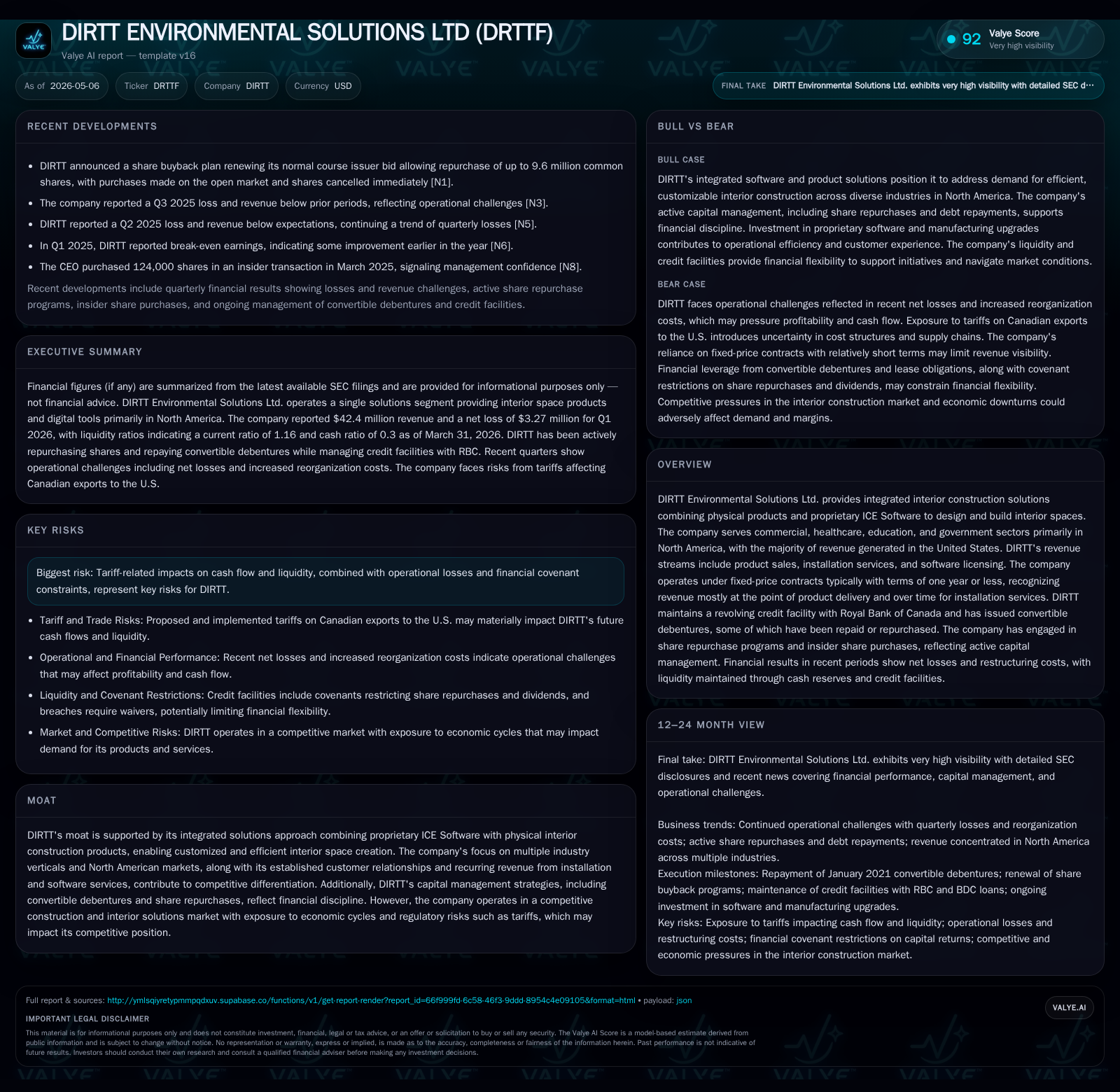

DIRTT Environmental Solutions Tightens Capital Structure While Advancing Integrated Interior Innovation

Recent quarterly actions reveal DIRTT’s focus on debt reduction and share repurchases alongside continued execution of its ICE Software-driven interior construction platform.

In its latest quarterly filing, DIRTT Environmental Solutions completed repayment of its outstanding January 2026 convertible debentures, renewed share repurchase programs, and further optimized its credit facilities. This financial discipline occurs against a backdrop of tariff-related revenue uncertainties impacting cash flow. The company’s integrated model pairing proprietary ICE Software with modular interior products supports customized, fixed-price projects primarily in the North American commercial and healthcare sectors. While tariff risks and litigation challenges persist, DIRTT’s contract structure and software integration create switching costs that underpin growth potential through deeper customer engagement and expanded service offerings.

Recent Quarterly Developments: Capital Management and Operational Update

DIRTT’s May 6, 2026 10-Q reveals a clear push toward strengthening the capital structure through disciplined liability management. The company successfully repaid the outstanding principal and accrued interest on the January Debentures at maturity on January 31, 2026 [S2]. This repayment extinguished approximately C$16.6 million ($12.1 million USD) in principal associated with these debentures, removing a significant near-term debt maturity overhang from the balance sheet [S1][S2]. Concurrently, DIRTT continued its normal course issuer bids (NCIBs), which allow it to repurchase shares and December Debentures on the open market at prevailing prices [S2][S3].

The company also amended its revolving credit facility with Royal Bank of Canada (RBC) during Q1 2026 to integrate a new loan agreement with the Business Development Bank of Canada (BDC), which provides up to C$15 million under favorable terms maturing in 2032 [S8]. At quarter-end March 31, 2026, DIRTT had no drawn amounts against its RBC credit facility but maintained available borrowings of approximately C$14 million ($10.1 million USD), providing a liquidity buffer despite tightened operating cash flows [F1][S8]. Importantly, DIRTT disclosed that tariff-related impacts on Canadian-U.S. trade continue to pose risks that could materially affect future cash flows and liquidity profiles [S2][S3]. These factors underscore why capital preservation measures have taken precedence alongside operational execution.

Business Model: Integrated Solutions with ICE Software Differentiation

DIRTT operates a vertically integrated business combining physical modular interior construction products with proprietary design software known as ICE® Software [S1]. This synergy allows architects, contractors, and clients to conceive highly customized interior spaces translated directly into manufacturing instructions via digital models. Through fixed-price contracts typically spanning a year or less, revenue recognition mainly occurs at product delivery for hardware sales while installation services are recognized over time [S1].

The business model generates revenue through three primary streams—product sales (modular walls, partitions, furniture), installation services customizing those products onsite, and licensing fees for ICE software provided both to external construction partners and end customers [S1][F1]. ICE Software integration creates embedded switching costs by tying client design processes closely to DIRTT’s manufacturing system, facilitating long-term customer retention beyond just component supply. This approach enables scalable customization without sacrificing cost or time certainty—a competitive advantage relative to traditional interior construction methods reliant on manual labor-intensive tasks.

Recurring revenue from installation services also adds margin stability that complements the historically lumpy product order cycle typical in construction markets. The company focuses largely on commercial verticals including healthcare facilities requiring adaptable configurations, educational buildings emphasizing speed of construction, government projects demanding compliance rigor, and general commercial office spaces seeking sustainability credentials [S1][S10].

Competitive Environment: Market Position and Industry Dynamics

DIRTT operates in a niche within the broader interior construction industry characterized by escalating digitization yet still anchored in traditional build methods. Its competitive moat rests on the proprietary ICE Software platform integrated tightly with manufactured physical modules enabling faster turnarounds and precise project costing. This contrasts with legacy competitors offering conventional onsite installations lacking customizable digital-first workflows.

However, the company must navigate cyclical headwinds typical of construction sectors sensitive to economic fluctuations as well as structural challenges posed by regulatory tariffs affecting cross-border supply chains. Tariffs levied on Canadian-made goods exported into the U.S.—DIRTT’s largest revenue market—increase input costs reducing price competitiveness versus domestic manufacturers [S2][S3]. Given most production remains Canadian-based while customer demand centers largely in the U.S., these import duties necessitate close monitoring as incremental cost pressures may compress margins or delay project approvals.

Strategically, DIRTT’s strength lies in serving diverse verticals within North America leveraging digital tools fostering customer intimacy. Market dynamics favor players who can deliver precision-built interiors rapidly with lower waste footprints—a trend correlating with ESG-oriented procurement policies increasingly prevalent among government and healthcare customers.

Growth Drivers: Expansion Opportunities in Target Verticals and Products

Looking ahead, growth for DIRTT stems from multiple levers converging around deepening software adoption tied to hardware deployment [S1][S2]. Increased licensing of ICE Software expands the ecosystem effects as more construction partners integrate toward standardized manufacturing workflows enhancing order volume visibility.

Cross-selling enriched installation services alongside product sales augments overall wallet share per client while smoothing revenue volatility inherent in hardware shipments alone. Enhanced offerings in healthcare segment renovations driven by pandemic-induced modernization needs represent another avenue given stringent infection control requirements necessitating flexible interiors.

Geographically, while DIRTT’s footprint is concentrated largely in the United States—with Canadian sales steady but smaller—continued north-south trade dynamics imply potential channel expansion if tariff barriers ease or supply chain localization shifts arise.

Incremental enhancements in manufacturing technology underpin opportunities for cost reductions enabling competitive price points alongside product innovation such as integrated environmental controls or adaptable partitioning systems supporting evolving workplace trends.

Risks and Constraints: Tariffs, Liquidity, and Legal Proceedings

Critical risks revolve predominantly around external economic factors impacting cash flow sufficiency amidst ongoing tariff uncertainties between Canada and the U.S., as highlighted repeatedly in recent filings [S2][S3]. These tariffs elevate landed cost structures diminishing pricing flexibility.

Although DIRTT shows improvements via debt repayments like extinguishing January Debentures early this year reducing net leverage measured at roughly $2.9 million net debt against $15 million cash at quarter-end [F1], vigilance remains necessary given term maturities approaching end-2026.

Legal litigations—particularly concerning intellectual property claims involving Falkbuilt Ltd.—have shifted jurisdiction from U.S. courts back to Canada following dismissals based on forum non conveniens doctrine. While proceedings remain pending potentially increasing legal costs or management distraction risk, no material developments indicative of financial strain surfaced in the latest quarter [S1][S2].

What to Watch Next: Milestones, Guidance, and Execution Signals

Key upcoming milestones include the release of Q2 2026 operational results expected around August where tariff impact signaling through backlog health metrics will be critical to assess sustained demand resilience [S2][S3]. Monitoring progress on installment services growth alongside indicators such as bookings converts will illuminate execution momentum.

Regulatory developments influencing cross-border trade policy remain a wildcard impacting margin forecasts; any easing could spur profitability improvement via reduced input costs while intensification would warrant re-pricing initiatives or increased lobbying efforts.

Watch also for updates related to ongoing litigation outcomes since extended trials scheduled through early 2026 could influence legal provisions or reshape competitive positioning if judgments impose restrictions.

Finally, corporate finance watchers should track refinements within share repurchase programs or debt refinancing transactions managed under evolving covenant landscapes; these signal management’s confidence level in balancing capital returns vis-à-vis liquidity preservation.

Latest Financial Snapshot: Balance Sheet and Liquidity Focus

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $15mm | |

| 2026-03-31 | ||

| Total debt | $18mm | |

| 2026-03-31 | ||

| Net debt | $3mm | |

| 2026-03-31 | ||

| Current assets | $57mm | |

| 2026-03-31 | ||

| Current liabilities | $49mm | |

| 2026-03-31 | ||

| Current ratio | 1.16x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Period End |

|---|---|---|

| Cash & Equivalents | 14,999,000 | |

| 2026-03-31 | ||

| Total Debt | 17,891,000 | |

| 2026-03-31 | ||

| Net Debt (Approx.) | 2,892,000 | |

| 2026-03-31 | ||

| Current Assets | 57,209,000 | |

| 2026-03-31 | ||

| Current Liabilities | 49,465,000 | |

| 2026-03-31 | ||

| Current Ratio | 1.16 | |

| 2026-03-31 |

This snapshot reflects a modest net leverage profile equivalent to roughly $2.9 million after considering cash balances relative to total debt outstanding approximating $17.9 million including equipment leases fully accounted for [F1]. It portrays DIRTT Environmental Solutions Ltd.’s strategic capital maneuvers coupled with its differentiated integrated interior construction platform amid challenging trade dynamics and industry competition. The company's efforts to manage financial risk while deploying growth initiatives illustrate its attempt to carve sustainable niche advantages within North America's evolving industrialized construction sector.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments