ACRES Commercial Realty Delivers With Merger Strategy and Commercial Mortgage Execution

ACRES Commercial Realty’s latest quarter underscores strategic merger progress and robust commercial mortgage loan operations as key value drivers.

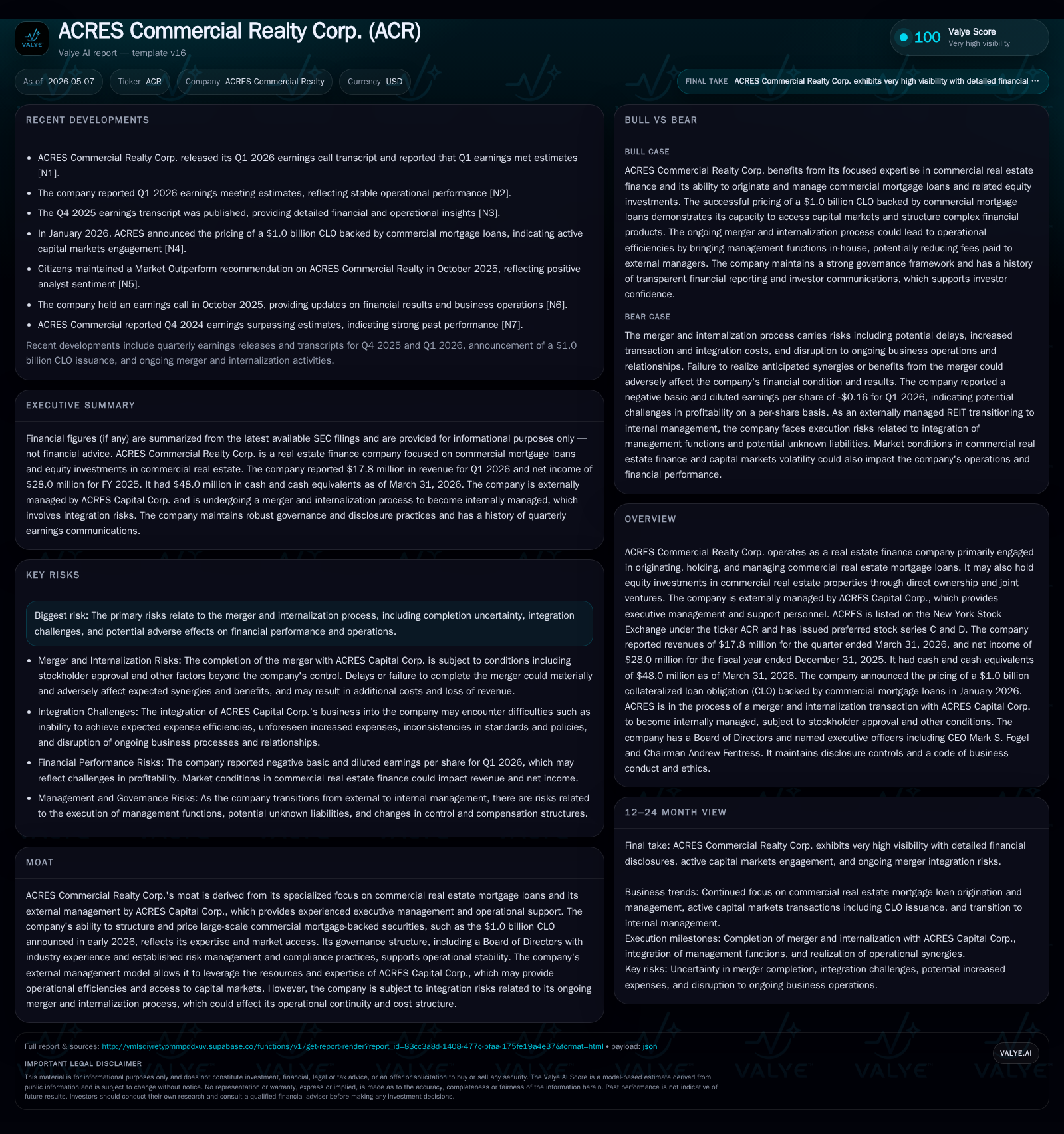

In its first quarter 2026 filing, ACRES Commercial Realty reported sustained commercial mortgage loan revenues alongside a significant $1 billion CLO issuance, reflecting effective capital markets execution. The company is advancing on a transformative merger to internalize management, aiming to capture synergies and streamline operations amid integration risks. ACRES’ business model, centered on originating and holding commercial real estate loans with a complementary equity investment platform, benefits from its external management expertise and CLO market access. Strategic growth hinges on merger completion, increased loan origination volumes, and enhanced securitization capabilities.

Latest Quarterly Update Highlights

ACRES Commercial Realty Corp.'s first quarter of 2026 report (filed May 6) delivers clear evidence of steady commercial real estate mortgage lending performance paired with notable capital markets activity. Revenue was reported at $17.8 million for the quarter ended March 31, 2026 [S2], underscoring resilience in its core loan origination and servicing business.

Central to the recent update is the successful pricing of a $1 billion collateralized loan obligation (CLO) backed by commercial mortgage loans announced in January 2026. This transaction signifies both operational execution strength in sourcing quality loan assets and favorable access to institutional credit markets amid a recovering securitization environment.

Strategically pivotal is the April 29, 2026 announcement of a proposed all-stock merger to acquire ACRES Capital Corp., the company's external manager [S3][N3]. This move to internalize management aims to eliminate fees paid to the third party while consolidating operational control. However, the merger remains subject to customary closing conditions including stockholder approval, presenting an ongoing source of uncertainty [S2]. Recent risk disclosures stress that failure or delay could impair expected synergies and weigh on financial results [S2]. Additionally, substantial legal and advisory expenses related to the transaction have been incurred [S2].

Composition changes in executive leadership accompany these developments with new appointments to managing director roles for capital markets and originations set at closing [S20]. Such reorganization signals intent toward integrating broader responsibilities internally post-merger.

Business Model and Value Proposition

ACRES operates chiefly as a commercial real estate finance company focused on originating, holding, and managing mortgage loans secured by income-producing real estate [S1]. Revenues derive primarily from interest income on mortgage loans as well as fees tied to loan servicing activities. Additionally, ACRES holds some equity investments either directly or through joint ventures enhancing yield opportunities beyond pure debt exposure.

The company’s externally managed structure means ACRES Capital Corp. currently handles executive functions under a management agreement [S1]. Upon completing the planned merger/internalization, ACRES aims to bring these capabilities in-house—removing outside management fees while potentially improving alignment of incentives.

A competitive moat is built around its ability to structure complex commercial mortgage-backed securities such as CLOs—an area demanding deep credit analysis expertise and proven access to institutional investors comfortable with commercial mortgage credit risks. This specialization enables ACRES to drive volume while mitigating funding cost volatility.

Management’s disciplined investment governance includes use of an Investment Committee that reviews transactions exceeding defined thresholds ($50-75 million ranges), reinforcing credit quality controls [S1]. This framework supports loan portfolio integrity critical in cyclical real estate credit markets.

Industry Context and Competitive Positioning

Within the broader CRE financing ecosystem, ACRES participates as a mid-sized originator and holder focusing predominantly on structured lending solutions characterized by detailed underwriting processes suitable for institutional capital deployment [S1].

Macroeconomic conditions impacting CRE debt pricing—including interest rate environments and property market fundamentals—directly influence asset yields achievable by ACRES. Its demonstrated ability to channel originated loans into CLO vehicles offers an advantage in funding diversity compared with lenders reliant on more traditional bank-like balance sheet channels.

Regulatory scrutiny around non-bank CRE lenders continues but has not curtailed CLO demand materially, given their importance in dispersing risk across capital markets. However, any tightening could constrain issuance volumes or investor appetite over time.

Capacity limitations reflect both equity capital availability for direct investments as well as warehouse financing infrastructure underlying loan origination scale. The company’s external management has delivered operational discipline resulting in measured growth trajectories aligning asset quality preservation with expansion ambitions.

Competitively, ACRES faces rivals ranging from other specialty finance REITs to large banks’ CMBS desks; differentiation comes through its focused niche in CRE loan origination packaged into repeatable securitizations offering transparency desirable for CLO tranche investors.

Growth Catalysts and Demand Drivers

Future growth is expected from three synergistic levers:

Loan Origination Expansion: Increasing origination volume under disciplined underwriting can grow core interest income streams. The hiring of a Managing Director for Originations signals commitment to scale this engine post-internalization [S20].

Securitization Activities: Repeat CLO issuances enable recycling capital through bond tranches attracting institutional buyers while retaining servicing fees — leveraging prior success including the $1 billion deal closed early 2026 [S2].

Merger Synergies: Internalizing ACRES Capital Corp.’s operations promises cost savings by terminating external management fees plus operational efficiencies from tighter integration of back-office functions [S3][S2].

Additional growth avenues may come from selective equity investments or joint ventures providing diversification alongside debt holdings. The market backdrop of rising CRE transaction volumes after pandemic disruptions bodes well for incremental demand.

Risks Surrounding Merger Internalization

The merger process presents principal risks:

- Closing Conditionality: Completion depends on stockholder votes plus regulatory approvals which remain uncertainties outside company control [S2][S3]. Delays may increase transactional expenses or erode confidence.

- Integration Complexity: Combining organizations involves reconciling standards, systems, policies, compensation schemes — mismatches could disrupt ongoing operations impacting revenues or expenses negatively [S2].

- Synergy Realization Timing: Expected cost savings may be delayed or less than forecasted due to unforeseen liabilities or operational challenges post-merger.

- Market Sentiment Impact: Merger-related uncertainties can influence share price volatility adversely if perceived execution risks persist.

These factors warrant close monitoring given their outsized influence relative to routine operating risks inherent in CRE lending.

Key Milestones and What to Watch Next

Investors should focus on:

- Stockholder Approval Vote: Critical trigger for consummation of the merger/internalization transaction scheduled following proxy statement distribution [S5][N3].

- Quarterly Earnings Reports: Future filings will shed light on realized synergy capture including reduction in external management fees plus any incremental operating costs tied to integration activities [S2].

- Additional CLO Issuances: New securitization deals would confirm sustained access to capital markets supporting origination throughput expansion.

- Leadership Integration Progress: Execution of appointments announced April 2026 positioning key executives responsible for capital markets and originations reflects preparedness for enlarged internal organization scope [S20].

- Debt Refinancing or Capital Raises: Any moves here could affect liquidity position especially if supporting growth initiatives or managing leverage levels following internalization.

Financial Snapshot and Capital Structure Overview

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $48mm | |

| 2026-03-31 | ||

| Total debt | $1876mm | |

| 2026-03-31 | ||

| Net debt | $1828mm | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026, ACRES held approximately $47.9 million in cash and equivalents against total debt near $1.88 billion yielding net debt around $1.83 billion [F1]. Reported revenues totaled about $17.8 million for Q1 reflecting stable core loan portfolio operations [S2][F1].

This leverage profile aligns with typical CRE finance structures balancing asset-backed borrowing capacity with liquidity buffers necessary for ongoing operations plus investment commitments.

Liquidity adequacy appears sound though will be tested as merger-related payments occur combined with new asset acquisitions or secured warehouse financings for growing originations pipeline.

This analysis focuses entirely on documented filings without conjecture beyond clearly stated facts. Market dynamics impacting ACRES must be judged within credible SEC disclosures considering prevailing economic conditions affecting commercial real estate financing.

Disclaimer: This report is for informational purposes only derived from publicly available SEC filings and does not constitute investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments