Extreme Networks Reports Earnings Beat Despite Liquidity Tightness

Strong Q3 performance highlights operational resilience amid below-par liquidity ratios and ongoing market pressures.

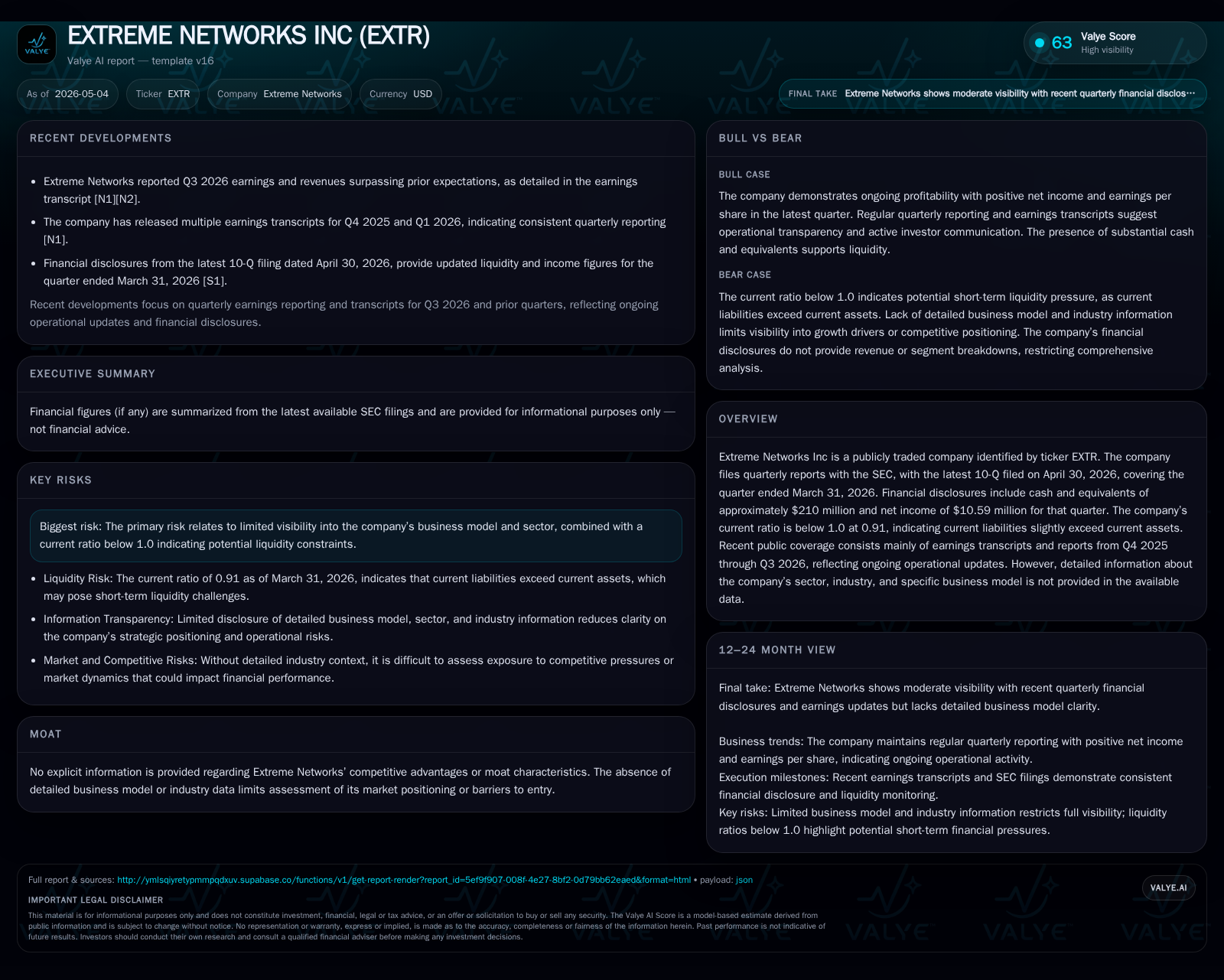

In its latest quarter ending March 31, 2026, Extreme Networks exceeded revenue and earnings expectations, registering a net income of approximately $10.59 million. Despite this operating success, the company faces liquidity challenges, with a current ratio below 1.0 highlighting working capital constraints. Extreme’s business model centers on enterprise networking solutions blending hardware and cloud-managed software offerings that respond to evolving customer demands for scalable, AI-ready infrastructure. Competitive pressures and capital structure risks remain notable but are partially offset by strategic growth drivers linked to software subscriptions and network modernization trends.

Q3 2026 Operating Highlights and Strategic Implications

Extreme Networks Inc reported its latest quarter results for the period ended March 31, 2026, through an SEC Form 10-Q filed on April 30, 2026 [S2], complemented by an earnings announcement dated April 29, 2026 [S3]. The quarter showcased revenue exceeding consensus estimates alongside a positive net income figure approximating $10.59 million [F1]. This profit outcome marks an improvement directionally compared to prior periods despite the company operating with a tight liquidity profile — evidenced by a current ratio of 0.91 as of quarter-end [F1], reflecting that current liabilities ($593 million) slightly outstrip current assets ($542 million).

Additionally, Extreme held robust cash and equivalents on hand amounting to roughly $210 million [F1], which provides some buffer against working capital demands but does not fully alleviate near-term liquidity concerns. These findings portray a company navigating operational execution effectively while confronting balance-sheet strain typical for capital-intensive technology firms competing in dynamic markets.

Business Model Overview: Technology Focus and Customer Value

Extreme Networks operates as a provider of enterprise networking equipment and associated software solutions designed to meet the increasingly complex demands of modern digital infrastructures. While explicit segment details are limited in the filings examined, external sources including recent earnings call transcripts suggest revenue generation stems primarily from three interlinked streams: physical networking hardware (switches, routers), recurring software revenue largely tied to cloud-managed and subscription-based offerings, and professional services centered on deployment and support [N1][N2].

This blend allows the company to monetize both one-time product sales and build steadier recurring revenue through intelligent network management platforms that incorporate automation capabilities—a crucial differentiator as enterprises transition toward AI-ready environments necessitating more fluid and scalable network architecture.

Customer value is created by delivering integrated solutions that simplify network operations while enabling real-time analytics and enhanced security features within an increasingly software-defined landscape. Such positioning aims to mitigate risks associated with commoditized hardware pricing by embedding higher-margin software ecosystems that foster stickier customer relationships.

Competitive Positioning within Network Infrastructure Industry

Extreme Networks contends in a highly competitive industry featuring entrenched incumbents offering broad portfolios ranging from basic Ethernet switching products to sophisticated cloud-native networking platforms. Within this arena, pricing power typically varies; hardware components often compete on price due to commoditization pressures whereas differentiated software stacks providing automation, analytics, or enhanced security can command premium valuations.

Though no explicit moat characteristics were outlined in regulatory disclosures [S2], market commentary implies Extreme leverages channel partnerships alongside direct sales efforts to penetrate enterprise segments responsive to turnkey cloud-managed networking solutions [N2]. This dual approach aids in balancing scale with targeted customer engagement.

Regulatory impact appears minimal based on available data but adoption cycles are influenced by macroeconomic IT spend patterns which can introduce cyclical fluctuations particularly affecting capital expenditures related to upgrades or expansions.

Growth Catalysts and Expanding Market Demand

Key growth vectors for Extreme integrate structural demand trends such as rising AI application deployment necessitating networks capable of higher throughput, lower latency, and enhanced automation frameworks [N1]. The proliferation of software-defined networking (SDN) also creates upsell potential within existing accounts as traditional hardware setups migrate toward more flexible virtualized architectures.

These market dynamics translate into tangible operational KPIs like increased bookings volumes in AI-centric sectors or expanding deal sizes incorporating multi-year subscription contracts referenced in investor calls [N1][S2]. Continued product innovation aligned with these secular trends underpins revenue growth aspirations while promoting margin enhancement via a shift from purely transactional hardware sales towards higher-margin software-enabled services.

Liquidity Constraints and Financial Risks

Moreover, disclosed total debt stood near $180 million as last recorded ending June 30, 2025 [F1], which while structured at previous reporting cycles suggests leverage remains appreciable within the capital base. Close management of receivables collections cycles alongside prudent expense control will be critical mitigants against these financial risks as Extreme balances growth investment against operational sustainability [S2][S3].

Key Upcoming Milestones and Performance Indicators

Stakeholders should focus on several key forthcoming checkpoints to gauge Extreme’s trajectory:

- The next quarterly earnings release will signal whether momentum behind growth initiatives persists within potentially challenging industry spending cycles.

- New product introductions targeting AI-optimized network segments could serve as inflection points for expanding addressable market share.

- Monitoring backlog developments or booking rates through investor communications provides early signals about customer demand strength or softness amid an unsettled IT spending environment.

- Analyst updates post earnings may revise guidance or sentiment based on emerging data points regarding execution or market conditions [N11][S4].

Success across these markers will validate strategic bets on software-led transformations counterbalancing cyclical hardware adjacencies.

Latest Financial Position Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $210mm | |

| 2026-03-31 | ||

| Current assets | $542mm | |

| 2026-03-31 | ||

| Current liabilities | $593mm | |

| 2026-03-31 | ||

| Current ratio | 0.91x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Period End |

|---|---|---|

| Cash & Equivalents | $210,113,000 | |

| 2026-03-31 | ||

| Current Assets | $541,802,000 | |

| 2026-03-31 | ||

| Current Liabilities | $593,265,000 | |

| 2026-03-31 | ||

| Current Ratio | 0.91 | |

| 2026-03-31 | ||

| Net Income (Q3) | $10,590,000 | Q3 2026 |

This snapshot illustrates the juxtaposition between solid cash levels aiding near-term liquidity with overall working capital tightness reflected in the sub-industry-standard current ratio figure supporting earlier analysis points [F1][S2].

Disclaimer: This analysis is based solely on publicly available SEC filings and related news sources as of early May 2026. It does not constitute investment advice or recommendations regarding any securities mentioned. Readers should conduct their own due diligence when considering insights derived herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments