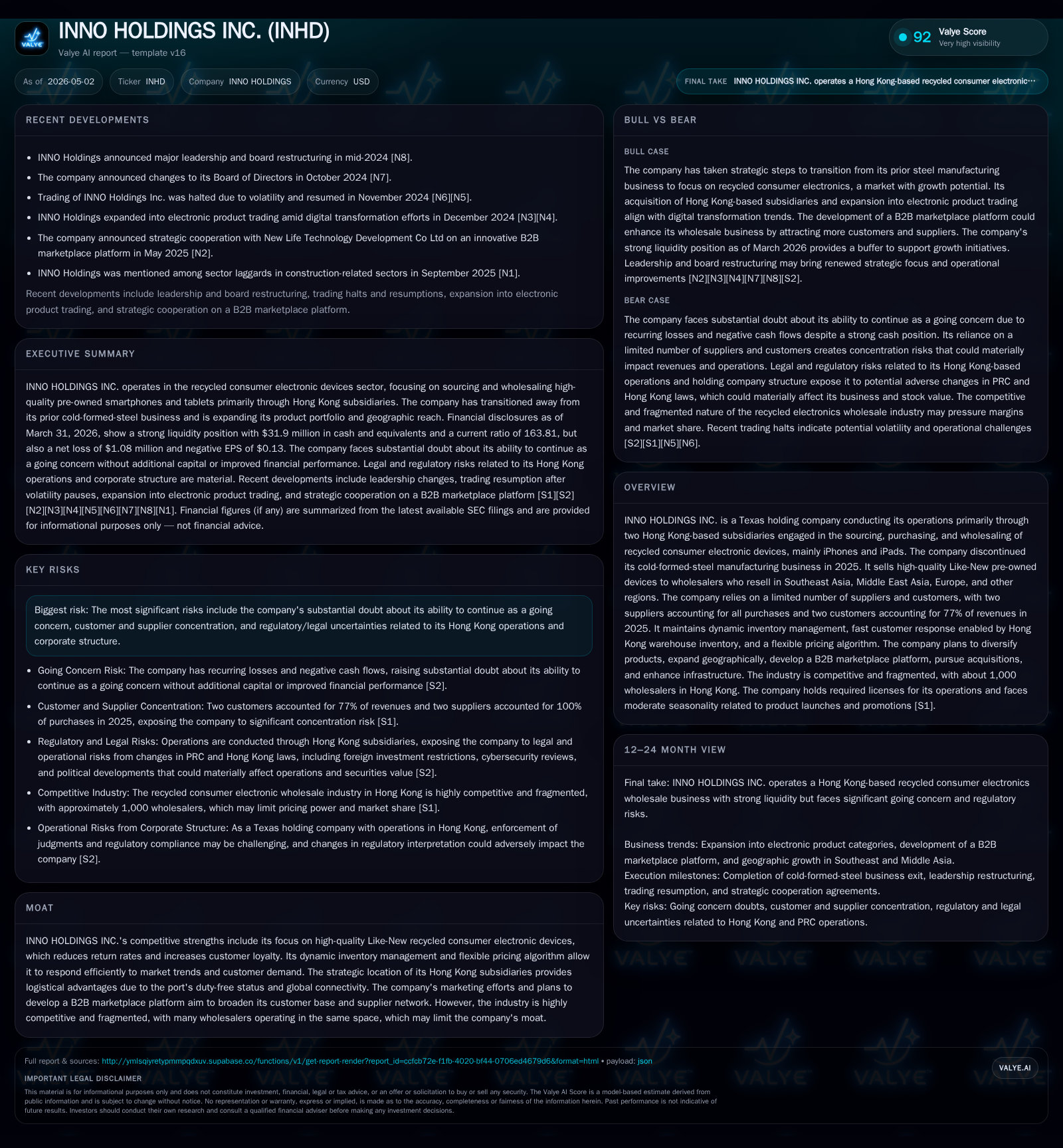

INNO Holdings continues transitioning from its discontinued steel manufacturing business to recycled consumer electronics, focusing on high-quality Like-New iPhones and iPads sold wholesale primarily through Hong Kong-based subsidiaries. The latest quarterly filing reveals substantial doubt about the company’s ability to continue as a going concern despite solid cash reserves, driven by recurring operational losses and concentrated supplier-customer dependencies. Growth plans hinge on launching a blockchain-powered B2B marketplace platform with MEGABYTE Solutions Limited alongside product diversification and acquisitions. Regulatory risks tied to Hong Kong operations and ownership structure, coupled with concentrated counterparties, pose notable execution challenges.

Q1 2026 Operating Results Reveal Transition Challenges and Capital Needs

In its most recent 10-Q filing dated May 1, 2026, INNO Holdings confirmed continuing operational difficulties despite significant liquidity resources. The company reported an operating loss nearing $4.4 million for the quarter ended September 30, 2025, along with a net loss exceeding $7 million over the same period [F1]. While these figures precede the current quarter’s end by six months, no subsequent improvement has been disclosed suggesting these trends persist into early 2026 [S2].

Despite holding a healthy cash balance of nearly $32 million as of March 31, 2026, INNO’s filings articulate substantial doubt about its ability to continue as a going concern without additional capital inflows or improved operational performance [S2]. This dichotomy underscores the company’s acute need for either operational turnaround or successful capital-raising efforts within the coming year.

Notably, total debt remains negligible at under $100 thousand based on the latest available data from December 2024 [F1], implying that leverage constraints are minimal. The balance sheet therefore supports near-term solvency but does not alleviate concerns driven by persistent negative earnings and uncertain revenue growth visibility.

Business Model Focused on High-Quality ‘Like-New’ Pre-Owned Consumer Devices

INNO Holdings shifted away entirely from its previous cold-formed-steel manufacturing business during Q2 2025 to concentrate solely on the sourcing and wholesaling of recycled consumer electronics — principally Like-New condition iPhones and iPads purchased from a small set of suppliers [S1]. These devices undergo quality vetting aimed at minimizing returns due to cosmetic or functional degradation, which is critical in fostering customer loyalty among wholesale clients scattered across Southeast Asia, Middle East Asia, Europe, and other markets.

Revenue derives exclusively from sales to wholesale customers who then resell these devices further down their distribution chains. Product concentration remains heavily skewed toward Apple’s mobile products with aspirations disclosed to gradually broaden offerings into MacBooks, smartwatches, headphones, and other ancillary electronic accessories [S1]. However, this diversification remains nascent.

This business model hinges fundamentally on maintaining high standards for product quality (‘Like-New’ grading), effective inventory management via Hong Kong warehouses enabling rapid customer responses, and leveraging dynamic pricing algorithms sensitive to market conditions. The company's revenue mechanics are volume-driven through device throughput but highly vulnerable to supplier quality consistency given the dual-supplier concentration.

Competitive Environment: Supply Chain Concentration and Geographic Niches

The recycled consumer electronics wholesaling industry is notably fragmented with many small players competing on quality assurance standards and supply chain agility. INNO’s reliance on just two suppliers accounting for all purchases — coupled with two customers generating over three-quarters of revenues — presents both an operational risk due to counterparty concentration and a potential negotiating weakness [S1][S2].

Nonetheless, INNO attempts to mitigate these risks through intense supplier vetting procedures requiring background checks before onboarding new vendors. The strategic placement of its operating subsidiaries in Hong Kong provides key logistics advantages such as duty-free port facilities and connectivity enabling fast turnarounds critical in this fast-moving product market segment.

Regulatory complexity arising from operating in Hong Kong under China's evolving legal-regulatory regime adds another layer of strategic risk. Political tensions may affect trading freedoms or capital movement restrictions related to cross-border transactions involving U.S.-listed holding companies like INNO. This geopolitical overlay complicates long-term planning amid growing external scrutiny.

Innovation and Growth Drivers: B2B Marketplace, Product Diversification, and Acquisitions

Looking forward, INNO aims to leverage digital innovation via a recently announced strategic partnership with MEGABYTE Solutions Limited to jointly develop a blockchain-powered decentralized B2B marketplace platform targeted at cross-border wholesale trade in recycled electronics [S1]. This Web3 integration is designed to enhance transactional transparency, reduce intermediary costs, and improve supply-demand matching efficiency.

While promising as a technological differentiator within an otherwise commoditized sector, this initiative is still very early stage with considerable execution uncertainty. Regulatory hurdles around blockchain use cases in cross-jurisdictional commerce add further complexity. Additionally, adopting such emerging technology demands expertise that INNO acknowledges it is currently developing.

Parallel growth strategies involve expanding product categories beyond phones/tablets into laptops (e.g., MacBooks) and various electronic accessories — an effort aimed at capturing more wallet share per customer while broadening supplier relationships.

Moreover, INNO signals intentions toward targeted acquisitions especially in underpenetrated regions such as North and South America where it currently lacks distribution presence. Acquisitions could accelerate scale benefits but require capital deployment which intersects materially with the company’s funding challenges.

Risk Factors: Going Concern Doubts, Supplier-Customer Concentration, Geographic Regulatory Exposure

The filings consistently underscore 'substantial doubt' about continuing as a going concern given recurring losses alongside operating cash flow deficits [S2][S17]. Without successfully raising new capital or materially improving business economics through growth or margin expansion initiatives (e.g., B2B platform adoption), ongoing viability is severely constrained.

Supplier-customer concentration amplifies revenue volatility risk since losing or renegotiating terms unfavorably with either large suppliers or customers could materially impact sales volume or cost base. While supplier vetting reduces quality risks somewhat, diversity remains limited.

Operating primarily through Hong Kong subsidiaries exposes INNO to regulatory risks stemming from PRC government policy shifts potentially impacting overseas listings by China-connected firms. Recent SEC guidance combined with China’s tightening of foreign-investment rules may add compliance costs or restrict capital mobility between U.S.-based holding entities and Hong Kong operations.

Additional litigation or foreign corruption-related risks exist under statutes like the Foreign Corrupt Practices Act given business conducted across jurisdictions prone to governance challenges [S18].

Upcoming Milestones: Execution on Platform Launch, Customer Diversification, and Capital Raising

Key near-term catalyst events involve:

- Commercial rollout progress of the blockchain-powered B2B marketplace platform developed jointly with MEGABYTE Solutions — critical for validating technology-enabled scaling claims;

- Expansion efforts underway to onboard new suppliers beyond current dual-vendor reliance aiming to reduce concentration risk;

- Broadening customer roster beyond top two buyers representing majority revenue percentage;

- Execution success of announced acquisition targets particularly in Americas region providing meaningful incremental scale;

- Securing necessary financing either via equity or debt markets sufficient to fund working capital needs over ensuing twelve months without diluting shareholder value excessively;

- Management changes including recent board director appointment reflecting governance dynamics potentially influencing strategic direction stability [S3].

Each milestone carries substantial execution risk given limited operating history post-pivot combined with volatile macroeconomic themes affecting discretionary electronics spending globally.

Latest Financial Snapshot Highlights Solid Liquidity Supported by Conservative Leverage

INNO's balance sheet as of the latest quarter shows robust liquidity characterized by an outsized current ratio (~163.8), reflecting significant cash buffers relative to minimal short-term liabilities [F1]. Total debt remains minimal at approximately $98 thousand as of December 2024 [F1], supporting a low leverage profile.

However, persistent negative profitability reflects ongoing structural challenges in scaling operations profitably within its core recycled electronics wholesale niche combined with pressures related to customer concentration constraints.

--

Disclaimer: This analysis is based solely on publicly available SEC filings dated through May 2026 alongside companyfacts numerical data. It avoids investment recommendations or projections beyond grounded evidence. The information presented does not constitute financial advice or endorsements.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments