Tutor Perini Advances Infrastructure Backlog Amid Strong Q1 Execution

Tutor Perini’s first quarter results demonstrate momentum in backlog growth and operational performance, supporting its leadership in large-scale construction sectors.

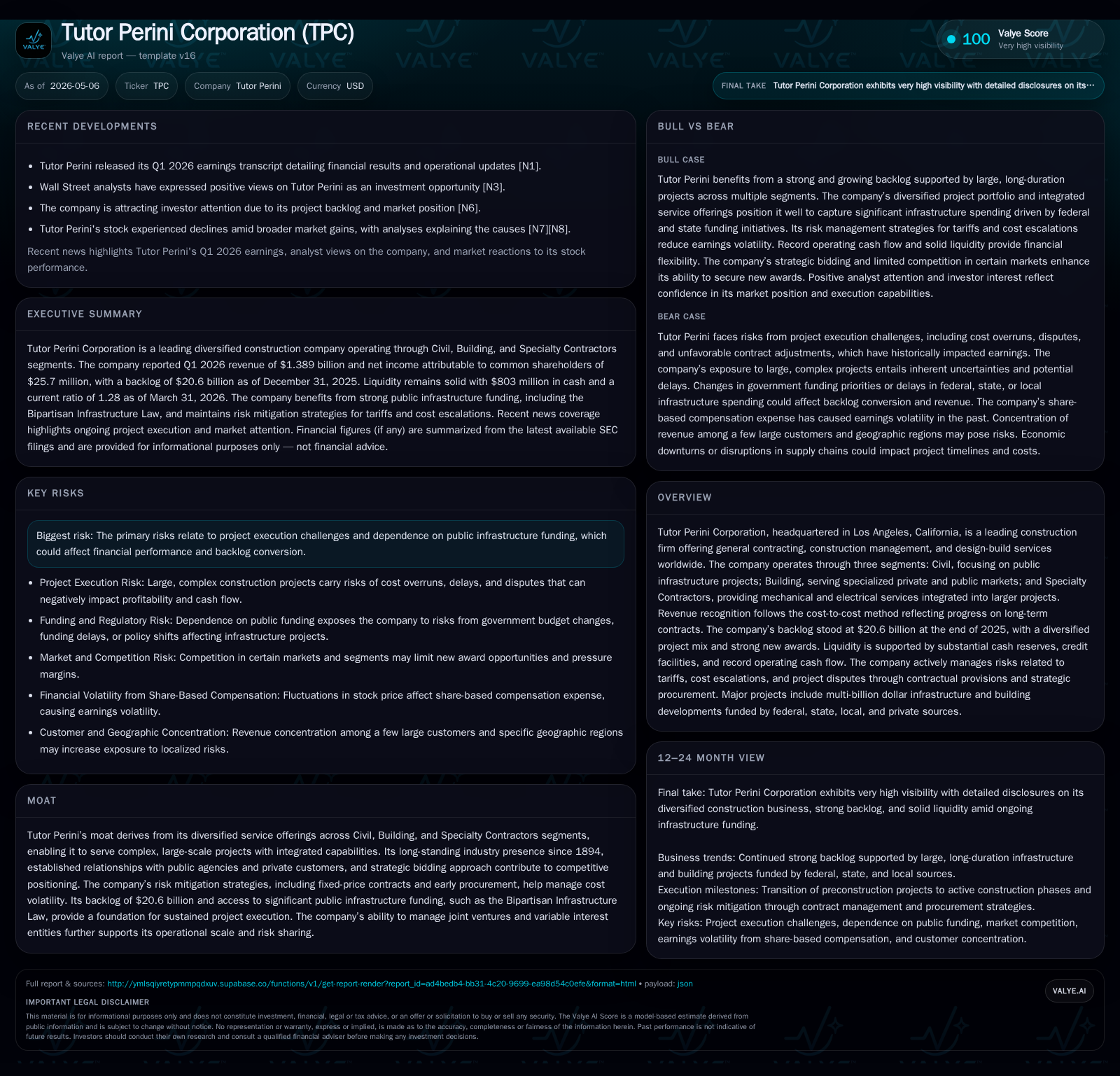

Tutor Perini Corporation reported strong revenue growth of $1.39 billion in Q1 2026, supported by a backlog of $20.6 billion. Operating income remained solid amid ongoing risk and cost pressures, validating its integrated Civil, Building, and Specialty Contractors segments. The company leverages diversified project mix, public infrastructure funding, and robust liquidity to underpin future growth while managing execution risks tied to legal settlements and contract complexity. Key indicators to watch include backlog conversions, claim resolutions, and cash flow trends.

Latest Quarterly Performance Highlights

Tutor Perini Corporation generated Q1 2026 revenue of approximately $1.39 billion, up from $1.25 billion in Q1 2025, marking an 11.5% increase reflecting increased project completions and ongoing progress in higher-margin contracts [S2]. Gross profit expanded to about $154.6 million from $134.4 million year-over-year. Income from construction operations contracted modestly to $59.2 million (Q1 2025: $65.3 million), impacted by higher general & administrative expenses which included share-based compensation volatility linked to the company’s stock performance [S2]. Net income attributable to Tutor Perini stood at nearly $25.7 million versus $28.0 million previously.

Backlog reached a robust $20.6 billion as of December 31, 2025—a key foundation for sustained revenue visibility driven primarily by public infrastructure projects supported by recent federal legislation [S1], [S2]. Operational cash flow conversion remains strong with cash & equivalents rising to approximately $803 million, underscoring liquidity strength complemented by a conservative total debt level around $425 million [F1]. Net debt is effectively negative given cash holdings exceed debt balances by roughly $378 million [F1]. The current ratio at 1.28 reflects comfortable short-term asset coverage [F1].

Notably, the improvement in operating results coincides with ongoing resolution of legacy disputes and settlements that continue to affect earnings visibility but are expected to stabilize over time as change orders mature [S24], [N2]. This operating update signals Tutor Perini's ability to balance ramping newer projects while managing legacy risk exposure.

Overview of Tutor Perini’s Business Model and Service Offerings

Tutor Perini operates through three core segments: Civil, Building, and Specialty Contractors [S1], [S17]. The Civil segment focuses on public works infrastructure—highways, bridges, tunnels, mass transit systems—services characterized by large-value contracts often backed by state/federal funding streams. The Building segment delivers complex structures for private clients and government entities across hospitality, healthcare, detention facilities, biotech labs, and commercial offices.

Specialty Contractors consist of electrical, mechanical (HVAC/plumbing), fire protection systems spanning both civil and building projects. This integration affords tighter scheduling control and cost management advantages that differentiate their general contracting approach versus competitors who subcontract these specialties externally.

Revenue recognition employs the cost-to-cost method appropriate for long-term contracts whereby earnings reflect progression towards completion rather than invoicing milestones alone [S1]. Such methodology smooths earnings albeit introduces exposure to scope changes or claims affecting estimate at completion revisions.

This business model benefits from diversification across public/private sectors and service lines allowing Tutor Perini to bid competitively on complex multi-disciplinary jobs where integrated execution capability acts as a moat.[S1]

Competitive Position Within the Construction Industry

Established since 1894 via predecessor firms merged into today’s Tutor Perini in 2008 [S1], the company boasts entrenched market stature bolstered by deep relationships with state/local agencies integral to public project procurements. Its ability to perform in highly regulated environments dealing with union labor forces, permitting processes, and compliance with federal tariff considerations sets high barriers for new entrants.

Sector-native challenges include labor skill shortages affecting capacity utilization nationally alongside supply chain volatility for critical materials such as steel and concrete that influence pricing power dynamics [S24]. Tutor Perini addresses these with refined procurement strategies including early ordering that hedges inflation effects while contractual frameworks transfer some risk via fixed-price or escalation clauses.

Its joint venture arrangements help allocate execution risk on mega-projects while expanding bid competitiveness without disproportionate capital commitments [S17]. Pricing power appears moderately durable given project complexity combined with reputational leverage but margin compression risk persists amid inflationary cycles.

Competitors often specialize narrowly within civil or building segments; Tutor Perini’s cross-segment integration creates differentiation allowing holistic project capture especially in government-funded infrastructure where scale matters significantly.

Key Growth Drivers: Backlog and Infrastructure Spending

The company’s backlog grew substantially during 2025 benefiting materially from the Bipartisan Infrastructure Law fueling federal/state investments in transportation networks [S1], [N6]. Backlog composition includes sizable awards in mass transit (up sharply Q1 2026), bridges (incremental gains), water management expansions plus military facility projects delivering steady revenue streams in the Civil segment alone ($697.7 million in Q1) [S17].

Private sector recovery across healthcare facilities and detention centers boosts Building segment revenue alongside specialized offerings in biotech/pharmaceutical markets lending higher-margin potential [S17].

Strategic use of early procurement limits cost volatility while sustained success negotiating change orders improves realized margins over time—particularly important given prior years’ residual project adjustments now reversing positively [S24]. Expansion of Specialty Contractors within internal contracts enhances efficiency delivery enabling better control over schedules and costs across multifaceted jobs.

Demand drivers appear largely structural given nationwide infrastructure modernization imperatives combined with demographic trends supporting healthcare/commercial construction needs.

Risks and Operational Challenges Impacting Performance

Execution risk remains a focal concern evident from historical legal disputes culminating in multi-million-dollar settlements related mainly to complex tunneling machinery damages litigation resolved recently with no material impact on Q1 results but highlighting project intricacies faced [S24]. Such disputes contribute episodic earnings volatility requiring reserve recognition impacting margin stability.

Additional threats stem from reliance on continued appropriation of public funds; budget fluctuations could delay project starts or reduce backlog replenishment rates.[S24] Escalating input costs pose margin pressure particularly if inflation outpaces escalation remedies embedded within contracts or outlasts procurement hedging strategies.

Regulatory delays in permits or approvals can defer cash flow timing while share-based compensation expense fluctuations linked to market valuations inject financial statement noise complicating performance evaluation [S2], [S24].

Management mitigates several risks through fixed-price agreements combined with proactive claim management minimizing surprise exposures yet residual uncertainty warrants close monitoring.[N1]

Looking Ahead: Milestones and Market Signals to Monitor

Key near-term markers include quarterly backlog updates reflecting conversion velocity especially concerning large-scale transport/highway contracts where billings pace directly correlates with revenue recognition acceleration.[S2] Watching incremental awards wins amid competitive bid environment will clarify trajectory under tightening labor/material conditions.[N1]

Cash flow trends weekly aligned with dispute claim negotiations serve as liquidity barometers given past volatility periods.[S3] Management commentary during upcoming earnings calls will be vital for insight into anticipated margin progression post-share-based compensation normalization.[N2]

Furthermore, resolution outcomes from pending smaller legal matters or regulatory changes impacting contract structuring will shape medium-term profitability outlooks.[S24] Observers should also track programmatic enhancements in internal project controls driven by Specialty Contractors integration purportedly improving project delivery benchmarks.[N7]

Latest Financial Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $803mm | |

| 2026-03-31 | ||

| Total debt | $425mm | |

| 2025-12-31 | ||

| Net debt | $-378mm | |

| 2025-12-31 | ||

| Current assets | $4.1bn | |

| 2026-03-31 | ||

| Current liabilities | $3.2bn | |

| 2026-03-31 | ||

| Current ratio | 1.28x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

This snapshot affirms Tutor Perini’s stable capital structure featuring significant cash balances relative to debt maturities alongside solid operating profitability sustaining liquidity robustness essential for executing sizable multi-year projects.

Disclaimer: This analysis is based strictly on disclosed SEC filings and news reports as of May 6, 2026; it does not constitute investment advice or recommendations regarding Tutor Perini Corporation's securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments