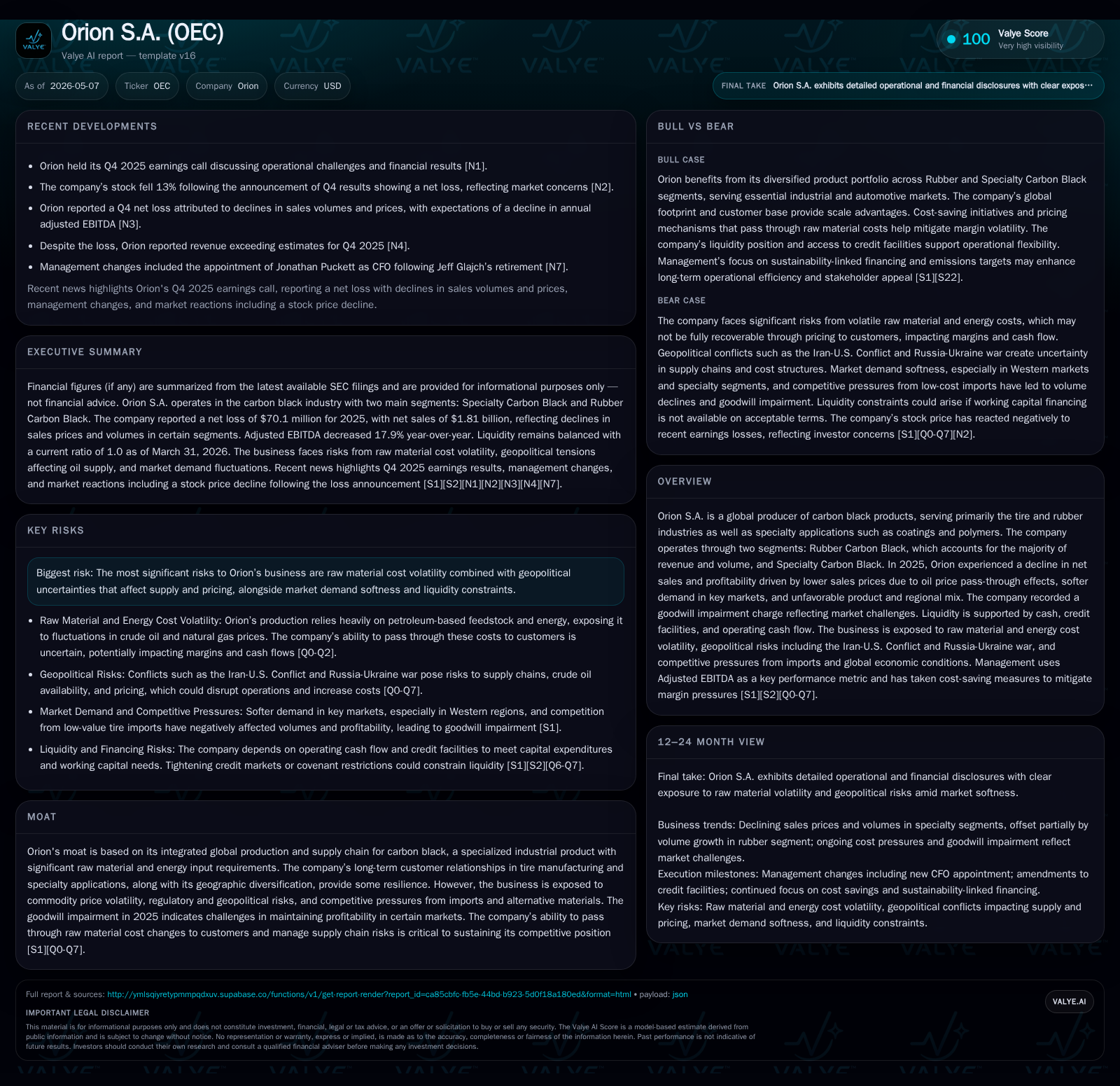

Orion S.A. Confronts Profitability Pressures and Raw Material Volatility in Q1 2026

Orion's Q1 2026 report underscores persistent margin compression despite stable volumes, amid raw material cost swings and geopolitical risks.

In its latest quarterly filing, Orion S.A. reported ongoing headwinds driven by volatile raw material prices and soft demand in specialty segments, which have continued to pressure profitability despite slight volume growth in core products. The company's strategic focus remains on managing supply chain risks, executing cost savings, and navigating geopolitical uncertainties that affect its feedstock sourcing. Competitive pressures from imports and slower industrial end markets further challenge its Specialty Carbon Black segment. Liquidity appears adequate but leverage ratios are elevated, signaling cautious capital management ahead.

Recent Operating Update

Orion S.A.'s first quarter 2026 filing dated May 6, 2026, highlights continued challenges in profitability despite slightly increasing production volumes within its Rubber Carbon Black segment. Management’s discussion points to persistent volatility in raw material costs – especially carbon black oil derived from petroleum – intensified by geopolitical concerns including the Iran-U.S. conflict and Russia-Ukraine war [S2]. These dynamics disrupt feedstock supply chains, complicate cost pass-through mechanisms embedded in supply contracts, and impose margin pressures.

While total volumes modestly increased over the prior year period primarily due to Rubber Carbon Black demand gains, the Specialty Carbon Black segment faced softer industrial markets leading to reduced sales volume and unfavorable product mix effects [S2][S1]. Notably, margins remain compressed as contractual price adjustments lag input cost upticks and customers resist fully reflecting these increases in final prices given competitive import pressures.

The company disclosed a significant goodwill impairment charge of $80.8 million recorded during 2025 due to adverse shifts in trading conditions for both reporting units—underscoring heightened competition from low-cost tire imports from Asia and ongoing portfolio mix challenges underpinned by geopolitical uncertainties impacting trade norms and regulatory regimes [S1].

Business Model

Orion generates revenue primarily through the production and sale of carbon black products leveraging two operational segments: Rubber Carbon Black (the bulk of revenues) serving predominantly tire manufacturers globally, and Specialty Carbon Black addressing niche applications such as coatings and polymers [S1].

Revenue mechanics are tied to volume sold against customer contracts with embedded price formulas indexing feedstock costs to petroleum benchmarks allowing some input cost pass-through albeit imperfectly due to timing mismatches or competitive market resistance.

Margins fluctuate materially due to raw material price volatility (carbon black oil/fuel), energy costs associated with manufacturing processes consuming significant fuel inputs, and global logistic complexities. The firm's ability to optimize product mix towards higher-margin specialty offerings is critical but remains challenged under current cyclical economic softness.

Customer retention is anchored by long-term contracts primarily with tire OEMs, which ensure predictable demand; however, end-market softness or surging imports can disrupt demand patterns. Switching costs are moderate given product commoditization in certain segments, intensifying import competition.

Management has pursued cost containment efforts yielding SG&A expense reductions year-over-year despite inflationary pressures elsewhere [S1], signaling a focus on operational leverage.

Industry Structure and Competitive Position

The carbon black industry is characterized by high raw material intensity (petroleum-based feedstocks), significant energy consumption during manufacturing, and substantial capital investments required for facilities optimized for scale efficiency. This creates barriers to entry yet leaves incumbents vulnerable to feedstock market cycles.

Orion operates a globally integrated production footprint providing some geographic diversification benefits but also exposure to regional regulatory regimes affecting environmental compliance costs (e.g., EU carbon markets) and trade tariffs [S12][S24].

Competitively, Orion faces intense pricing pressure from low-cost Asian producers especially in tire carbon black where price-sensitive imports have eroded Western market share causing reduced profit margins as reflected by the goodwill impairment charge [S1]. Specialty carbon black's technical complexity lends somewhat better pricing power but is subject to cyclical industrial demand variation.

Further complicating industry dynamics are geopolitical uncertainties affecting crude oil supply impacting raw material cost stability. Pass-through pricing formulas provide partial mitigation but cannot fully shield earnings from rapid commodity price swings or political disruptions.

Growth Drivers

Growth levers for Orion rest on stabilizing raw material sourcing amidst geopolitical risks by diversifying suppliers and enhancing supply chain agility. The expansion of specialty carbon black applications offers premium margin potential contingent on innovation success and market penetration.

Incremental volume growth in Rubber Carbon Black remains linked closely to global tire demand trends correlated with automotive production cycles—electric vehicle adoption timelines influence capital deployment such as the delayed La Porte facility construction adjusted for EV adoption rates [S27].

Cost containment programs aimed at reducing distribution expenses and optimizing fixed cost absorption support profitability under softer revenue conditions. Additionally, sustainability-linked credit agreements incentivize emissions reductions at Northern American plants potentially improving long-term operational efficiency while aligning with ESG expectations [S17][S22].

Risks / Watchpoints / Growth Constraints

Key risks include:

- Raw material cost volatility exacerbated by geopolitical conflicts (Iran-U.S., Russia-Ukraine) disrupting crude availability affecting primary feedstock pricing adversely impacting margins if price pass-through fails or lags.

- Competitive challenges from Asian low-cost imports driving downward pricing pressure especially in core Rubber Carbon Black Western markets diminishing both volume elasticity and profitability.

- Regulatory tightening particularly regarding environmental emission standards adding operating costs or limiting capacity utilization.

- Liquidity constraints given elevated net leverage nearing covenant thresholds requiring careful working capital management amidst uncertain macroeconomic conditions.

- Demand softness in specialty industrial applications moderated by global economic deceleration constraining sustainable margin expansion.

What to Watch Next

Monitor upcoming quarterly filings for:

- Segment-level volume trajectories signaling recovery or further softness.

- Pricing updates especially feedstock pass-through efficacy reflecting commodity price trends.

- Operating margin trends clarifying whether cost savings offset price pressures.

- Capital expenditure milestones relating to La Porte facility advancement indicative of future capacity expansion aligned with EV adoption curves.

- Refinancing or covenant compliance disclosures around credit facilities amid leverage profile scrutiny.

- Geopolitical developments impacting oil supply chains that could materially influence raw material costs or sourcing reliability.

Financial Profile Brief Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $50.5mm | |

| 2026-03-31 | ||

| Total debt | $1,013.7mm | |

| 2026-03-31 | ||

| Net debt | $963.2mm | |

| 2026-03-31 | ||

| Current assets | $661.5mm | |

| 2026-03-31 | ||

| Current liabilities | $659.7mm | |

| 2026-03-31 | ||

| Current ratio | 1x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026, Orion holds approximately $50.5 million in cash against total debt of about $1.014 billion producing net debt of roughly $963 million. Current assets slightly exceed current liabilities yielding a current ratio near one indicating tight near-term liquidity balance [F1].

Capital expenditures remain significant ($161 million spent in Q4 FY25), reflecting investment into asset maintenance plus selected growth projects amid adjusted timelines responding to evolving market conditions [S8][S14].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments